Stronger FULL YEAR-19E earnings on the cards, supported by e-banking income

We expect Profit After Tax (PAT) to grow by 19.2 percent year-on-year to N71.22bn in full year 2019. Our higher earnings forecast is hinged on non-interest income growth (+10.0 percent year-on-year) and sustained decline in impairment charges (-13.4 percent year-on-year).

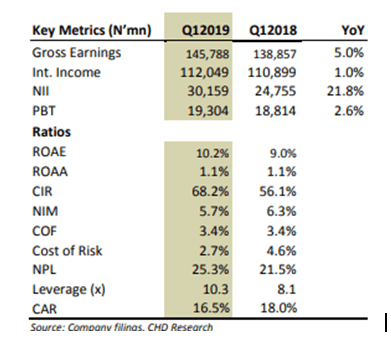

In first quarter of 2019, PAT grew by 6.9 percent year-on-year as non-interest income increased by 21.8 percent year-on-year and impairment charges fell by 45.3 percent year-on-year, offsetting the impact of the 26.3 percent year-on-year growth in operating expenses on earnings. The non-interest income growth was largely driven by electronic banking fees (+83.0 percent year-on-year).

E-banking’s contribution to non-interest income increased to 33.3 percent in first quarter of 2019 from 25.8 percent in full year-18, largely reflective of FBN’s stronger digital banking footprint with 10 million digital banking customers as at first quarter of 2019 (9.4 million in 2018).

Notably, the value of USSD and mobile banking transactions grew by over 100 percent in full year 2018 and the quarterly trend shows sustained expansion in first quarter 2019. Agency banking has also been supportive of increased volumes of e-banking transactions and management plans to further expand the number of “Firstmonie” agents to 30,000 by full year 2019 from 20,000 as at first quarter 2019.

Lower impairment charges to remain earnings supportive.

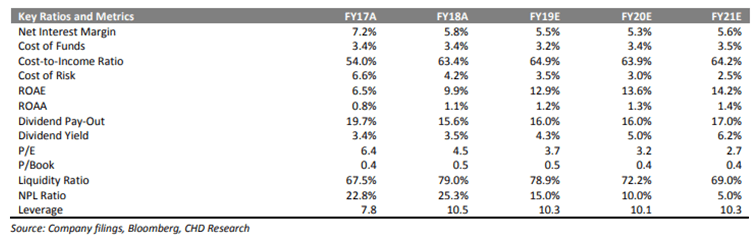

We expect impairment charges to decline by 13.4 percent year-on-year in 2019, post the 42.2 percent year-on-year drop in 2018, given FBN’s tightened risk framework. This is reflective of our lower cost of risk forecast of 3.5 percent (3.5 percent-4.0 percent guidance) vs. the 4.2 percent achieved in 2018.

Impairment charges fell by 45.3 percent year-on-year in first quarter of 2019 with the cost of risk at 2.7 percent. Loan growth was flat as at first quarter of 2019 (-0.6 percent Year To Date), but management expects lending to improve in subsequent quarters and guided to 5.0 percent loan growth in 2019, which could translate to higher impairment charges. It is worth highlighting the increase in FBNH’s Non Performing Loan (NPL) ratio to 25.3 percent in 2018 from 22.8 percent in 2017, against management’s guidance of 17-18 percent.

Management, however, remains confident on delivering its single digit NPL ratio target for 2019. The bank further disclosed that some of its legacy exposures (mainly Atlantic Energy) have been resolved and subsequent improvement in NPLs via restructuring, recovery and write-off, is expected in 2019. We are, however, cautious and forecast the NPL ratio at 15.0 percent vs. management’s guidance of less than 10 percent.

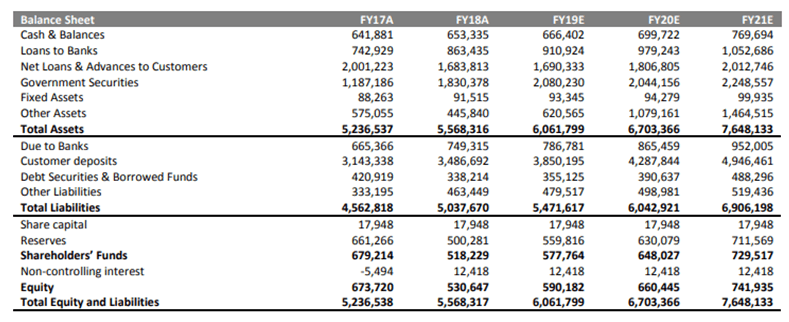

NIMs and cost efficiency could weaken in 2019. We expect the net interest margin to contract by 40bps in 2019 on lower asset yields. We note that FBNH reported a 150bps year-on-year expansion in yield on assets in first quarter of 2019 as interest income on investment securities was resilient, post the 6.8 percent year-on-year growth in investment securities to N1.48tn.

However, the 1.2 percent year to date drop amid lower asset yields suggests interest income could decline from second quarter of 2019 onwards. We expect funding costs to decline further in full year 2019, despite the pressure seen from higher interest expense on deposits from banks in first quarter of 2019.

We believe sustained mobilisation of cheap deposits (86 percent of total deposits in first quarter of 2019 as against 85 percent in full year 2018) amid lower market interest rates will support the moderation of cost of funds.

On cost efficiency, we expect the cost-to-income ratio to increase to 64.9 percent in 2019 from 63.4 percent in 2018 as we forecast operating expense (OPEX) growth at 8.4 percent year-on-year vs. +5.9 percent year-on-year for operating income.

We note that the cost to income ratio (CIR) spiked to 68.2 percent in first quarter of 2019 from 56.1 percent in first quarter of 2018, due to higher regulatory and promotion costs. Management’s cost-saving initiatives such as branch rationalisation as well as human capital and Information Technology transformation may, however, support improved efficiency from 2020.

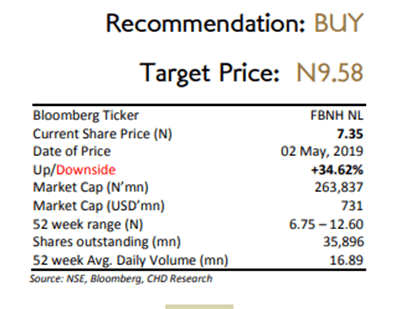

We maintain our BUY rating on FBNH, but cut our 12-month TP by 9.0 percent to N9.58.

This implies an expected total return of 34.6 percent (capital gain: 30.3 percent and 2019 dividend yield: 4.3 percent). We expect the full retention of the bank’s profit to persist in 2019 on the need to further strengthen its capital base. It is worth highlighting that FBN’s (bank only) Capital Adequacy Ratio (CAR) stood at 17.3 percent as at full year 2018 on regulatory transitional basis post IFRS 9 adoption, but was down to 16.5 percent as at first quarter of 2019.

Management further disclosed that the full year 2018 CAR would have been lower at 10.7 percent on full impact. We note that higher than expected credit losses and operating expenses as well as lower non-interest income are downside risks to our earnings forecasts. FBNH is trading on a 2019 estimated P/B and ROAE of 0.5x and 12.9 percent respectively vs. our banking coverage average of 0.7x and 16.6 percent respectively.