In a matter of seconds, oil prices plunged 31% in Asia on Monday morning as the market reacted to what is fast becoming an all out price war between the world’s largest oil producers.

That’s the most oil prices have fallen since the Gulf war in 1991, in what is sure to set alarm bells ringing louder in oil-dependent Nigeria which risks a deeper fiscal crisis as a result of the abrupt price downturn.

Oil may be well headed towards projections made by Goldman Sachs, one of the most influential banks in commodity markets, which on Sunday lowered its price forecast for Brent to $30 a barrel for the second and third quarters, and warned there could be dips to $20 a barrel in the coming weeks.

Back at home, all eyes will be on Nigeria this morning to see how the financial markets react to tumbling oil prices, with many analysts predicting the worst sell-off in stocks, bonds and the currency since 2016.

Brent for May settlement tumbled as much as $14.25 a barrel to $31.02 on the London-based ICE Futures Europe Exchange. That’s the biggest intra-day loss since the U.S.-led bombing of Iraq in January 1991. It pared back some of those losses to $35.76 a barrel by 6:25 a.m. in Singapore, down $9.51.

Hammered by a collapse in demand due to the coronavirus, the oil market sank deeper into chaos on the prospect of a supply free-for-all. Saudi Arabia over the weekend slashed its official prices by the most in at least 20 years and signaled to buyers it would ramp up output — an unambiguous declaration of intent to flood the market with crude. Russia said its companies were free to pump as much as they could.

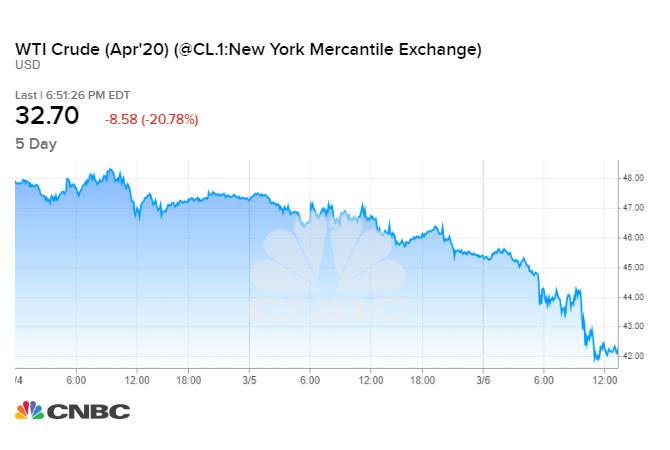

International benchmark Brent crudefutures plummeted 30% to $31.02 per barrel, its lowest level since Feb. 2016. U.S. West Texas Intermediate crude dropped 27% to $30 per barrel, also its lowest level since Feb. 2016. WTI is on pace for its worst day since January 1991 during the Gulf War, and its second worst day on record.

“This has turned into a scorched Earth approach by Saudi Arabia, in particular, to deal with the problem of chronic overproduction,” Again Capital’s John Kilduff said.

“The Saudis are the lowest cost producer by far. There is a reckoning ahead for all other producers, especially those companies operating in the U.S shale patch.”

After the initial drop the losses were pared somewhat, with each contract trading down slightly more than 21%.

On Saturday, Saudi Arabia announced massive discounts to its official selling prices for April, and the nation is reportedly preparing to increase its production above the 10 million barrel per day mark, according to a Reuters report. The kingdom currently pumps 9.7 million barrels per day, but has the capacity to ramp up to 12.5 million barrels per day.

“We believe the OPEC and Russia oil price war unequivocally started this weekend when Saudi Arabia aggressively cut the relative price at which it sells its crude by the most in at least 20 years,” Goldman Sachs analyst Damien Courvalin said in a note to clients Sunday. “The prognosis for the oil market is even more dire than in November 2014, when such a price war last started, as it comes to a head with the significant collapse in oil demand due to the coronavirus,” the firm added.

Goldman cut its second and third quarter Brent forecast to $30 per barrel, and said that prices could dip into the $20s.

Saudi Arabia’s price cut followed a breakdown of talks in Vienna last week. On Thursday, OPEC recommended additional production cuts of 1.5 million barrels per day starting in April and extending until the end of the year. But OPEC ally Russia rejected the additional cuts when the 14-member cartel and its allies, known as OPEC+, met on Friday.

The meeting also concluded with no directive about the production cuts that are currently in place but set to expire at the end of the month. This effectively means that nations will soon have free rein over how much they pump.

“As from 1 April we are starting to work without minding the quotas or reductions which were in place earlier,” Russian Energy Minister Alexander Novak told reporters Friday at the OPEC+ meeting in Vienna, adding, “but this does not mean that each country would not monitor and analyze market developments.”

Oil prices have already moved sharply lower this year as the coronavirus outbreak has led to softer demand for crude. A potential supply glut could pressure prices further.

“Both events – coronavirus and OPEC+ falling apart were not expected or priced into the market a month ago,” said Rebecca Babin, senior equity trader for CIBC Private Wealth Management. She said the key things to watch going forward are whether or not Saudi Arabia and Russia reach a “Hail Mary” deal, and if not, how quickly U.S. supply is shut in to support prices.

“There is still significant uncertainty, but the commodity market is not waiting around to find out if miracles can happen,” she added.

The unfolding of events is reminiscent of 2014 when Saudi Arabia, Russia and the U.S. competed for market share in the oil industry. As production escalated, prices plummeted. Some see prices heading back to those lows.

″$20 oil in 2020 is coming,” Ali Khedery, formerly Exxon’s senior Middle East advisor and now CEO of U.S.-based strategy firm Dragoman Ventures, wrote Sunday on Twitter. “Huge geopolitical implications. Timely stimulus for net consumers. Catastrophic for failed/failing petro-kleptocracies Iraq, Iran, etc – may prove existential 1-2 punch when paired with COVID19.”

But others, including Eurasia Group, believe that Saudi Arabia and Russia will eventually come to an agreement.

“The most likely outcome of the failure of the Vienna talks is a limited oil price war before the two sides agree on a new deal,” analysts led by Ayham Kamel said in a note to clients Sunday. The firm puts the chances of an eventual agreement at 60%.

Vital Knowledge founder Adam Crisafulli said Sunday that oil “has become a bigger problem for markets than the coronavirus,” but also said that he does not foresee prices falling to the Jan. 2016 lows.

“Saudi Arabia can’t tolerate an oil depression – the country’s fiscal breakeven oil prices remains very high, Saudi Aramco is now a public company, and MBS’s grip on power isn’t yet absolute. As a result, the [government] won’t be so cavalier in sending oil back into the $30s (or even lower),” he said in a note to clients Sunday.

The prospect of another price war is spooking traders who will remember the crash that began in 2014, when an explosion in U.S. shale production prompted OPEC to open the spigots in an attempt to suppress prices and curtail shale output.

That strategy ended in failure, with shale producers proving too resilient and Brent crude tumbling below $30 a barrel in 2016 amid a global glut of crude. And it was that crash that prompted OPEC to club together with Russia and others to curtail output and help shore up their oil-dependent economies.

An oil price war is the last thing the global economy, already struggling from the Coronavirus pandemic, needs.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp