By Paul Igbinoba

The consistent rebound of the naira in the foreign exchange market since March 2024 is the strongest indication yet that the Nigerian economy is beginning to experience a turnaround. But it is not yet celebration time, and there is still much work to be done. The government needs to remain steadfast and stay the course of reform to the end. But it must continue to prioritise measures to cushion the adverse effects of economic reforms on the poor and vulnerable groups.

Read also: Nigeria’s far-reaching macro-economic reforms and the changes in the electric power sector

The courageous decision to liberalise two key markets, the foreign exchange market and the market for petroleum products, led to a sharp depreciation of the naira and triggered pernicious inflationary pressure. A strategic reset of the outcomes of these two key markets also holds the key to the short-term turnaround of the economy.

Since the resumption of Mr Yemi Cardoso as the Governor of the Central Bank of Nigeria in early October 2023, the apex bank has unleashed an unprecedented combination of monetary policy measures to support the naira and fight inflation. These measures include: clearance of foreign exchange backlog obligations to banks and airlines, amounting to $7 billion; placing limits on banks’ Net Open Position, which was meant to limit the exposure of Nigerian banks to foreign exchange risks; removal of caps on international money transfer operations; discontinuation of the cap on the spread on interbank foreign exchange transactions and lifting of restrictions on the sale of interbank forex proceeds; implementation of a Price Verification System; removal of the daily cap of N2 billion on remunerable Standing Deposit Facility, and overhaul of the Bureaux De Change (BDCs), leading to the revocation of 4173 operators’ licences, and the weekly allocation of $10,000 to each of the remaining 1509 BDC operators; and the two successive hikes in the monetary policy rates (MPR) from 18.75 percent in January to 22.75 percent in February and subsequently to 24.75 in March, among a continuing series of unrelenting measures to shore up the value of the naira and fight inflation.

The eventual coming on stream of the behemoth, the 650,000 barrels per day Dangote petroleum refinery, is the second leg of the welcome development that has a great potential to turn around the economy and make a significant difference to the present economic narrative. The refinery has long been expected to make a huge impact on the economy, and the timing of the sale of its products, beginning with automotive gas oil, also known as diesel, could not have come at a better time. Aviation fuel is to soon follow, as well as premium motor spirit (PMS) in May.

Already, the price of diesel has crashed to N1200 per litre from N1700 per litre, which will eventually come down even further. One can imagine that by the end of the second quarter in June, the price of diesel would have sufficiently settled so as to make a tremendous impact on both transportation costs and the cost of production of goods and services in a manner that will considerably moderate the inflation rate, combined with the stabilisation in the exchange rate of the naira, to the relief of various stakeholders in the Nigerian economy.

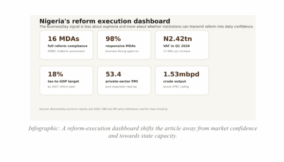

“On the whole, the government should be encouraged and supported to stay on course with economic reforms in the key markets of foreign exchange, downstream petroleum products, upstream gas markets, and electricity markets.”

These auspicious developments have, however, been punctuated by necessary but long-delayed reforms in the power sector. Recently, the Nigerian Midstream and Downstream Petroleum Regulatory Authority (NMDPRA) set the new price at which power-generating companies are to buy gas from upstream gas producers at $2.42 per million Metric British Thermal Units (MMBTU), up from $2.18 in 2021. The adjustment was necessary to encourage upstream producers to produce and supply enough gas to fire our thermal power plants. In a related development, the Nigerian Electricity Regulatory Commission (NERC) announced a 300 percent increase in tariff (which amounts to N225/kwh) for Band A electricity customers who are expected to get 20 hours of electricity per day, making them premium customers.

Read also: Nigeria economic reforms to accommodate foreign investors Tinubu

The increase in the price of gas by NMDPRA is in line with the Petroleum Industry Act, and the increase in electricity tariffs for premium energy consumers is in line with the long battle to enthrone cost-reflective tariffs in the Nigerian Electricity Supply Industry (NESI) to ensure improved power supply, liquidity, and long-term financial sustainability and profitability of power sector firms.

These are certainly hard economic decisions that the government and its agencies have to make at this difficult time. There are really no viable alternatives to these measures if we want the power sector to be turned around. There has been a barrage of criticism from a cross-section of stakeholders, understandably, especially from those who are hardest hit, particularly manufacturers. But also from political groups, who have been vitriolic in their criticisms without offering viable alternative solutions to getting Nigeria out of perpetual darkness. I think the most viable way to handle the challenge of high energy costs is through the sustainable use of energy to minimise waste, which is still cheaper than the use of diesel- and petrol-powered generators.

On the whole, the government should be encouraged and supported to stay on course with economic reforms in the key markets of foreign exchange, downstream petroleum products, upstream gas markets, and electricity markets.

The Nigerian economy has a huge potential for self-correction. But all stakeholders must, however, cooperate to ensure that the positive outcomes we all desire are realised.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp