Nigeria’s capital market is reacting positively, unlike any of its previous election cycles, and regulators and analysts are converging on the same explanation: investors have stopped treating the political calendar as the market’s biggest threat.

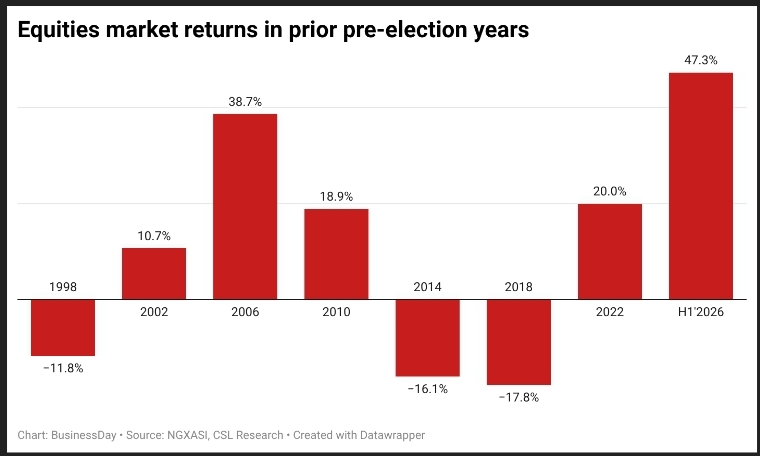

The Nigerian Exchange closed the first half of 2026 with a 47.4 percent return, its strongest pre-election half-year performance in almost three decades.

Data by CSL Stockbrokers shows equities have historically struggled in the build-up to presidential polls, losing 11.8 percent in 1998, 16.1 percent in 2014, and 17.8 percent in 2018. This year’s rally breaks that pattern by a wide margin, and the divergence has become the central talking point among market watchers ahead of the 2027 election.

For the Securities and Exchange Commission (SEC), the resilience is not incidental. Speaking at the Mid-Year Capital Market Review, Mid-Year Macroeconomic Review and Investment Outlook, Emomotimi Agama, director-general of the Securities and Exchange Commission (SEC), said the current cycle differs from previous election years because the reforms underpinning it are structural rather than cyclical.

“Elections themselves do not necessarily undermine market performance, as investors are more concerned about policy uncertainty than the political calendar,” Agama said.

He argued that Nigeria’s macroeconomic environment is considerably stronger than during comparable pre-election periods over the past decade and pointed to domestic institutional investors, including pension fund administrators, insurance companies, and collective investment schemes, as a stabilising force that previous election cycles did not have.

“The Commission’s responsibility is to ensure that market regulation remains completely insulated from politics. Our rules, enforcement mechanisms, and market infrastructure will continue to function efficiently before, during, and after the elections,” he said.

Agama added that investors with medium and long-term horizons often treat pre-election caution as an entry opportunity, accumulating fundamentally strong stocks while sentiment is subdued elsewhere in the market.

Uche Uwaleke, Nigeria’s renowned capital market economist, said the approach of the 2027 general elections presents another source of uncertainty for financial markets.

According to him, increased election-related spending could inject liquidity into the economy but may also fuel inflation if not carefully managed.

“If inflation is demand-driven as a result of increased money supply, the Central Bank will be compelled to hike interest rates,” Uwaleke said.

“There is an inverse relationship between rising interest rates and stock market performance.”

A market cap trajectory that tells its own story

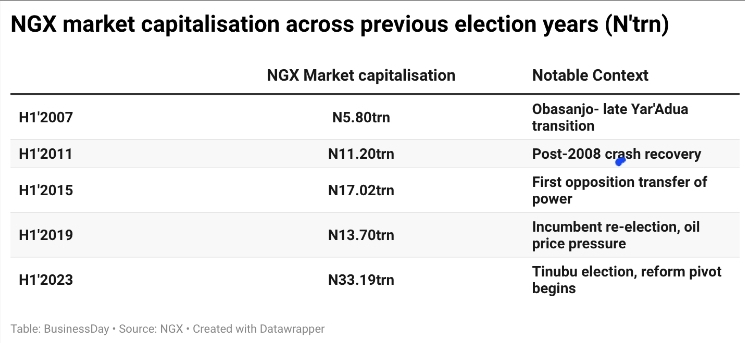

The NGX’s election-year market capitalisation history shows a broadly upward path, though not a straight line. Market capitalisation rose from N5.8 trillion in the first half of 2007 to N11.2 trillion in the first half of 2011 and N17.02 trillion in H1 2015, before slipping to N13.7 trillion in H1 2019 amid naira pressure and a subdued oil price environment. By 2023, the year President Bola Ahmed Tinubu was elected, and the reform programme began, it had climbed to N33.19 trillion

That 2019 dip is the exception analysts point to when weighing how much comfort to take from the current rally; market capitalisation gains built on sentiment alone have reversed before when reform momentum stalled or global conditions turned. Agama, the SEC DG, for his part, was careful to separate the current rally from speculation.

“The easy repricing has largely taken place. Going forward, earnings growth, sound corporate governance, and financial performance will determine which companies continue to outperform,” he said, addressing suggestions that valuations have run ahead of fundamentals.

He attributed the first-half performance to improving corporate earnings, the successful recapitalisation of banks, exchange rate stability, and renewed foreign investor participation, rather than to speculative trading.

Asalu Adegboyega Yinka, a stock market analyst, said that the election cycle pattern was broken in 2022 and 2026. Being a pre-election year, the benchmark index consolidated on what happened in 2022.

“What actually plays a great role in our equity market is improved macroeconomic parameters such as exchange rate stability, growth in GDP, deceleration in headline inflation, improved external reserves above $50 bilion primarily driven by Dangote Refinery, effective control of MPR by CBN, sound corporate earnings from both listed and unlisted companies in Nigeria, and successful recapitalisaton of banks in Nigeria raising N4.6 trillion in the last twenty-four months,” he said.

CSL’s research also credits the banking sector specifically for anchoring this year’s rally, pointing to an elevated interest rate environment that has supported net interest margins, balance sheet expansion following recent capital-raising exercises, improved foreign currency liquidity, and strong profitability across Tier-1 and Tier-2 lenders.

That combination, the report argues, has reinforced banking stocks’ role as the primary conduit through which foreign portfolio inflows re-enter the Nigerian market, a role reformed pricing discovery under the Nigerian Foreign Exchange Market framework has made easier to sustain.

Three tickets, one continuity thesis

Away from the SEC’s public messaging, sell-side research is arriving at a similar conclusion through a different route. A CSL Stockbrokers report dated 30 June assesses the emerging electoral landscape as a three-bloc contest: the ruling All Progressives Congress (APC), fielding President Bola Tinubu on a platform of reform continuity; the Nigeria Democratic Congress (NDC), anchored by Peter Obi and running mate Rabiu Kwankwaso on a fiscal-discipline and governance-repositioning agenda; and the African Democratic Congress (ADC), led by Atiku Abubakar with Rotimi Amaechi, offering the deepest pool of executive experience among the three but the least defined reform narrative.

CSL’s analysts disclosed that an APC victory is the lowest-disruption scenario for markets, likely to sustain the current trajectory of exchange-rate liberalisation, fiscal consolidation, and foreign portfolio inflows. An NDC-led outcome, by contrast, could trigger initial volatility, but the report suggests this could turn constructive if early cabinet appointments and policy signals reassure investors, with banking, infrastructure, consumer goods, and export-oriented stocks flagged as potential beneficiaries.

While an ADC victory is expected to draw a more cautious, wait-and-see response, with the market’s reaction depending less on the outcome itself than on the calibre of the incoming economic team.

The report added, “The APC is the cost-of-living crisis, elevated inflation and weak purchasing power could harden anti-incumbency sentiment, compounded by rising insecurity in parts of the Southwest alongside the more familiar threats in the north.”

