Traders reduce bets on US rate cuts after buoyant economic data

Bond traders have had a major rethink on the path of US interest rates, reducing bets on a series of cuts after stubbornly high inflation readings and strong economic data.

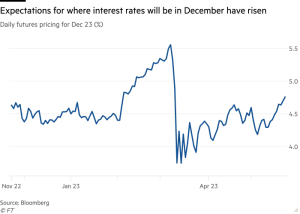

A little more than two weeks ago, traders in the Treasury futures market had put money on the possibility that interest rates could be cut to 4.2 per cent by the end of the year, from the current range of 5 per cent to 5.25 per cent, suggesting three or even four rate cuts. Now that expected tally has dropped to a likely maximum of two, taking rates to 4.7 per cent.

The broad shift drags investors more in line with the consistent message from the US Federal Reserve that it has no plans to chip away at rates while inflation remains far above its target. But it also underlines the state of intense uncertainty over where markets are heading next.

“If you are feeling confused about the macro outlook, it is important to realise that you are not the only one,” wrote Dario Perkins, an analyst at TS Lombard in London.

“A head-clutching Old-Testament-style recession would resolve many of these tensions and bring some clarity to the outlook. But I would not be surprised if the confusion continued for a while longer, with a global macro environment that continues to frustrate both the bulls and the bears.”

Read also: German right cries foul over return of Benin Bronzes to Nigeria

Since the collapse of Silicon Valley Bank and other regional US lenders this year, financial markets have expected a credit crunch to result in a US recession, which could prompt the Fed to cut rates.

Meanwhile, US consumer price rises have been slowing, reaching an annual pace of 4.9 per cent in April. Some investors have taken that, in combination with the regional bank failures, as a sign that the Fed will start to reverse the historically aggressive pace of rate rises that it has executed over the past 14 months.

But the Fed itself has never been sympathetic to that view, and in recent weeks a growing number of its policymakers have reminded traders that the fight with inflation is far from over. The US job market has also remained robust, with the unemployment rate hovering at 54-year lows. A brief rise in weekly claims for unemployment benefits earlier in May ultimately turned out to largely be the result of fraud, economists said. Bond markets are caught in these cross currents.

“The data flow has been a bit better recently. People got worried [about] the jobless claims number . . . but then finding out it was fraud in Massachusetts and that we’re trending not quite as high is one reason we’ve taken out some of the cuts,” said Jay Barry, head of interest rate strategy at JPMorgan.

Barry also noted that the JPMorgan surprise index, which compares investors’ perceptions of economic growth against the reality in the data, has jumped significantly in the past few weeks.

Fed Chair Jay Powell on Friday said that the credit crunch expected in the wake of the collapse of the regional banks may limit how much the Fed needs to raise rates.

“The sooner we see the Fed stop hiking rates, the less economic damage we’ll see, so the less need we’ll have to cut rates,” said Kristina Hooper, chief global market strategist at Invesco.

This adjustment in views on rate cuts could matter for asset managers, who have been piling into shorter-dated bonds, betting that interest rates will come down. The yields on shorter-dated Treasury notes move with inflation expectations, so a rise in yields could be costly.

“From here, I think the level of uncertainty remains high and investors will remain extremely cautious given the tail risks ahead and the highly volatile start to the year,” said Kavi Gupta, head of US rates trading at Bank of America.

Investors also say that recent progress on debt ceiling negotiations could be pushing yields higher.

“This is generally a world where US Treasury bonds rally on a fear of a default by the US government over that horrendous debt ceiling debate, so the fact that bonds have sold off and yields have risen is at least driven in part by hopes and expectations that a deal on that is near,” said Jim Leaviss, chief investment officer for public fixed income at M&G Investments, on a podcast this week.

Analysts at BlackRock suggested investors are falling back into the habit of assuming that market stresses or economic wobbles will nudge the Fed and other central banks into backing down on rates.

“Most developed markets are grappling with a shared problem. Core inflation is proving more stubborn than expected and remains well above central banks’ 2 per cent targets,” they wrote in a recent note.

“We think that means central banks can’t undo any of their inflation-fighting rate hikes any time soon, even if financial markets think the Federal Reserve will start cutting rates before the end of the year. We see recession ahead. But unlike in the past when central banks would cut rates to stimulate a struggling economy, we think the unresolved inflation problem makes that unlikely this time.”

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp