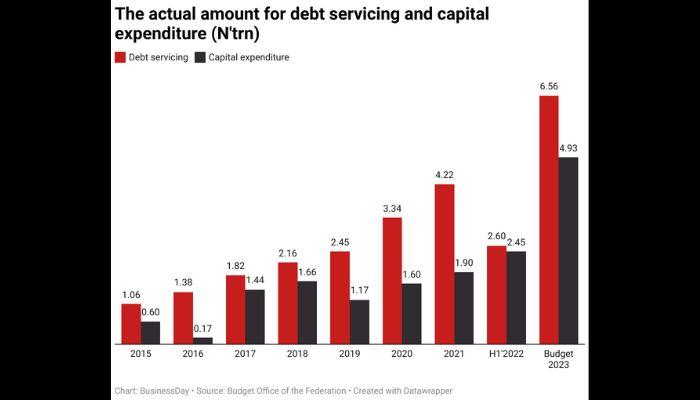

For every naira spent on capital expenditure (capex), Nigeria has spent nearly two times more servicing a ballooning debt stock since 2015, a trend that is partly to blame for the deepening poverty in the country of 200 million people.

Under President Muhammadu Buhari, who took charge of Africa’s largest economy in 2015, the federal government has spent N10.99 trillion on capital expenditure, according to data collated by BusinessDay from budget implementation reports up until the first half of 2022. In the same period, N19.03 trillion was spent repaying creditors, 73 percent more than capital expenditure.

Spending more on debt service than capital expenditure is not entirely new for Nigeria, despite being a developing nation with a gaping infrastructure deficit.

Data from the same Budget Office show that every year since 2015, the federal government has spent more money servicing debt than it has on badly needed infrastructure. That’s despite the government touting infrastructure spending as one of its main achievements.

The trend of spending more on debt service than capex, which is set to stretch for the ninth straight year, according to the 2023 budget proposal, could see the government spend N6.31 trillion, 75 percent higher than the amount in the 2022 budget and 50 percent more than the actual amount spent in 2021.

It gets even worse. The amount to be spent on debt service in 2023 translates to 65 percent of estimated revenues for the year (N9.73 trillion). That’s a better outlook than that of the International Monetary Fund, which forecast Nigeria’s debt service cost to equal 100 percent of revenues next year.

The spike in local and global interest rates has made the cost of borrowing jump this year and is likely to continue in 2023 as central banks try to tame rising inflation.

The government spent more than it earned to service debt in the first four months of 2022, according to official data.

A debt service-to-revenue ratio of 118 percent at the end of April (which implies that the debt service costs exceeded revenue by 18 percent) left the country with the worst debt service-to-revenue ratio in the world, according to the Economist Intelligence Unit.

Nigeria’s inability to pay creditors without having to borrow some more may well be the story for the whole of the year, with the World Bank predicting that debt service costs would exceed revenues by 2 percent (102 percent) at the end of 2022.

Analysis of budget implementation reports show that over 70 percent of Nigeria’s debt stock, which has more than tripled to N42.8 trillion as at June 2022 from 2015 levels, has gone to recurrent expenditure including debt servicing.

In that time, Nigeria’s infrastructure has not significantly improved and that has been pointed to by critics who say the government’s borrowing has not been impactful. The country still requires investment of $100 billion a year for 30 years to address its infrastructure deficit.

Much of that gap, which includes lack of good roads and a railway network that can drive economic activities, poor power generation, transmission and distribution systems, and dilapidated airports, remain largely unresolved despite the government’s debt binge and infrastructure spending.

Public-private partnerships (PPP) have not been useful. Private fund managers at a recent private equity event accused the government of not keeping contracts and failing to select the right projects for PPPs.

The huge debt service costs raise questions about debt sustainability, according to Ayodeji Ebo, managing director and chief business officer of Optimus by Afrinvest, as the majority of debts are directed toward non-productive areas like recurrent expenses.

“When a developing country with limited resources and a huge infrastructure deficit is spending so much on debt service and still subsidises petrol, electricity, etc., then it is digging a debt pit for itself,” Ebo said.

Low oil revenue, a major source of government earnings, has forced the federal government to rely on external and domestic borrowing to fund its projects and close budget deficits.

Read also: World Bank dashes hope of countries seeking debt relief

In a bid to tackle this infrastructure challenge amid low government revenues, the Central Bank of Nigeria (CBN) announced the creation of the Infrastructure Corporation (InfraCorp) in October 2021 (after it was approved by the President in February 2021) to boost funding for capital projects in the country.

The InfraCorp was established by the CBN in partnership with African Finance Corporation and the Nigerian Sovereign Investment Authority with a seed investment of N1 trillion. Funding is expected to grow to N15 trillion over the next few years and will be deployed to tackle critical infrastructure projects.

But the project is yet to get off the ground.

Buhari’s tax credit for infrastructure scheme has also sought to address the infrastructure deficit, with some large companies, including the Dangote Group, taking up the responsibility to fix roads in exchange for tax breaks.

Some of the presidential candidates vying for Nigeria’s top job in 2023 have all identified the rising debt levels of the government as a challenge. Atiku Abubakar, the candidate of the main opposition Peoples Democratic Party, described the country’s debt level as a “recipe for macroeconomic instability”, saying he would explore PPPs more if elected president next year.

Peter Obi, the candidate of the Labour Party, who has been critical of the government’s debt binge since 2019, said: “Nigeria must stop borrowing for consumption, but only borrow to invest in regenerative development projects and other productive ventures.”