“The NDC’s is organisational: a comparatively thin nationwide vote-delivery network relative to the ruling party’s structure across all six geopolitical zones. The ADC’s investors are still waiting for clarity on how an Atiku-led government would diverge from the current administration or from previous ones, while Abubakar’s history of repeated presidential bids risks dampening enthusiasm among some segments of the electorate.”

An incumbent victory is not automatically bullish if macroeconomic conditions deteriorate: the report warns that if inflation remains stubbornly high, fiscal deficits widen, or reform momentum stalls after the vote, any positive market reaction could prove short-lived, regardless of who occupies Aso Rock.

Currently, Nigeria’s headline inflation slowed to 15.91 percent in June 2026, its first time in five months, signaling that monetary authorities may hold key interest rates even as global energy volatility continues to dampen local prices, the National Bureau of Statistics disclosed in its June inflation report.

Olayemi Cardoso, the CBN governor, said during a fireside chat at the BusinessDay CEO Forum 2026, that authorities had projected that a rate cut was imminent as inflation began to gradually cool, but the longer-than necessary US-Iran war dimmed that outlook.

“There were 11 months of continuous disinflation,” Cardoso said, adding that the trend had strengthened expectations that “over a period of time, we would expect interest rates to begin to moderate.”

What to expect from the capital market in the next six months

Analysts say the second half is expected to be shaped by the Central Bank of Nigeria’s interest-rate decisions, third- and fourth-quarter corporate earnings, and exchange-rate stability, as well as the timing of anticipated listings such as Dangote Refinery and the Nigerian National Petroleum Company (NNPC).

Tunde Amologbe, the managing director of Arthur Steven Asset Management, said, “We had predicted at the beginning of the year that the market was going to do a 45 percent gain. The market has surpassed that. We are at 51 percent.”

“Our feeling is that ultimately we are likely to close at about this level by December 2026, probably at about 50 percent or just slightly below.”

“We are expecting relatively stable markets,” the Arthur Steven, chief, said, explaining that further gains would increasingly depend on corporate fundamentals rather than broad market momentum.

The optimistic market outlook is being supported by improving macroeconomic indicators.

Speaking in a recent interview, Segun Adams, a macroeconomic strategist at Afrinvest Research, said Nigeria’s economy has broadly performed in line with expectations despite disruptions from geopolitical tensions in the Middle East.

“The economy is moving in the direction we expected,” Adams said, citing stronger-than-expected GDP growth, improved exchange-rate stability, a stronger trade balance and Nigeria’s sovereign credit rating upgrade by S&P Global Ratings as evidence that reforms introduced since 2023 are beginning to gain traction.

Nigeria’s economy expanded by 3.89 percent in the first quarter of 2026, underpinned by stronger oil production and resilient non-oil sector growth despite tight monetary conditions, according to Afrinvest.

However, analysts cautioned that the same factors supporting markets could become headwinds in the months ahead.

Arthur Steven Asset Management said monetary policy, inflation, foreign exchange stability, and earnings performance would remain the biggest determinants of investor sentiment through the rest of the year.

Afrinvest has also revised its average inflation forecast for 2026 higher after renewed geopolitical tensions disrupted the earlier disinflation trend.

“The war disrupted that trajectory,” Adams said, noting that rising global energy prices temporarily reversed the moderation in inflation witnessed across many economies, including Nigeria.

Despite those risks, analysts remain broadly positive on Nigerian assets, citing stronger economic fundamentals than a year ago.

Arthur Steven Asset Management expects investors to continue favouring equities over other asset classes but advised regular portfolio rebalancing as market conditions evolve.

“The next phase of the market will require stronger earnings delivery, sustained macroeconomic stability, and continued policy consistency,” the firm said, adding that investors should pay close attention to monetary policy, inflation, and corporate performance as the market enters a more demanding second half.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp