Amid the economic tumult gripping Nigeria, President Tinubu’s administration is steadfastly navigating the nation towards calmer waters. At a pivotal event titled “An Economy in Distress: The Way Forward,” organised by the Leadership Group in Abuja, Mohammed Idris, the Minister of Information and National Orientation representing President Tinubu, shed light on the administration’s strides.

Contrary to despair, Idris emphasised that Nigeria is grappling with challenges but not succumbing to distress. He highlighted a glimmer of hope amidst the storm: a remarkable $30 billion in foreign direct investment (FDI) commitments secured within the nine months of President Tinubu’s administration.

These commitments, spanning sectors from manufacturing to telecoms, highlight a growing confidence in Nigeria’s economic potential. Idris also pointed out the recent surge in capital importation and the historic milestone of the Nigerian Stock Exchange All Share Index (ASI) crossing the 100,000-point mark in January 2024.

Read also: Beyond the decline: Examining Nigeria’s path to economic stability

President Tinubu echoed these sentiments, dismissing the notion that Nigeria’s economy is in dire straits. Instead, he painted a picture of resilience and progress, crediting ongoing reforms for these positive outcomes.

The increasing interest from foreign investors and the substantial rise in remittances from Nigerians abroad further validate Nigeria’s attractiveness on the global stage.

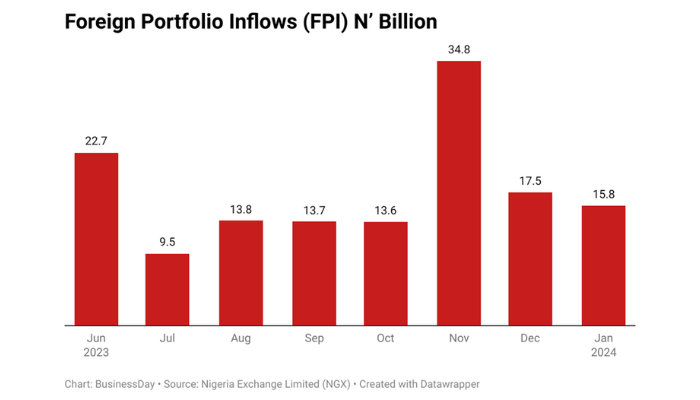

Foreign portfolio investors’ purchases of Nigerian securities exceeded $1 billion in February alone, totalling receipts of at least $2.3 billion for the year, according to Hakama Sidi Ali, a spokeswoman for the central bank.

This marked an increase compared with $3.9 billion for the entirety of 2023. Similarly, overseas remittances surged more than fourfold to $1.3 billion in February from the previous month.

Additionally, Nigeria’s sixth sovereign sukuk of 350 billion naira has been listed on the stock exchange and the FMDQ Securities Exchange. This move aims to enhance liquidity, enable trading, and achieve price discovery, signalling Nigeria’s commitment to embracing diverse financial instruments.

An intriguing question surfaces: What’s behind the concurrent positive effects? It seems akin to monetary wizardry, with authorities tightening the reins by hiking the monetary policy rate to 22.75 percent and the cash reserve ratio to 45 percent, yielding tangible results.

But there’s a catch: this move could spell trouble for local production firms, notably small and medium enterprises (SMEs). With banks left with a mere 30 percent liquidity for money creation, SMEs might feel the squeeze, hampering their growth and operations in the market.

According to a report by MSME Africa in the second quarter of 2023, a staggering 80 percent of small and medium enterprises (SMEs) in Nigeria face failure, largely attributed to economic challenges and regulatory constraints.

Factors such as harsh economic environments, limited access to capital, and poor business practices have been identified as major impediments hindering the growth and transition of micro-businesses.

As banks grapple with lower liquidity, SMEs may find it increasingly challenging to secure the funds they need to fuel their growth and operations. This could stifle their ability to innovate, expand, and stay competitive in the market, perpetuating the woes of capital inaccessibility.

On the flip side, there’s another obstacle: higher borrowing costs. Even if SMEs manage to secure loans, they could be burdened by soaring interest rates, eating into their profit margins and making it harder to sustain their operations.

This could hinder their capacity to invest in crucial areas such as technology, infrastructure, and talent development, ultimately limiting their long-term success and competitiveness. And so, the cycle of woe continues.

Yinka Sodipe, Group Investment Officer at Nigeria Exchange Group (NGX) Plc., emphasised the necessity for government intervention to address the adverse spillover effects of monetary tightening policies on small and medium enterprises (SMEs).

Sodipe suggested implementing a cushion policy to mitigate these effects, specifically focusing on enhancing the effectiveness of credit purchase financing. He highlighted the importance of stimulating demand through credit, particularly by enabling SMEs to procure goods and services from manufacturers and suppliers.

Philip Bakare, SME Financial Advisory Expert, further elaborated on various strategies that the government could employ to mitigate the impact of the tightening policy on SMEs.

He suggested the establishment of the Nigeria SME Growth Fund, a dedicated fund aimed at providing low-interest loans or grants to SMEs operating in priority sectors such as agriculture, manufacturing, and technology. Bakare emphasised the importance of transparency and accountability in the management of this fund, advocating for its administration by development finance institutions or government agencies.

Additionally, Bakare proposed the implementation of tax incentives for SME lenders as another means of support. He suggested that the government could offer tax incentives to banks and other financial institutions that provide loans to SMEs at favourable interest rates.

By incentivizing lenders through tax breaks or credits, the government could encourage increased lending to SMEs at reduced costs, thereby facilitating their access to much-needed financing.

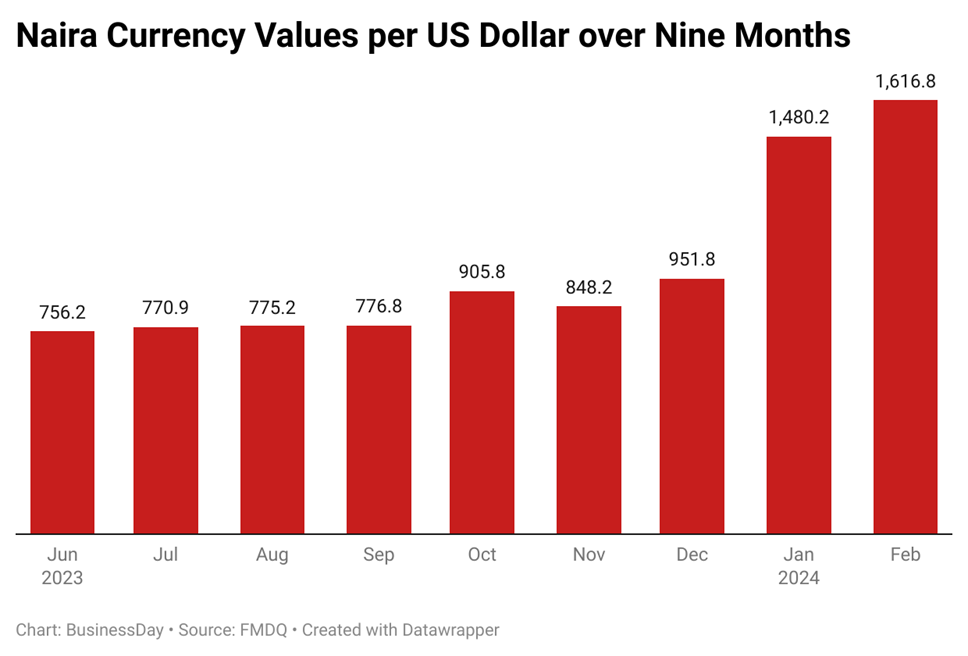

Despite the influx of $30 billion in foreign direct investment (FDI) and foreign portfolio investment (FPI) exceeding $1 billion in February 2024, as reported by Hakama Sidi Ali, a spokeswoman for the central bank, the exchange rate remains stubbornly high at N1,617.96, according to NAFEX as of March 12th, 2024.

This indicates that more US dollars are required, whether through FDI, FPI, or other revenue sources, to stabilise the naira—a simple yet pressing truth.

While there is a glimmer of optimism stemming from the positive effects of tightened monetary policy and increased foreign investment, the economy still requires more US dollars to experience a boom akin to that of the 1970s to support the naira.

Regrettably, Nigeria’s economic growth has often been characterised as ‘jobless growth’ over the decades—a scenario where economic expansion fails to alleviate poverty or reduce unemployment due to insufficient job creation or employment opportunities.

The current state of the economy in Nigeria reflects a sentiment of dissatisfaction among its citizens, who are growing increasingly disenchanted with business as usual. According to data from the National Bureau of Statistics (NBS), despite reported growth rates, the positive impact on the lives of ordinary Nigerians remains elusive. This underscores the urgent need for inclusive growth, where the benefits of economic progress are felt by all, particularly the poor.

Economists and some groups of professional update forums emphasise that it is no longer sufficient for the government to rely on superficial policies aimed at impressing the populace without delivering tangible results. Instead, there is a pressing need for a shift towards policies that prioritise inclusive growth and meaningful impact on the lives of citizens.

During times of economic hardship, the effects are immediately felt by the most vulnerable segments of society. However, during periods of economic prosperity, the focus often shifts towards mismanagement of resources, corruption, and investment in unproductive projects.

This cycle, reminiscent of the challenges faced in the 1970s after the period of prosperity, only serves to exacerbate poverty levels in the country.

It is unfortunate that the poor in Nigeria often bear the brunt of governmental mismanagement and malicious actions. Despite being the most vulnerable, they are frequently marginalised and overlooked in policy decisions, perpetuating a cycle of poverty and inequality.

The current economic climate in Nigeria emphasises the need for a departure from business as usual. It demands a renewed focus on inclusive growth, where the prosperity of the nation is measured not just by economic metrics but by the tangible improvements in the lives of all citizens, especially the most vulnerable among them.

Basit Shuaib, an economist, once said, ‘A country is as rich as its people or citizens.’

Oluwatobi Ojabello, senior economic analyst at BusinessDay, holds a BSc and an MSc in Economics as well as a PhD (in view) in Economics (Covenant, Ota).