Nigeria’s annual headline inflation moderated for the fourth consecutive month to 17.38% in July.

The divergence between the global and Nigerian inflation trends has been a subject of controversy in the last couple of months. A more disturbing fact is that the published data seems not to reflect market reality.

According to recent National Bureau of Statistics data, the consumer price index, (CPI) which measures inflation increased by 17.38 percent (year-on-year) in July 2021 representing a 0.37 percent rate moderation compared to the rate recorded in June 2021 (17.75 percent). This implies that prices continued to rise in July 2021 but at a slower rate than they did in June 2021.

On a month-on-month basis, the Headline index increased by 0.93 percent in July 2021. This was 0.13 percentage points lower than the rate recorded in June 2021 (1.06) percent.

The percentage change in the average composite CPI for the twelve months period ending July 2021 over the average of the CPI for the previous twelve months period was 16.30 percent, showing a 0.37 percent point rise from 15.93 percent recorded in June 2021.

The urban inflation rate increased by 18.01 percent (year-on-year) in July 2021 from 18.35 percent recorded in June 2021, while the rural inflation rate increased by 16.75 percent in July 2021 from 17.16 percent in June 2021.

On a month-on-month basis, the urban index rose by 0.98 percent in July 2021, down by 0.11 points against the rate recorded in June 2021 (1.09 percent), while the rural index also rose by 0.87 percent in July 2021, down by 0.15 points over the rate that was recorded in June 2021 (1.02 percent).

The corresponding twelve-month year-on-year average percentage change for the urban index was 16.89 percent in July 2021. This is higher than 16.51 percent reported in July 2021, while the corresponding rural inflation rate in July 2021 was 15.73 percent compared to 15.36 percent recorded in June 2021.

The composite food index rose by 21.03 percent in July 2021 compared to 21.83 percent in June 2021. This implies that food prices continued to rise in July 2021 but at a slower speed than they did in June 2021.

The rise in the food index was caused by increases in prices of Milk, Cheese and Eggs, Coffee, Tea and Cocoa, Vegetables, Bread and Cereals, Soft drinks, and Meat.

Read also: Equities lose N3bn as investors take profit on recent gains

On a month-on-month basis, the food sub-index increased by 0.86 percent in July 2021, down by 0.25 percent points from 1.11 percent recorded in June 2021.

The average annual rate of change of the Food sub-index for the twelve-month period ending July 2021 over the previous twelve-month average was 20.16 percent, 0.44 percent points from the average annual rate of change recorded in June 2021 (19.72) percent.

In Nigeria, analysts have attributed these current diverging trends to ‘the outside lag’ and ‘consumer price resistance’. The outside lag is the time lag between when policies are implemented and when the economy or markets begin to feel the impact.

In Q2, there was an increase in interest rates both in the interbank and T/bill markets and an increase in cash reserve ratio debits (a de facto tighter monetary policy). Consumer price resistance is also reflected in the NBS data, which revealed that 50% of Nigerians reduced their food purchases both in volume and value.

These trends thus indicate that Nigeria’s inflation rate has thus reached a point of inflection. This is consistent with the 1.28% decline in the global food price index to 123.0 points and the 3.02% drop in the AFEX commodity price index to 451.45 points in the month of July.

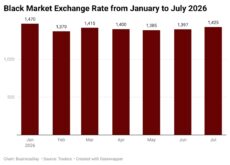

While consumer price inflation is expected to continue its downward trend, inflation risks remain elevated due to heightened insecurity in some of the food-producing states (which could limit the impact of the harvest), higher energy costs, and exchange rate pass-through. The naira weakened to a record low of N525/$ following the CBN‘s decision to discontinue the sale of forex to BDCs before appreciating by 1.9% to N515/$. Currency pressures and the difficulty in accessing forex have forced some manufacturers to resort to local substitutes, which is reducing supply to retail markets.

For instance, corn, which is usually in massive supply during the peak of the rainy season, witnessed scanty supply to retail markets this year. This is partly because it is used as a substitute for sugar in producing ethanol. The IMF’s SDR allocation ($3.35bn) and the impending Eurobond issue ($6.2bn) will boost forex supply and taper demand pressures in the near term.

Another factor likely to be contributing to this decline could be attributed to moderation in commodity price movement. A recent market survey in Lagos revealed a mixed commodity price trend. The varying price movements were largely attributed to produce perishability, logistics costs, and harvest.

The price of tomatoes declined sharply by 41.67% to N35,000/basket in July. Tomato is a highly perishable commodity due to its high water content. Hence, with supply increasing and inadequate storage facilities, sellers tend to lower prices to reduce post-harvest losses.

Another major factor influencing commodity prices in various markets is higher logistics costs. The farther the market is from the production point, the higher the cost of logistics and this reflects in commodity prices. The price of diesel, the principal fuel for logistics and distribution, surged by 23.95% to N295/liter.

The volatility in the prices of agricultural commodities is largely due to seasonality. During the harvest season, prices fall due to increased supply and vice versa. For instance, the price of a medium tuber of yam fell to N1,500 from N2,000 in the last two months. As the harvest season continues, pricing pressures are expected to further reduce.

Global inflation lately has posed itself to be a hydra-headed problem in the world. Most advanced and developing economies are reporting inflation rates higher than their targets. For instance, inflation in the US spiked to a 13-year high of 5.4% compared to a target of 2%. This is largely due to expenditure initiatives like infrastructure bill ($2trn), COVID stimulus package, and pandemic-related supply shocks. There is a raging debate as to whether inflation this time is transitory or structural. The comforting news is that price inflation without an increase in wages (wage inflation) tends to be transient.

With Q2 GDP numbers scheduled for release on August 26th, consensus forecasts range from 2.6%-3.2% due to base year effects. The sustained recovery in economic growth and moderation in inflation will further justify the MPC’s decision to maintain status-quo again in September.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp