Higher adoption of mobile money is driving the growth of account ownership in financial institutions particularly in Sub-Saharan Africa (SSA) countries like Nigeria, a recent 2021 Global Findex report by World Bank has said.

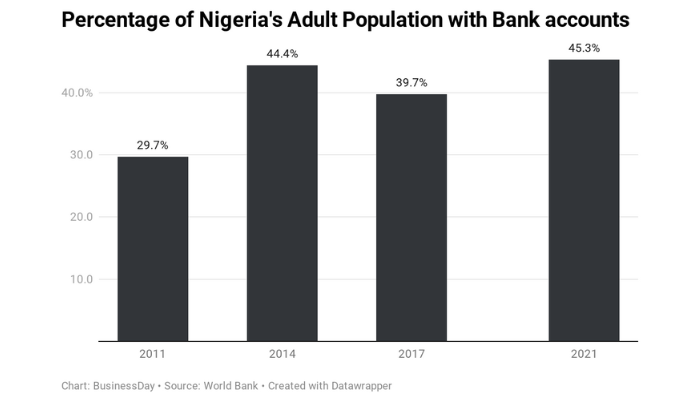

An analysis of the report titled ‘Financial Inclusion, Digital Payments, and Resilience in the Age of COVID-19, showed that Nigeria’s banked population increased by 15.6 percentage points to 45.3 percent in 2021, the highest in 10 years from 29.7 percent in 2011.

The 45.3 percent put Africa’s biggest economy in the 18th position out of 25 SSA countries.

A further analysis also showed that the percentage of women with bank accounts rose by 8.5 percent to 34.5 percent while the number of men who own bank accounts increased by 22.1 percent to 55.5 percent.

“Mobile money has become an important enabler of financial inclusion in Sub-Saharan Africa especially for women as a driver of account ownership and of account usage through mobile payments, saving, and borrowing,” the report stated.

The Global Findex Database has become a mainstay of global efforts to promote financial inclusion. Launched with funding from the Bill & Melinda Gates Foundation, the database has been published every three years since 2011.

Despite the improvement, Nigeria still has a high unbanked rate of 54.7 percent. The World Bank reports that Nigeria, India, China are among the countries contributing to the global unbanked population.

“Globally, about 1.7 billion adults remain unbanked without an account at a financial institution or through a mobile money provider. Because account ownership is nearly universal in high-income economies, virtually all these unbanked adults live in the developing world.

“Indeed, nearly half live in just seven developing economies such as Bangladesh, China, India, Indonesia, Mexico, Nigeria, and Pakistan.

The report also highlighted that Mauritius (90.5 percent), South Africa (85.4 percent), Kenya (79.2 percent), Namibia (71.4 percent) and Ghana (68.2 percent) are the five SSA countries with the highest percentage of banked population while South Sudan, Sierra Leone, Guinea, Burkina Faso and Malawi are the least five with 5.8 percent, 28.9 percent, 30.4 percent, 36.1 percent and 42.7 percent respectively.

Read also: AAA Entertainment gets $3.8mn film finance facility from Afrexim Bank

On the improvement for Nigeria, Temitope Omosuyi, an Investment Strategy Analyst at Afrinvest Limited noted that it is slow progress and that the country still has a long way to go

“For monetary policy to become extremely effective in achieving its objectives such as reducing inflation and ensuring financial stability, they need more people in the financial system,” Omosuyi said.

Data from Nigeria Inter-Bank Settlement System (NIBSS) and other sources shows that the volume and value of electronic financial transactions increased following the pandemic, and some financial services.

According to NIBSS, the volume of transactions through mobile devices rose by 128.4 percent to 153 million in the first four months (January-April) of 2022 from 67 million in the same period last year,

“We now have technology making businesses better and easier. It is also in line with the Central Bank of Nigeria (CBN)’s plan to drive financial inclusion in the country,” said Ayodele Akinwunmi, senior relationship manager, Corporate Banking Group, FSDH Merchant Bank

Financial inclusion means that people have access to basic financial services like a savings account, credit and insurance. It has continued to assume increasing recognition across the globe among policy makers, researchers and development oriented agencies.

Its importance derives from the promise it holds as a tool for economic development, particularly in the areas of poverty reduction, employment generation, wealth creation and improving welfare and general standard of living.

A higher exclusion rate in Nigeria could lead to a poorer population as lack of access to credit and insurance puts them at an economic disadvantage.

That is why in 2012, the CBN in collaboration with stakeholders launched the National Financial Inclusion Strategy aimed at increasing the inclusion rate to 80 percent by 2020.

And with 45.3 percent of the banked population, it shows that the country missed out its target. Thus, the CBN has set a new target of 95 percent by 2024 which is believed to be achievable by exploring new techniques and policies such as the Licensing and Regulatory Guidelines for Payment Service Banks, the Shared Agent Network Expansion Facility and generally providing the conducive regulatory environment for fintechs to contribute to financial inclusion.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp