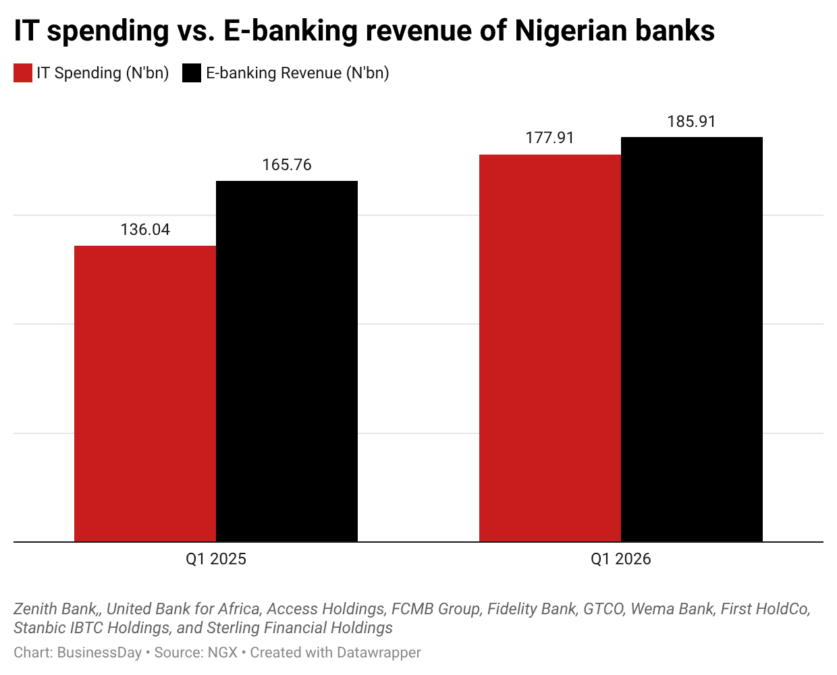

Nigeria’s banks increased their spending on information and technology (IT) by 30.8 percent in the first quarter of 2026, driven by the growing adoption of artificial intelligence and digital channels.

A BusinessDay analysis of the first-quarter (Q1) 2026 financial statements of 10 lenders show

```

Members Only

Login or create an account to continue

This article is available to registered BusinessDay readers. Please login if you already have an account, or create a new account to continue reading.

New to BusinessDay? Register now and start reading.

```

Chinwe Michael

Chinwe Michael is a financial inclusion advocate and economy journalist who uses compelling storytelling to drive awareness. With a background in Banking and Finance and experience across accounting, media, and education, she applies sharp analysis and attention to detail to every piece. She simplifies complex financial and economy concepts into engaging content for Africa and global audience. Chinwe also doubles as a speaker with global recognition for her expertise.