Inflation gets a bad rap in economic circles, but is it really the villain it’s made out to be? The idea that inflation always spells trouble isn’t entirely accurate. In fact, moderate inflation can have both upsides and downsides, and seeing the bigger picture is key to making smart economic decisions and shaping public opinion.

The usual story goes like this – prices go up, and suddenly, everything gets more expensive. Your money doesn’t stretch as far, your savings take a hit, and the economy gets shaky. But hold on a minute – it’s not that simple. Inflation is more nuanced than that, and its effects can vary depending on the situation.

In reality, moderate inflation can actually spur economic growth in specific circumstances. Moderate inflation typically ranges from 3 percent to 10 percent.

For example, the Federal Reserve of the United States establishes annual inflation rate targets of around 2 percent, believing that a gradual rise in prices helps maintain profitability for businesses and encourages consumers to make purchases without waiting for lower prices. Some experts even argue that one of inflation’s main roles is to prevent deflation.

This notion resonates with the views of John Maynard Keynes, a prominent economist, who argued that a certain level of inflation was essential to avoid the Paradox of Thrift.

According to this concept, if consumer prices continuously decline due to increased productivity, consumers tend to delay their purchases in anticipation of better deals. Consequently, aggregate demand diminishes, resulting in reduced production, job losses, and economic stagnation.

In the same vein, a report from Forbes, while inflation can erode the purchasing power of money over time, economists generally argue that a low, steady level of inflation is essential for fostering economic growth.

But how can inflation be seen as beneficial? To understand this, let’s consider its opposite: deflation. In a deflationary scenario, prices of goods and services gradually decrease, while the value of money increases. This means consumers can buy more with the same amount of money they had before.

On the surface, this might sound like a good thing. However, deflation can bring about negative consequences. When prices fall, it often indicates a decrease in demand for goods and services and an increase in supply, which further drives prices down. This trend may reflect consumer pessimism about the economy, leading to reduced spending and increased hoarding of cash.

Over time, deflation can hamper the production of goods and services, resulting in layoffs and rising unemployment rates. Some economists argue that deflation poses an even greater risk to an economy than inflation does.

While it’s clear that moderate inflation can have both positive and negative effects, a deeper understanding of its impact often requires a historical perspective. By investigating past instances of moderate inflation and its effects on economic growth, this piece provides valuable insights into how inflation has been managed and its implications for various economic indicators.

Let’s delve into historical case studies from different countries and time periods to explore the nuanced relationship between moderate inflation and economic growth and other indicators.

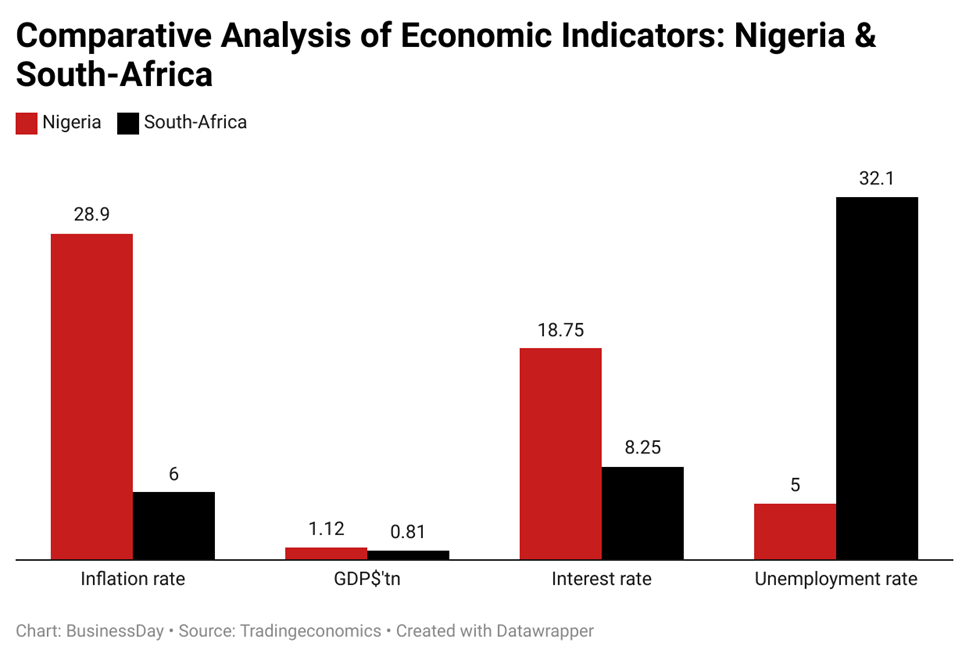

Regrettably, Africa’s two largest economies, Nigeria and South Africa, seem to be operating in opposite economic directions, creating a complex economic narrative.

It becomes evident that the impact of inflation is nuanced and varies across different contexts. Nigeria’s staggering inflation rate of 28.9percent as reported by National Bureau of Statistics (NBS) is juxtaposed with its relatively modest GDP of $1.115 trillion.

Despite its high inflation, Nigeria maintains a substantial GDP, indicating that inflation does not necessarily hinder economic output. Conversely, South Africa’s inflation rate of 6 percent aligns more closely with conventional expectations of moderate inflation, yet its GDP is notably smaller at $0.812 trillion. This contrast underscores the complex relationship between inflation and economic growth.

Furthermore, both countries grapple with high unemployment rates, with South Africa facing a particularly alarming rate of 32.1 percent. This suggests that inflation alone does not dictate a country’s employment prospects, as other factors such as structural issues and policy frameworks play significant roles.

The juxtaposition of these economic indicators challenges the simplistic narrative that high inflation inevitably leads to economic downturns. Instead, it underscores the importance of considering a range of factors, including GDP, interest rates, and unemployment rates, to fully understand the economic implications of inflation.

Abayomi Fashina, a risk analyst, emphasised that African nations face a daunting journey in harmonising their macroeconomic indicators to exert positive influences on other variables. He underscored the prevailing opposite trajectories observed in the continent’s two largest economies as indicative of the substantial challenges ahead in achieving economic coherence across the region.

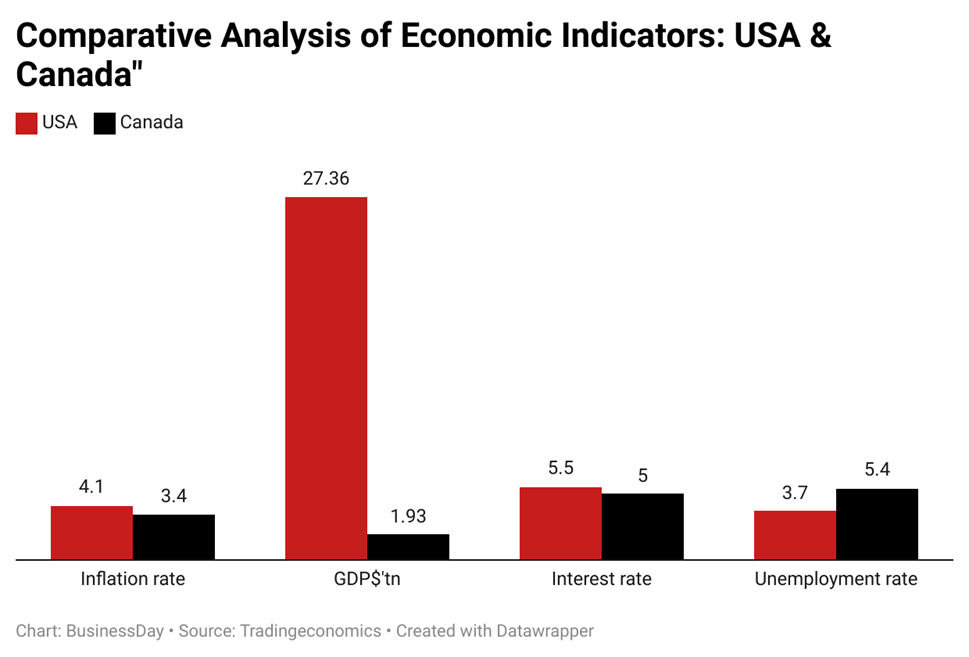

Contrary to popular belief, inflation does not always spell economic trouble. The juxtaposition of inflation rates between the United States (USA) and Canada provides an interesting perspective. The USA, with an inflation rate of 4.1 percent, boasts a significantly higher GDP of $27.36 trillion compared to Canada’s $1.928 trillion. Despite a slightly lower inflation rate of 3.4percent, Canada’s GDP is notably smaller.

This indicates that moderate inflation can coexist with robust economic growth, as evidenced by the USA’s thriving economy. Furthermore, both countries maintain relatively low-interest rates of 5.5 percent and 5 percent, respectively, suggesting that their monetary policies are conducive to economic stability. However, the unemployment rates present a nuanced picture.

While the USA reports a lower unemployment rate of 3.7 percent, Canada struggles with a slightly higher rate of 5.4percent. This discrepancy underscores the multifaceted nature of economic indicators and the need for comprehensive analysis when evaluating the impact of inflation.

Overall, the data challenges the notion that inflation is inherently detrimental, highlighting the importance of considering broader economic factors in assessing its implications.

A closer look at Germany and France’s economic indicators challenges the notion that inflation always spells trouble. Despite both countries experiencing moderate inflation rates, Germany’s stands at 5.9 percent, slightly higher than France’s 5.7 percent. Yet, Germany boasts a significantly larger GDP of $4.509 trillion compared to France’s $3.145 trillion. This suggests that inflation doesn’t necessarily hinder economic growth, as seen in Germany’s robust GDP.

Germany also maintains a lower interest rate of 2.1 percent compared to France’s 4.5 percent. This lower rate may stimulate investment and borrowing, supporting economic expansion despite inflationary pressures. Conversely, France’s higher interest rate could pose challenges for businesses and consumers, potentially slowing economic activity.

Both countries face unemployment, with Germany’s rate at 5.7 percent and France’s notably higher at 7.5 percent. While inflation may influence employment dynamics, other factors such as labour market policies and economic structure also play significant roles.

The comparison between Germany and France’s economic indicators highlights the complexity of inflation’s effects. It underscores the need for a nuanced understanding of economic factors beyond inflation rates to accurately assess their implications.

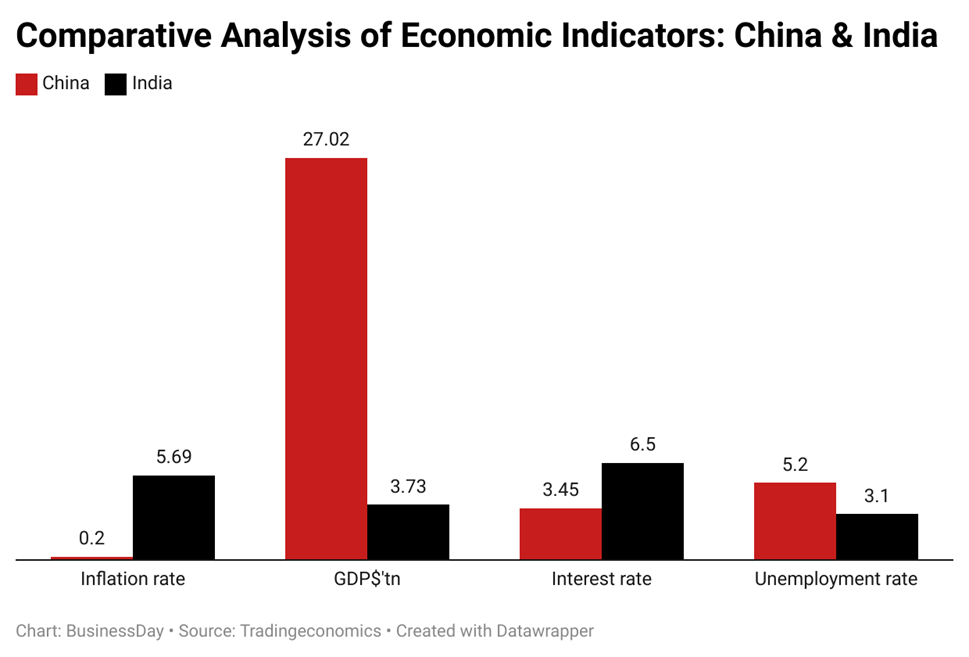

Examining China and India’s economic indicators challenges the conventional wisdom surrounding inflation. China maintains a remarkably low inflation rate of 0.2 percent, while India’s stands at 5.69 percent, indicating divergent inflationary pressures.

Despite this disparity, both countries demonstrate significant GDP figures, with China boasting $27.02 trillion and India at $3.73 trillion. These figures suggest that moderate inflation does not necessarily impede economic growth, as evidenced by China’s robust GDP despite its minimal inflation rate.

Additionally, China maintains a relatively low-interest rate of 3.45 percent, which may promote investment and economic activity. Conversely, India’s higher interest rate of 6.5 percent could present challenges for borrowing and investment, potentially affecting economic expansion.

Both countries also contend with unemployment, with China’s rate at 5.2 percent and India’s notably lower at 3.1 percent. While inflation may influence employment dynamics, various factors such as labour market policies and economic structure contribute to unemployment rates.

The comparison of China and India’s economic indicators underscores the complexity of inflation’s effects and challenges the notion that inflation always spells trouble. It emphasises the need for a nuanced understanding of economic factors beyond inflation rates to accurately assess their implications.

Mikel Ariyibi, a public sector analyst, gives his opinion: “I understand the concerns surrounding inflation and its potential impact on everyday life. While high inflation rates can indeed pose challenges for individuals and businesses alike, it’s essential to recognize that not all inflation is inherently harmful. In fact, moderate inflation can often be a sign of a healthy, growing economy.”

Mikel added, “A moderate inflation can have several positive implications. It can stimulate economic activity by encouraging consumer spending and investment. When prices rise gradually, consumers are incentivized to make purchases sooner rather than later, which can drive demand for goods and services. This increased consumer spending can, in turn, spur business growth, job creation, and overall economic expansion.

Moreover, moderate inflation can also help prevent stagnation and deflation, which can be far more detrimental to an economy. Inflation encourages businesses to invest in innovation and expansion to keep pace with rising costs, leading to greater productivity and competitiveness in the long run.”

“However, it’s crucial to ensure that inflation remains within manageable levels to avoid its negative consequences. Excessive inflation can erode purchasing power, reduce real incomes, and create uncertainty, particularly for those on fixed incomes or with limited savings. Therefore, policymakers must strike a delicate balance, implementing measures to control inflation while also fostering sustainable economic growth.”

“Ultimately, while inflation may have its drawbacks, it’s not inherently evil. When managed effectively and kept at moderate levels, inflation can serve as a catalyst for economic vitality and progress, benefiting individuals, businesses, and society as a whole.”

In the instance with Mikel, Oluwatobi Abisoye echoed the sentiment that inflation isn’t always the bad guy it’s cracked up to be. When kept in check, a little inflation can be just the push the economy needs to get things moving. But let’s not get too carried away – too much of a good thing can quickly turn sour. As with everything in economics, it’s all about finding that delicate balance.

Oluwatobi Ojabello, senior economic analyst at BusinessDay, holds a BSc and an MSc in Economics as well as a PhD (in view) in Economics (Covenant, Ota).

Wasiu Alli is a business and finance journalist at BusinessDay who writes about the economy, business trends, and politics. He holds a BA. Ed. and M. Ed. in English Language and Education.

Oluwatobi Ojabello, PhD, is a dynamic and multi-dimensional Assistant Editor for Economy and Markets with over two years of professional journalism experience. He delivers authoritative, data-driven coverage of fiscal policy, financial institutions and capital markets, using clear analysis to explain Nigeria’s most complex economic developments. His work focuses on macroeconomic policy, financial stability and corporate performance, turning technical issues into accessible narratives that inform both experts and everyday readers.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp