Zainab Ahmed, Nigeria’s finance minister, in a media interview on the sidelines of the IMF/World Bank annual spring meetings, said Africa’s largest economy was exploring a debt restructuring for which advisers had been appointed, sparking fears that the West African nation may be on the path to a default.

Although she has since walked back the restructuring talk but investors are still somewhat uneasy.

Countries turn to debt restructuring when at risk of default on their sovereign debt due to severe cash flow constraints. The process of debt restructuring typically entails creditors or bondholders taking a haircut by agreeing to accept a reduced percentage of what they are owed.

The maturity dates on bonds can also be extended, giving the government (the issuer) more time to secure the funds it needs to repay its bondholders.

Ghana, Nigeria’s west African neighbour, is one country in talks with creditors to restructure its local currency debt due a severe financial crunch. The restructuring is likely to entail haircuts on principal and interest payments as well as extension of maturities, according to bankers familiar with the matter.

Ghana’s financial situation is dire. A senior director from global ratings agency, Fitch, said in September that a debt default was a “real possibility”.

Ghana’s total public debt as of June 2022 was $54.4 billion, 78.3 percent of GDP, up from $32.3 billion or 55.5 percent of GDP in 2017, according to central bank and finance ministry data.

Interest payments have been the government’s largest annual expense since 2019, and were its second-largest expense for five straight years prior to that, finance ministry figures show. Domestic debt accounts for more than 80 percent of that, which is why it is the target for restructuring.

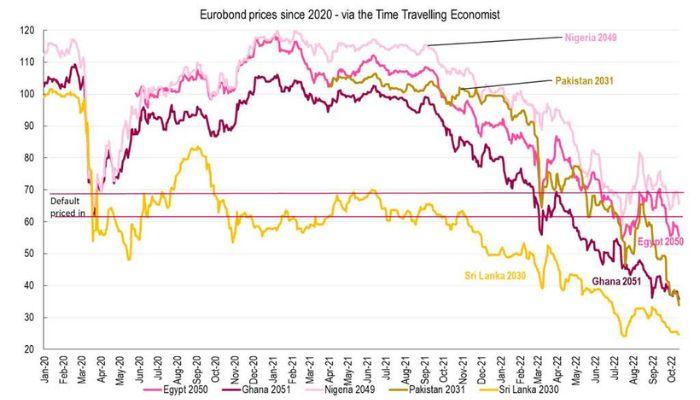

Ghana’s Eurobonds have traded at junk since news of the debt restructuring plans became public with its credit rating slipping to below investment grade. Its currency is one of the worst performers among African currencies this year, down by about 30 percent since January.

Fast forward to Nigeria and the interview where Finance Minister Ahmed spoke of a possible debt restructuring. The statement spooked investors and roiled the markets, with Nigeria’s Eurobond due in 2047 falling below 56 cents on the dollar. The naira also crashed to a new low.

Investors are now pricing in the risk of a possible default, like they have done with Ghana, following the minister’s statement.

However, is Nigeria set for a default, and did Ahmed really mean a debt restructuring, in the real sense of the term?

If Ghana’s example was anything to go by, Nigeria – though dealing with a financial crunch as well – is still in a better position than Ghana.

Unlike Ghana, Nigeria’s debt to GDP ratio is 23.1 percent although that understates the country’s revenue challenges. The IMF estimates that the country’s debt service costs would exceed revenues next year after gulping 86 percent in 2021.

Analysts who combed the entire interview also believe it is not the case that Nigeria may actually be planning a debt restructuring as the country was in no risk of a debt default.

Razia Khan, chief economist at Standard Chartered Bank, said there was nothing in the interview that Nigeria’s Finance Minister did that spoke to anything like a default and it was simply “an unfortunate use of the term.”

“For its overall debt portfolio, the FG is considering how to extend maturities (‘stretch out the repayments to longer periods’),” Khan said.

“To my mind, this is pretty standard – it isn’t really a restructuring. Moreover the FinMin made clear that Nigeria would only consider international capital market issuance when market conditions improve. It seems safe to conclude therefore that no ‘restructuring’ was intended,” Khan said.

A country planning a debt restructuring is unlikely to be thinking of raising even more debt from the international capital market.

The finance minister has since clarified her comments, saying the government was not planning to restructure the country’s debt but to renegotiate existing external loans to a more longer tenor to gain more time for repayment.

“My sense is that the only key development on Nigeria’s debt is the securitisation of CBN’s Ways & Means debt which has been talked about for years,” said Wale Okunrinboye, head of research at pension fund manager, Sigma Pensions.

“The mention of rollover (which the FGN does normally) and extending maturities (which might mean focus on longer dated debt) is not anything new. The red herring is ‘restructuring’ within the LCY context. Given the news out of Ghana naturally spooks everyone,” Okunrinboye said.

Read also: Nigeria at 62: Retired, broke and indebted

The finance minister’s clarification is important as there is a bond auction next week.

Beyond the restructuring talk, the minister’s comment is more reflective of Nigeria’s dire financial condition. Indeed if the country continues on its current path, it may not take long before a real restructuring is on the table.

Only three African countries have worse debt service to revenue ratios than Nigeria and two (Ethiopia and Zambia) have defaulted and the other is Ghana.

“FX reserves are sufficient to get the country through until the elections and I’d be a little surprised if they are so low that default is likely in 2023,” said Charles Robertson, global chief economist at Renaissance Capital.

“After the elections, Nigeria could cut the fuel subsidy, devalue the currency (boosting naira revenues from oil exports) and cut the fiscal deficit. The current account could improve, bringing in more dollars to the economy and so on. Potentially Nigeria could even change its views on the IMF, or at least use the re-allocated SDRs in the Resilience and Growth Trust,” Robertson said.

“So default is far from inevitable in Nigeria, but in the medium to long-term is a serious risk.

“Talking about re-profiling may be just a sensible way to push debt repayments into the future – or could be about the mix of local and external debt and moving more towards local when external markets are basically closed. But raising the issue shows that Nigeria is under pressure,” Robertson said.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp