KPMG Nigeria, a professional services company, has projected that the oil sector in Africa’s biggest economy would exit recession in the fourth quarter of 2023, after 14 consecutive quarters of negative growth.

In the company’s latest report titled ‘Expected Sluggish Q3 2023 GDP Growth’, it said the improvement in Q4 will be driven by recent and ongoing efforts targeted at curtailing oil theft and oil infrastructure vandalism.

“Furthermore, the increase in crude oil production could be as a result of oil discovery by the Petroleum Production License awardees of the 2020 marginal field bid round,” the report said.

It said the Nigerian Upstream Regulatory Commission had in June last year handed over 57 oil fields located onshore and swamps of the Niger Delta to local oil companies with a charge on them to quickly develop the fields and produce the first oil before the end of 2023 as published in the Africa Oil+Gas report in September.

Read also: Nigeria’s oil GDP drops 9% in second quarter of 2023

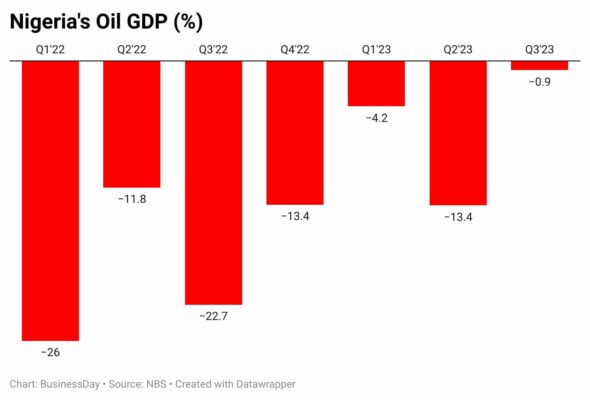

According to the National Bureau of Statistics (NBS), Nigeria’s oil sector, a major source of government revenue, recorded a real growth rate of –0.85 percent (year-on-year) in Q3, indicating an increase of 21.8 percentage points relative to the rate recorded in the corresponding quarter of 2022 (-22.7 percent).

“Growth also increased by 12.6 percentage points when compared to Q2 which was –13.4 percent. On a quarter-on-quarter basis, the oil sector recorded a growth rate of 12.5 percent in Q3,” the NBS report said.

It said the nation in Q3 recorded an average daily oil production of 1.45 million barrels per day (mbpd), higher than the daily average production of 1.20mbpd recorded in the same quarter of 2022 by 0.25mbpd and higher than Q2 production volume of 1.22 mbpd by 0.23mbpd.

In terms of the overall GDP, Africa’s most populous nation grew by 2.54 percent (year-on-year) in Q3 from 2.51 percent in Q2 and 2.25 percent in the same period last year.

“The under-welling performance of the economy in Q3 did not come as a surprise and align with our expectation in various recent publications on the economy of continuous slow and fragile growth at or below population growth,” authors of the KMPG report, said.

They opined that the continuous slowdown in household consumption demand and private investment in the presence of high and rising double-digit inflation and costs of production will conspire to keep growth slow.

Read also: Here is why Nigeria’s oil GDP is at the lowest since 2016

“We had also maintained that the ability of the economy to grow at high growth rates also depended on the oil sector exiting recession and the economy achieving macro stability before we can experience any stronger growth that will enable the economy to meet the current administration ambition of attaining a $1trillion economy by 2030.”

KPMG retained its earlier GDP forecast for 2023 at 2.65 percent driven by continuous improvements in the oil sector, while expecting the non-oil sector to retain its slow and fragile performance on the back of weakening household purchasing power, generally weaker private investments, and higher business costs.