RMB Nigeria Stockbrokers has predicted a rebound for the Nigerian economy especially in the second half of 2021. The economic prediction and more insightful analysis could be found in its latest report captioned “Nigeria: Half year 2021 Market Outlook”.

The projected economic growth of 2 percent is hinged on a moderate growth in the non-oil sector and improvement in vaccinations which will cause more economic activities to be carried out in the country. Inflationary pressures are to remain moderately high as the investment house put its 12-month headline inflation at 17.2 percent in 2021, higher than average of 13.2 percent for 2020. Nigeria’s latest headline inflation figure for May 2021 was 17.93 percent.

Further, RMB Stockbrokers expects the Nigerian currency, Naira, to be pressured on the back of the monetary policy of the Central Bank of Nigeria (CBN) will be accommodative enough resulting in the naira-dollar exchange rate within a range of N470/$ at the BDC market while NAFEX is expected to be at an average of N425/$ in 2021.

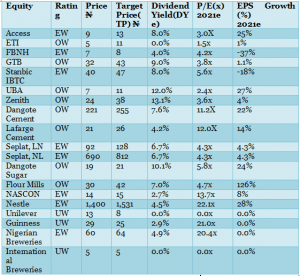

The investment house foresees an improvement in the interest rate environment, as that will deliver growth for Nigerian banks. Also, the Nigerian equity market is projected to be overweight, and consequently, RMB Stockbrokers favours equity over other asset classes in the remaining period in 2021. The firm estimates that equities in Nigerian market, trading on a 2021e P/E of 9.7x, amounts to a 5 percent discount to peer African markets and 20 percent to Kenya, and due to the negative real interest rate in Nigeria, equities at current prices are good bargain for long term investment.

As a result, RMB Stockbrokers identifies stocks that fit into its projection and these are Guaranty Holding Company Plc, Zenith Bank, United Bank for Africa (UBA), Dangote Cement, Lafarge, Flour Mills, and Dangote Sugar.

Sectoral projection: This is summarized below:

Cement industry

The demand for cement will remain strong into the second half of 2021, supported by the increase in housing infrastructure and commercial construction, and thus an 8 percent increase in cement consumption in 2021e.

Read also: Nigeria’s political space: Closing all gaps to grow the economy

“We upgrade Dangote Cement to (OW, TP: 255), as we expect the company to deliver record volumes in 2021e. We believe the company is adequately positioned to benefit from the increase in demand especially with the addition of new 3mmt capacity at the Obajana plant. From a valuation standpoint, Dangote cement trades on a 2021e P/E and EV/EBITDA multiple of 11.2x and 6.6x. We reiterate our OW rating on Lafarge Africa with our TP of N26 and expect earnings to continue to improve as the company repositions to focus on Nigeria following disposal of the troubled South African operation. Lafarge Africa trades on a 2021e P/E and EV/EBITDA multiple of 9.7x and 4.1x”, RMB said.

Key risks include foreign exchange risk and gas supply disruption.

“About 50 percent of production costs of cement manufacturers are linked to the dollar. These cost components include gas (major cost component), gypsum, bags and spare parts. As such, a steep devaluation in the currency will lead production costs to rise significantly, which will have a negative impact on the earnings of cement producers.

“Cement manufacturing is an energy-intensive activity with energy accounting for c.40% of costs. As such, disruption to gas supply, the dominant energy source for cement manufacturers in Nigeria, could negatively impact earnings”, RMB said.

Consumer goods sector

Rising inflation and high unemployment rate are to have significant impact on the consumer goods sector for the remaining part of 2021.

“For the consumer sector, volume growth in 2021e will remain stifled as inflationary pressure from the depreciation in the currency and local reforms especially the increase in the price of PMS and increase in electricity tariff, among others are expected to pressure consumer wallets. On a positive note, we expect the price increase implemented in 4Q20 into 2H21 by all consumer corporates to support margins and earnings in 2021e.

“We are overweight (OW) on Dangote Sugar (OW, TP: N21) and Flour Mills of Nigeria (OW, TP: N42) as we see these companies better able to weather the current challenging operating environment. Key risks to watch out for in 2021 in the sector are the direction of the currency and an upward adjustment in the price of PMS. A devaluation will be negative for earnings given that our coverage consumer companies are exposed to imported inputs while an increase in the price of PMS will weaken consumer spending power”, said the analysts at RMB.

Telecommunications sector

The nation’s telecoms sector has become a force to reckon with in the last few years in view of the significant growth of the firms in this sector, contribution to employment generation and market capitalisation of listed equities. With COVID 19 changing the way businesses are done, where some activities have been moved online, RMB foresees consistent increase in data consumption in Nigeria.

“For the Telecommunications sector, increased data consumption will propel growth for the rest of 2021, from greater broad band penetration (45 percent). In addition, we expect single digit growth in voice from improved rural penetration. That said, inflation from higher fuel and currency exchange rate losses will continue to weigh on operators profitability margins given the pricing competition between market leaders. Consequently, we expect double digit revenue growth for telecom operators with only 4 percent upside in EBITDA margins”, the investment firm said.

Oil and gas

Nigeria’s oil and gas industry is expected to be reignited following the passage of the Petroleum Industry Bill (PIB) by the National Assembly. On the other hand, government’s indecision to remove petroleum subsidy on the premium motor spirit may deny the three arms of government sizable amount of revenue. With general elections fast approaching, it is not clear when and how subsidy will be removed.

“In the oil & gas sector, we expect growth into the second half of 2021, supported by a timely recovery in global demand from developed economies and wider vaccine penetration. Additionally, we see little scope for a boost in market supply from Iran in 2021e, as we expect negotiations between the US and Iran to linger and keep sanctions in play till 2022e.

“Domestically, we expect stronger 2H21 output in view of OPECs unwinding schedule and estimate a 57 percent y/y appreciation in average crude prices in 2021. We are equal weight Seplat (EW, TP: N812, 128p), given the YTD rally on the counter and expect an improved outlook for the sector in 2022e. Seplat trades on a 2021e P/E and P/CF multiple of 4.3x and 2.5x respectively”, analysts at RMB said.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp