A recent report by the Global System for Mobile Communication Association (GSMA) intelligence has shown what developing countries can learn from India in driving financial inclusion through its Payment Service Banks (PSBs).

A PSB is a type of bank that operates on a smaller scale by harnessing technology services via mobile and agency banking to mobilize deposits and facilitate transfers from unbanked customers in rural areas and any location in a country. It is a key element of social inclusion, particularly useful in combating poverty and income inequality.

In Nigeria, three PSBs already have licences to operate such as Hope PSB, Money Master PSB and 9 PSB. Recently, MTN Nigeria, a telecommunications giant, MTN Nigeria has been granted final approval to operate mobile money (MoMo) PSB licence in Nigeria while MNO Airtel is expected to receive its licence soon.

According to the report titled ‘PSB in Nigeria: Opportunities and Challenges, as the PSB ecosystem in Nigeria is still in its infancy, these lessons and use cases can help inform how PSBs in Nigeria might create a value proposition and a successful, sustainable business model.

“PSBs will need to build profitable product, distribution and technology partnerships with other financial sector organisations such as deposit money banks, Fintechs and non-bank financial institutions, as well as in sectors such as agriculture, transport, utilities, humanitarian services and the public sector,” the report stated.

Read also: How MTN MoMo dominates mobile banking outside Nigeria

It adds, “PSBs will also need to optimise delivery channels and distribution networks while managing costs, make investments in seamless technology, clearly understand the product needs of unbanked populations and make a concerted effort to reach rural populations as well as building win-win product, payments and distribution partnerships in the wider ecosystem.”

The report also highlighted that for the PSB model to succeed in expanding formal financial inclusion, stakeholders must play an enabling role. “The regulator must provide regulatory clarity, provide a level playing field, make timely approvals for partnership requests and consider regulatory evolution as seen in India, as the market evolves.”

Nigeria and India share common similarities such as high population rate and poverty levels. While India has made significant progress in financial inclusion, the latter has made little progress as it is behind many other countries in formal financial inclusion.

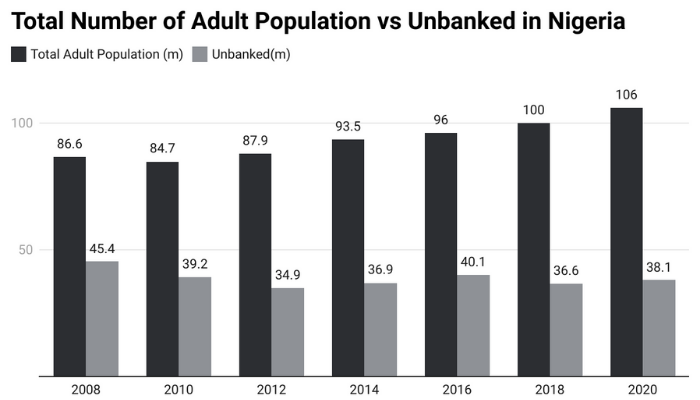

According to data from Enhancing Financial Innovation and Access (EFInA), Nigeria’s financial inclusion rate grew to 64.1 percent in 2020 from 63.2 percent in 2018. The 2020 figure is below the Central Bank of Nigeria (CBN)’s 80 percent financial inclusion target for the year 2020.

Although the inclusion rate dropped marginally from 36.8 percent in 2018 to 35.9 percent in 2020, the excluded adult population of 38.1 million reported in 2020 was higher than the 36.6 million recorded in 2018, meaning 1.5 million adults fell into the exclusion circle in the last two years to 2020.

“The country has historically maintained a bank-led model for financial inclusion and traditional banks have not been able to reach rural people due to several reasons such as the high cost of operating bank branches, onerous and bureaucratic on boarding procedures and lack of identity documents to open bank accounts,” the report highlighted.

India’s success in increasing financial inclusion is thanks to the Jan Dhan Yojana scheme launched in 2014. Narendra Modi, the prime minister, mandated that state-owned banks open at least one account for every unbanked household.

And so far, the initiative has helped to accelerate financial inclusion. According to the World Bank’s Global Financial Inclusion Database or Global Findex Report (2017), 80 percent of Indian adult populations have a bank account as of 2017, up from the 53 percent in 2014.

Currently, India has six Payment Banks namely, Airtel Payment Bank, India Post Payment Bank, Fino, Paytm Payment Bank, NSDL Payment Bank and Jio Payment Bank.

“Three of them are now profitable, suggesting that with a targeted strategy accompanied by enabling regulatory evolution, service banks may be able to extend financial inclusion and thrive commercially despite the limitations if they can sustain themselves during the early years of operations,” the report stated.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp