The World Bank economic team at the recently concluded Nigerian Economic Summit stirred controversy by stating that Nigeria has to stay the course of reforms for the next 10-15 Years to achieve any meaningful results. They also went further to endorse the government’s economic reform program and pledged support.

We do not agree with the World Bank’s position and timeline. The pronouncements are not backed by credible research or evidenced by data sets in its latest Nigerian economic report.

It is however time for a reality check, as the control levers for economic growth and development rest firmly in the hands of the Nigerian government.

The reform program, while commendable, has not been implemented properly. The cart was put before the horse. This led to a free fall of the currency, resulting in a 200% devaluation, and a surge in inflation and money supply. The outcome of the reforms and failure of the social intervention program is an Economic Reform Quagmire. It is therefore time for the government to hit the reset button, as it will take at least another budget cycle to achieve economic stability.

Nigeria has to permanently resolve its vulnerability to oil price fluctuations. It must emulate other oil-producing nations like Norway, with a US$ 1.6 trillion sovereign wealth fund. Last year, the Norwegian fund delivered US$213 billion in profits.

In our Nigeria 2024 year-end economic review, we stated that: “Q2 GDP growth at 3.19% is marginal with the July headline inflation easing from 34.19% to 33.40%. The trajectory of growth and inflation (not yet optimal) but in the desired direction allays the fears of recession and affirms the orthodox monetary policy stance of the CBN.

This is amidst the background of a 75% yearly increase in money supply to a record =N=100tn. Nigeria’s fiscal situation improved with revenue to debt service reduction by 30%, with technology deployments improved revenue collection.

However, the total debt burden of N121tn remains a challenge, as the 2024 budget debt service of N8.27tn exceeds both recurrent and capital expenditure. The supplementary budget will also increase the deficit from N10.4tn to N19.4tn.

” Since then, the downward inflation trajectory has reversed, due to the recent month-on-month spike to 32.70 percent from 32.25 percent, as a result of an increase in fuel prices. This will undoubtedly signal MPC for a further rate increase at the November meeting.

Data evidence also suggests that the CBN will not meet its inflation target of 24 percent by year end. In the light of these developments; fiscal challenges, suboptimal growth at 3 percent, declining productivity, high unemployment and failure to address growth strategies to move the Nigerian economy out of stagflation to a path of sustainability, we are hereby reviewing our forward guidance.

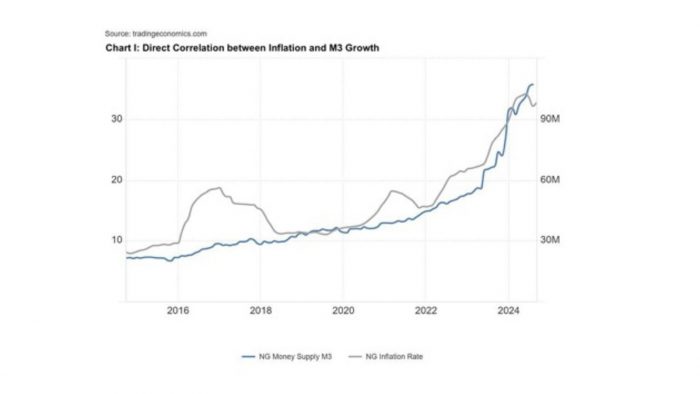

Our concern starts with the 100% increase in money supply in the past year to 107 trillion naira by August 2024. Our analysis Chart I shows a direct correlation over the last 10 years between the increase in money supply and a spike in inflation.

We are therefore concerned; that the CBN via Open Market Operations OMO, has mopped up 7.3 trillion naira in the last nine months, increased CRR from 32.5-50% and nearly 900 basis points MPR increase from 18.75-27.25% both in the past year, without significant decrease in the growth rate of both inflation and money supply.

The expected 20 trillion naira 2024 budget deficit will further exacerbate the situation.

Inflation reduction must remain a priority despite the manufacturing sector lobby group’s opposition to CBN’s tightening stance. Real rates are also currently negative.

Chart II Research over ten years projects an inverse relationship between GDP growth and Inflation. To achieve sustained GDP growth north of 8.5%, the historical data analysis proves that inflation must be at 12% or below.

Our benchmark exchange rate recommendation for year-end 2024 has been validated by events at =N=1,500-1,800/US$. However, for planning and budgetary purposes, our 2025 benchmark has been shifted to =N=1,800-2100/US$ as a result of the concerns we raised and the adverse impact on the economy.

Our views will change if we see a serious effort to restore fiscal discipline, sell down oil assets and ramp up oil production. The Silver Bullet for Nigerian Economic Recovery and Growth, are fiscal discipline, ramping up oil production and the sell down of oil assets to raise US$ 50 billion. The proceeds can be deployed to ease the debt burden and refinance NNPC. This will boost revenue and FX availability for the nation. In our opinion, this is long overdue.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp