… Nigeria need $25bn annually- Avuru

Once a vibrant hub for foreign investment, Nigeria’s oil sector has undergone a dramatic transformation, becoming a ghost town of lost opportunities as foreign direct investment (FDI) plummets from billions of dollars to mere trickles in recent days.

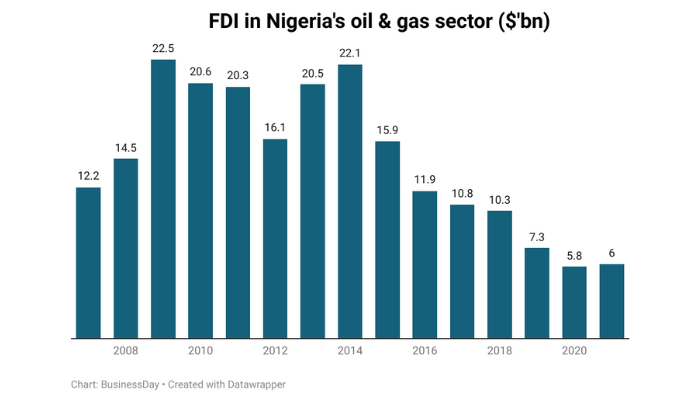

The 2010s witnessed a period of significant FDI from international companies eager to tap into the country’s vast oil and gas reserves as the future for Nigeria’s nascent indigenous upstream oil and gas industry looked bright, almost dazzlingly so.

Read also: Bureaucracy crimps oil sector as 20 federal agencies stifle operators

At its peak in 2014, Nigeria attracted the largest amount of FDI of any African country, with inflows exceeding $22.1 billion. This influx of capital fueled major projects, including deepwater exploration and development of new oil fields.

Oil was selling for more than $100 a barrel, as much as twice the production costs in Nigeria’s trickiest deepwater fields and several multiples of those in its shallow water and onshore fields.

Nigeria’s oil rigs, which depicts the level of oil fields averaged 35 rig counts in 2014, a development that translated to increased crude production as Nigeria’s output averaged 2.2 million barrels per day.

In August 2014 “the perfect storm of collapsing oil prices” arrived, said Carlos Hardenberg, lead portfolio manager of Templeton Emerging Markets Investment Trust. The naira fell, investors fled and Niger Delta militants who wanted a greater share of the country’s energy wealth struck.

Little has changed since then.

The country’s appeal had been tarnished by security problems that have only worsened since.

Compounding this internal rot is the exodus of oil majors such as Shell, ExxonMobil, Eni and TotalEnergies that once boomed with the rhythm of the pumps, now echo with the silence of departure.

The pain of this large-scale theft and vandalism, as well as decades of under-investment in infrastructure, was so severe that in April 2023, the country produced less than one million barrels of oil daily, far below its 1.8m bpd Organisation of Petroleum Exporting Countries quota.

In March, Nigeria’s oil production stood at 1.23m bpd.

“Nigeria currently needs $25 billion annually to stabilize its oil production at 2 million bpd,” Austin Avuru, executive chairman of AA Holdings said at the Harvard Business School (Association of Nigeria) event in Nigeria’s commercial capital.

Read also: Power tussle in asset sales, not theft, crippling Nigeria oil sector- Avuru

The Nigerian oil and gas industry was totally sidelined by foreign investors in the second quarter of 2023 for the first time on record with zero FDI, as the once lucrative sector attracted no capital inflow in the latest review quarter.

In the first quarter of 2023, oil FDI stood at $750, 000.

The country’s National Bureau of Statistics has not published its full-year 2023 FDI reports and its 2024 first-quarter FDI reports but it doesn’t take a seer to understand that the oil corporation is flailing.

“Prioritising political interests over transparency and due process in asset sales has led to corruption, mismanagement, and ultimately, the underperformance of the sector,” Avuru said.

He noted that those who should manage the process for a smooth transition from oil majors to local operators turned it into an “Approval Power Play”.

“Political connections rather than capacity became the qualifying criteria, in the absence of guidelines and defined processes,” Avuru explained

He noted that a long-drawn process meant that neither the divesting nor the acquiring entity was investing in the assets.

“Much worse most of the evacuation infrastructure fell into ‘no man’s land’; the divesting IOC’s stopped investing in their maintenance and surveillance,” Avuru said.

He added “A predictable noticeable and measurable decline in production set in but we chose to blame it all on “Crude Oil theft”.

BusienssDay’s findings showed fields that once accounted for more than two-thirds of all Nigerian oil production no longer represent value for multinationals, whose access to financing is critical for their development.

“Divestments by oil majors used to provide local operators an opportunity to prove their mettle, taking declining fields past production peaks, and improving host community relations to deliver higher royalties to the government; now local operators are scrambling to extract value from divested fields,” Tunji Oyebanji, energy lawyer at Lagos based oil firm said.

Last week, the federal government of Nigeria, through the Ministry of Petroleum (oil), announced it’s expecting to achieve a minimum of $20 billion worth of investment in the coming months.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp