From FMCGs and real estate to insurance and aviation, more businesses in Nigeria are making efforts to adjust their products and services to serve the larger segment of the low-income economy.

The marketing strategy, which is increasingly being adopted by many companies to increase their sales by targeting the low-income earners, signals Nigeria’s rising poverty rate.

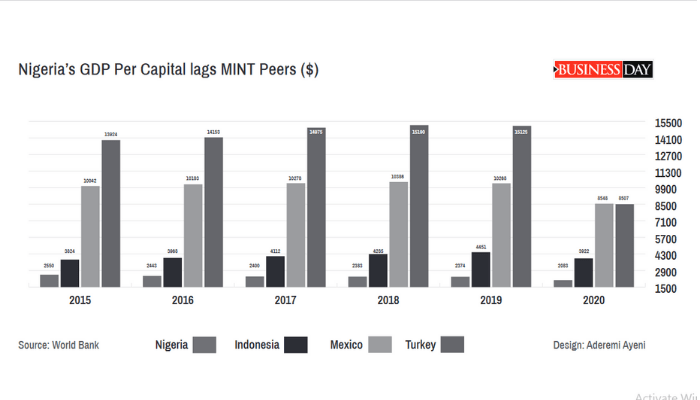

With a population of over 200 million people, Nigeria seems like a good destination for business as it has a large customer base. The problem with that is, almost half of the population are either too poor to afford essential goods and services or can now afford less of their usual consumption basket.

Businesses faced with reduced sales as a result of falling aggregate demand are forced to rebrand products and services into smaller packages (sachetisation) to boost profitability or close their shop.

“According to our conversation with the companies and the market, the winning strategy is to play ‘cheap’. Given the nature of the current economy where consumer wallet is depressed,” said Yinka Ademuwagun, research analyst, FMCGs, United Capital plc.

The National Bureau of Statistics (NBS) in the “2019 Poverty and Inequality in Nigeria” report highlighted that 40 percent of Nigeria’s total population, or almost 83 million people, live below the country’s poverty line of N137,430 ($381.75) per year.

The World Bank has also estimated that 11 million more Nigerians were dragged below the poverty line as a result of the pandemic and the economic recession experienced in 2020.

With data from the NBS showing a 1.92 percent contraction in 2020, it means Africa’s largest economy has now failed to match its average population growth rate of 2.6 percent for six straight years.

When economic growth fails to match population growth it means the economy is not creating new opportunities to accommodate a fast-rising population, and is a sign of worsening poverty levels.

“This has been a long-term trend. With the average Nigerian consumer facing stagnant income and higher commodity prices, it becomes imperative to provide some of these products in affordable smaller sizes. Thus, consumers buy what they need at a point in time as they make income,” Ayorinde Akinloye, a Lagos-based research analyst, said.

Read Also: Without reforms, Nigeria’s economic prospects remain subdued

Rising prices have put more strain on consumer’s already shrinking wallets.

According to data from NBS, Nigeria’s consumer price index, which measures the rate of increase in the prices of goods and services, slowed in April to 18.12 percent from 18.17 percent in March 2021. This is the first time it has slowed after rising for 19 straight months.

The number of jobless Nigerians rose to 27.1 percent in the second quarter of 2020, up from 23.1 percent in the third quarter of 2018, of which a large number are youths.

Poor consumers pay more in real terms

Although goods are made more affordable, businesses employing the sachetisation strategy make more profits and revenue from the poor customers. The sachets are loaded with contents small enough to attract price-sensitive customers but sizable to add up to a nice premium.

For instance, the retail price of a 50g of Golden Morn is N100, 10 sachet costs N1000 (50g X 10=500g). However, the retail price of a 500g pack is N850. The low-income customer is happy to avoid spending N850 on the 500g of Golden Morn and will pay N100 willingly.

With this strategy, poor consumers pay more in real terms for sachet goods while the rich spend less.

Aviation

Green Africa, the Lagos-based startup budget airline, made its entrance into the Nigerian aviation sector targeting the bottom of the pyramid with cheaper fares. Green Africa airfares range between N16,500 and N23,000, which is about a 50 to 70 percent slash in fares charged by other airlines.

Green Africa will fly to seven domestic destinations from Lagos, including Akure, Ilorin, Abuja, Owerri, Port Harcourt and Enugu. The company is offering cheap airfares at a time when the economic realities have weakened consumer purchasing power and Nigerians are afraid to travel by road given the rise in the number of kidnap cases on road trips.

Insurance

Insurance companies also recently began implementing staggered premium options across different class risks in an attempt to retain customers and attract new ones.

This means insurers have introduced different pay-out options like monthly or periodic pay-out options. The idea is to ensure that their customers that do not have enough money to purchase annual insurance policies are able to get the same cover on staggered payment of premium. Linkage Assurance and Consolidated Hallmark are some insurance companies offering these packages.

Meanwhile, across the insurance market, underwriters are wooing customers, particularly direct clients to pay in instalments as it is convenient for them, and many consumers are embracing this package, particularly in motor insurance policy.

FMCGs

Most leading Fast Moving Consumer Goods (FMCGs) companies have manufactured sachet packed products to capture poor consumers. This is all due to the waning purchasing power of consumers.

Most regular essential consumables such as milk, detergent, cooking oil, cereal, tomato sauce, cornflakes, toothpaste and so many other products are now in sachets. More recently, Baileys, Dettol, Morning Fresh and Hollandia have been added to the list of products now in sachets. This is to encourage quick sell and increase competitiveness in the consumer goods space, where affordability continues to be a big issue.

Real estate

According to the United Nations, Nigeria has a projected deficit of between 17 million and 22 million housing deficits. Efforts are on in the real estate industry to make housing more affordable to low-income earners and bride housing deficit.

For instance, the Federal Housing Authority (FHA) and Family Homes Funds have partnered to deliver 1,000 affordable housing units to low-income Nigerians.

The homes would be such that people can buy from N2 million for 1 bedroom, about N2.5 million to N2.75 million for two bedrooms and N3.5 million to N3.25 million for the 3 bedroom.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp