After years of relying on aggressive price increases to survive one of the country’s toughest macroeconomic periods, consumer goods firms are now entering the second half of 2026, where earnings growth will depend less on inflation-induced price hikes and more on volume recovery, operational efficiency, and balance-sheet strength.

BusinessDay’s analysis of nine listed consumer goods companies- Cadbury Nigeria, Champion Breweries, BUA Foods, Dangote Sugar Refinery, International Breweries, NASCON Allied Industries, Nestlé Nigeria, Nigerian Breweries, and Unilever Nigeria, shows that the high revenue growth that characterised the immediate aftermath of President Bola Tinubu’s economic reforms has slowed down.

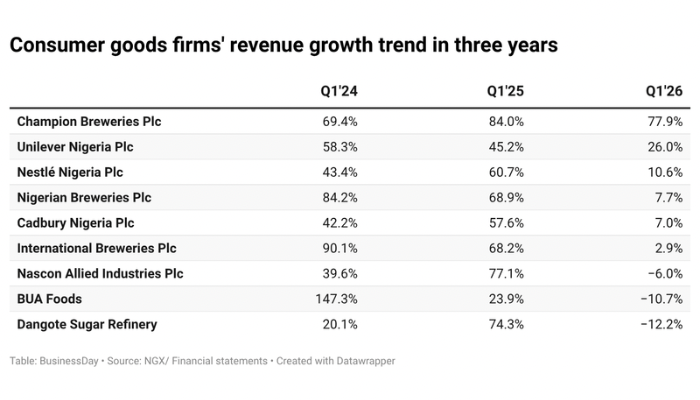

Analysis shows that the first-quarter (Q1) revenue growth across the companies dropped to 11.3 percent in Q1 2026, from 62.2 percent in Q1 2025 and 66.1 percent in Q1 2024, indicating that the industry’s next challenge will be sustaining earnings in an environment where companies have largely exhausted their ability to raise prices.

Abdulrauf Bello, portfolio manager at Cowrywise, stated that the sector’s impressive earnings over the past 18 months were largely driven by aggressive pricing actions that are unlikely to be repeated in the second half of 2026.

“The reason is that many of them have done really well. Starting from 2024 and through 2025, almost all of them raised prices, and there was really no fear of backlash because consumers had very few alternatives. Everybody was increasing prices.”

According to him, those price increases significantly lifted revenues and restored profitability after companies battled record foreign exchange losses, soaring inflation, and rising production costs following the naira liberalisation.

“That helped to boost margins, but there is no excuse to raise prices anymore because the foreign exchange market is now relatively stable,” he said.

When Tinubu assumed office in May 2023 and implemented sweeping reforms, including the removal of petrol subsidies and the liberalisation of the foreign exchange market, consumer goods manufacturers faced soaring production costs, unprecedented naira depreciation, foreign exchange losses, and record inflation.

Unable to absorb the shocks, companies repeatedly increased product prices to protect margins. Revenue surged, but much of that growth was driven by inflation rather than stronger consumer demand.

Three years later, analysts say the sector has reached an inflection point.

“The cycle has turned, and recovery has taken place, but 2026 is a year of stabilisation where abnormal profit will increasingly be determined by execution,” ARM Research said in its 2026 Nigerian Consumer Goods Playbook.

Pricing-led growth gives way to volume battle

The sharp moderation in revenue growth during the first quarter was not entirely unexpected.

A consumer market report by Boston Consulting Group’s Africa Consumer Sentiment Survey 2025 disclosed that Nigeria’s consumer economy is under pressure, with 83 percent of households cutting back on discretionary purchases as inflation, weak income growth, and currency instability continue to erode purchasing power.

The pullback places Nigeria among the most financially strained consumer markets in Africa, alongside Kenya and South Africa, and highlights the depth of stress facing households across Sub-Saharan Africa.

Unlike previous years when manufacturers aggressively repriced products to offset higher costs, many companies entered 2026 pursuing affordability strategies aimed at rebuilding volumes and protecting market share.

BUA Foods, for instance, reported a 10.7 percent decline in revenue in the first quarter of the year, compared to other years when the company’s revenue growth rose from 147.30 percent in Q1 2024 to 23.9 percent in 2025, after deliberately adopting more competitive pricing, while Dangote Sugar and NASCON also experienced revenue declines of 12.2 percent and 6 percent, as companies prioritised customer retention over aggressive price increases.

Even companies that still posted revenue growth, including Nestlé Nigeria, Nigerian Breweries, Cadbury Nigeria, and Unilever Nigeria, recorded far slower expansion than the double- and triple-digit increases seen over the past two years.

The slowdown reflects a fundamental reality: Nigerian consumers have reached their affordability limits. Years of elevated inflation have significantly eroded household purchasing power, forcing consumers to prioritise essentials, switch to cheaper brands, and embrace smaller pack sizes.

According to ARM Research, the sector is transitioning from the pricing-led expansion that defined 2023 and 2024 toward a more balanced mix of volume recovery and margin normalisation as companies increasingly struggle to implement broad-based price increases.

“Rather than relying on inflation to lift revenues, manufacturers are now competing through affordability initiatives, wider distribution networks and product innovation,” it said.

Data released by the National Bureau of Statistics (NBS) showed that the manufacturing sector grew by 3.29 percent year-on-year in Q1’26, compared to 1.69 percent recorded in the corresponding period of Q1’25.

The performance represents the sector’s strongest quarterly growth since the first quarter of 2022, when manufacturing expanded by 5.89 percent. It also marked a notable recovery from the preceding quarter, Q4’25, when the sector’s growth stood at 1.12 percent.

Macro headwinds remain

Despite signs of recovery, operating conditions remain far from easy.

The conflict, which began on February 28, 2026, appears to be gradually waning, as President Donald Trump said the US has agreed to continue talks with Iran, but the ceasefire is over.

This has fuelled volatility in global energy markets, increasing freight and logistics costs, and raising concerns over the cost of imported inputs used by Nigerian manufacturers.

The World Bank said fuel prices in Nigeria have risen by more than 50 percent following global crude shocks, with petrol prices climbing from below N870 per litre to above N1,300 per litre on average. Diesel, widely used by manufacturers because of the unreliable public electricity supply, has risen by about 70 percent to around N1,550 per litre.

Higher energy costs threaten to erode the efficiency gains that underpinned first-quarter earnings, particularly for manufacturers operating on thin margins.

During the period, Nigeria’s inflation declined for eleven consecutive months, falling from around 34 percent in 2024 to 15.06 percent by February 2026.

However, inflation began climbing again, rising from 15.38 percent in March, 15.69 percent in April and 15.93 percent in May, marking its highest level since November 2025

“I expect to see the impact of the war on the cost of sales, which is expected to require businesses to raise prices to keep the bottom line competitive,” said Samuel Oyekanmi, chief research officer at Abuja-based consultancy Norrenberger.

Kemi Abiodun, a consumer goods research analyst at Lagos-based consultancy CardinalStone, expects second-quarter earnings to reflect rising operating expenses, although she believes the sector is still likely to post resilient half-year results.

“For H1, I am a bit mixed on the bottom line because there’s this OPEX from surging energy prices that may affect some of them. We should probably expect relatively good numbers.”

Analysts’ expectations for the second half of the year

Analysts at Zedcrest Research

In its H2 2026 Consumer Goods Outlook, Zedcrest Research said the sector’s fortunes will increasingly depend on companies’ ability to manage costs and strengthen operations rather than rely on price increases.

“We maintain a cautiously positive outlook on Nigeria’s consumer goods sector in H2 2026,” the report said. “Sector performance is expected to be driven more by cost optimisation, localisation, backward integration, and stronger balance sheets than by pricing power alone.”

The research firm noted that while foreign exchange pressures have eased considerably from the shocks of 2023 and 2024, manufacturers now face a different set of challenges.

“Elevated inflation, energy costs, and weak consumer purchasing power remain key risks,” it said, adding that firms with stronger supply chains, greater operational efficiency, and disciplined cost management are expected to outperform peers.

According to the report, weak household purchasing power will continue to restrain demand, leaving companies with little room for broad-based price increases.

“Revenue growth is expected to remain modest and increasingly dependent on product mix, selective price adjustments, and incremental volume gains rather than a strong consumption upswing,” Zedcrest said. It expects consumers to continue favouring smaller pack sizes, value brands, and essential food products over discretionary spending.

Food manufacturers are expected to remain the sector’s biggest winners because demand for staples is relatively resilient, while breweries and discretionary consumer goods companies are likely to face greater pressure from slowing consumer spending and high production costs.

Although fertiliser prices have begun to stabilise, Zedcrest warned that earlier spikes have already filtered into agricultural production cycles, meaning manufacturers will continue to contend with elevated input costs.

“The sector’s broader cost environment is increasingly being shaped by more persistent pressures from energy, transportation, logistics, and distribution expenses, which are expected to remain the dominant drivers of margin performance through H2 2026,” the report said.

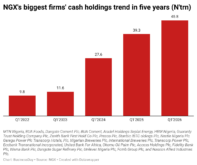

The outlook also points to stronger corporate finances after several manufacturers raised capital to reduce debt and improve liquidity.

Analysts at Meristem Research

Meristem Research maintained a positive outlook for Nigeria’s consumer goods sector in the second half of 2026, citing improving macroeconomic conditions and stronger corporate fundamentals.

“The outlook for the consumer goods sector remains positive for the second half of 2026,” the analysts said. “We expect revenue growth to remain supported by stable macroeconomic conditions, improving consumer demand, and continued investments in capacity expansion and product innovation.”

The research firm said profitability is expected to remain resilient as exchange rate stability, easing inflation and continued backward integration improve operating efficiency and reduce input cost pressures.

“While elevated energy costs and competitive pricing may weigh on margins for select players, companies with strong brands, efficient distribution networks, and diversified product portfolios are well positioned to sustain earnings growth through the remainder of the year,” the report stated.

On breweries, Meristem said the industry’s recovery is expected to gather momentum in the second half despite lingering cost pressures.

“We expect the brewery sector’s recovery to continue through H2 2026, supported by the full-year impact of March price increases, stable consumer demand, and a more favourable macroeconomic environment,” the analysts said.

According to the report, exchange rate stability and moderating inflation should continue to support profitability, although the proposed excise tax stamp policy could raise compliance costs if implemented.

“Overall, we expect Nigerian Breweries, Champion Breweries, and Guinness Nigeria to remain best positioned to sustain earnings growth,” Meristem added.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp