Until everyone dies of hunger or social unrest erupts, and the authorities resort to using military power to quell it, only then will it be acknowledged that things are getting tougher in Nigeria and the economy is biting hard.

This sounds too harsh or like an attack on the government, right? Well, that is the reality!

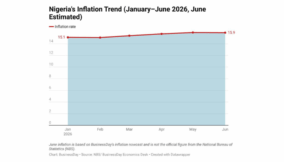

Every day Nigerians are facing an increasingly desperate situation as food prices soar beyond reach—food inflation has risen to 40.66 percent from 40.53 percent, as reported by the National Bureau of Statistics (NBS). Wages remain stagnant, and insecurity disrupts daily life.

Families are forced to make impossible choices between feeding their children and paying for essential services like healthcare and education.

“Families are forced to make impossible choices between feeding their children and paying for essential services like healthcare and education.”

The price of basic food items like tomatoes has skyrocketed to 1,000 Naira for just four small pieces, forcing many to resort to alternatives like carrots and cucumbers in their cooking of soup or stew, BusinessDay survey shows. This is not a sustainable way of living; it’s a clear indication of an economy in distress.

Moreover, the public health crisis is intensifying. The Nigeria Centre for Disease Control and Prevention (NCDC) has reported alarming numbers of cholera cases, aggravated by inadequate waste disposal and flooding during the rainy season.

The high cost of medicine further exacerbates the situation, compounded by the departure of major pharmaceutical companies to other countries, rendering essential drugs inaccessible to many. This dire scenario underscores the urgent need for effective healthcare solutions.

Insecurity remains a critical factor that demands immediate attention. You cannot downplay or politicise security issues and expect the food crisis to resolve itself—it’s simply impossible.

The term “politicise” is used here because it seems that addressing insecurity is a complex challenge, given its profound impact on the economy despite Nigeria’s significant military presence. Insecurity persists unabated, affecting daily life.

There exists a direct correlation between food supply chains and security. When security deteriorates, supply chains are inevitably disrupted, although other factors also play a role. Currently, farmers in northern Nigeria are unable to tend to their fields due to threats of violence. Some even resort to paying militias for protection just to access their farms.

It’s crucial to stress that I anticipate no decrease in food prices in the near future. Why? Insecurity significantly shapes supply chains in Nigeria, exerting substantial influence on pricing dynamics.

Furthermore, with the onset of the rainy season, the threat of floods will exacerbate existing challenges, further disrupting already vulnerable supply lines—an ex-ante consideration.

Globally, we’ve seen how conflicts like the Russia-Ukraine war can impact food prices, underscoring the interconnectedness of security and economic stability.

The government must recognize the urgent need for a cohesive and effective economic strategy. Without decisive action and clear direction, the country faces an escalating crisis that could lead to severe social unrest and further economic collapse.

Let me digress a little. Linear expansivity, a concept from physics describing how materials expand under heat, offers a metaphorical link to Nigeria’s situation. Just as materials have limits to their expansion before they break, so do people’s resilience and endurance under prolonged hardship.

Nigerians cannot endure indefinitely under the current economic strain, just as a material cannot expand infinitely. The continuous pressure of rising prices, stagnant wages, and insecurity is pushing Nigerians to their limits.

The government must act swiftly and decisively to alleviate these pressures before the situation reaches a breaking point. Delayed action risks exacerbating social unrest and deepening economic woes, further jeopardising the well-being of the nation and its people.

Lessons from similar countries

India: Gradual Removal of Fuel Subsidies and Broader Economic Reforms

India provides a pertinent case study on the gradual removal of fuel subsidies and its broader economic reforms. Recognizing the fiscal burden posed by subsidies, the Indian government initiated a phased approach to subsidy removal, aiming to cushion the impact on its economy and population.

A critical component of this strategy was the introduction of direct cash transfers to the most vulnerable households. The Direct Benefit Transfer (DBT) scheme, implemented in 2013, was a game-changer.

By directly transferring subsidy benefits to the bank accounts of beneficiaries, the government ensured that the poorest segments of the population were protected from the immediate price shocks associated with subsidy removal.

This approach not only helped manage inflation but also improved the efficiency and targeting of subsidies, reducing leakages and corruption. As of 2023, the DBT scheme continues to be a cornerstone of India’s social protection strategy, benefiting millions of households across the country.

Moreover, India has invested significantly in expanding its social safety nets. Programs such as the Mahatma Gandhi National Rural Employment Guarantee Act (MGNREGA) provide rural employment and income support, thereby mitigating the adverse effects of rising fuel prices on rural households. MGNREGA guarantees 100 days of wage employment per year to rural households, enhancing their income security and contributing to rural development.

In addition to MGNREGA, the Pradhan Mantri Garib Kalyan Anna Yojana (PMGKAY) was introduced during the COVID-19 pandemic to provide free food grains to poor families.

This programme has been extended multiple times to ensure food security for vulnerable populations, demonstrating the government’s commitment to supporting its citizens through economic hardships.

India’s economy has shown remarkable resilience and growth in recent years. Despite global economic uncertainties, India’s GDP growth rate is projected to remain robust.

According to the International Monetary Fund (IMF), India’s GDP growth is expected to be around 6.1 percent in 2023 and 6.8 percent in 2024, driven by strong domestic consumption and investment.

Inflation has been a concern for India, especially due to global supply chain disruptions and rising commodity prices. However, the Reserve Bank of India (RBI) has been proactive in managing inflation through monetary policy measures.

The RBI has adopted a balanced approach, adjusting policy rates to control inflation while ensuring that economic growth is not stifled. As of mid-2023, the Consumer Price Index (CPI) inflation rate stands at around 5 percent, within the RBI’s target range.

Egypt: Currency devaluation and economic reforms

In 2016, Egypt embarked on economic reforms with IMF support, including floating the Egyptian pound to address foreign exchange shortages and boost investor confidence.

This move initially caused a sharp rise in inflation, adversely affecting the poor. To counter these effects, Egypt expanded its “Takaful and Karama” programs, providing cash transfers to over 3.5 million families by 2023, as reported by the Ministry of Social Solidarity.

Enhanced food subsidies also ensured affordability for basic necessities. Structural reforms improved the business climate, streamlined regulations, and attracted foreign direct investment, which reached $8.6 billion in 2022, according to the World Bank.

Fiscal measures like VAT introduction and energy subsidy reductions improved budget sustainability. Infrastructure projects, including Suez Canal expansion, bolstered economic competitiveness.

Recently, Egypt is on track to break with past practices and allow its currency to float in line with IMF-backed reforms. However, the structural changes necessary to pull the country out of a cycle of bailouts seem less likely.

After two years of chronic foreign currency shortages, Egypt has secured a significant amount of funding since late February, including $24 billion for a UAE project to develop a city on the Mediterranean coast and more than $15 billion from the International Monetary Fund, European Union, and World Bank.

Lessons for Nigeria

Several countries have faced similar economic crises and their experiences can offer valuable lessons for Nigeria:

Implement direct cash transfers to vulnerable households

Like India’s DBT scheme, Nigeria should introduce direct cash transfers to protect the poorest segments from price shocks associated with subsidy removal. This approach will help manage inflation, reduce corruption, and ensure that subsidies are efficiently targeted. The bottleneck here is the lack of sufficient data capturing the number of vulnerable people in Nigeria.

Expand social safety nets

Nigeria should invest in social safety nets similar to India’s MGNREGA, providing rural employment and income support to mitigate the adverse effects of economic reforms on rural households. Programs that ensure food security for vulnerable populations, such as food grain distribution during crises, should also be prioritised.

Strengthen economic reforms and business climate

Following Egypt’s example, Nigeria should implement structural reforms gradually, considering the ripple effects, to improve the business climate, attract foreign direct investment, and enhance fiscal sustainability.

Streamlining business regulations, reducing bureaucratic red tape, and ensuring a stable macroeconomic environment will be crucial in achieving long-term economic stability and growth.

Open borders and introduce food subsidies

Additionally, opening borders for the importation of food at cheaper rates and introducing food subsidies will have positive effects on the vulnerable population.

This approach can help lower food prices, alleviate food insecurity, and provide immediate relief to those most affected by rising inflation and economic hardship.

Oluwatobi Ojabello, senior economic analyst at BusinessDay, holds a BSc and an MSc in Economics as well as a PhD (in view) in Economics (Covenant, Ota).

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp