Three years after Nigeria ended one of Africa’s largest fuel subsidies, the country’s finances look healthier than they have in years. Government revenues have surged. States are receiving record allocations. Investors have returned. Yet for millions of Nigerians, one question remains unanswered: Did the promised subsidy dividend ever arrive?

When President Bola Tinubu declared that “fuel subsidy is gone” in his May 2023 inaugural address, he set in motion the dismantling of a policy that had distorted Nigeria’s public finances for decades. The reform was widely judged unavoidable. The scheme consumed trillions of naira each year, disproportionately benefited higher-income households that consumed more fuel, encouraged large-scale smuggling into neighbouring countries where petrol was more expensive, and was repeatedly linked to inflated and fraudulent claims documented by official inquiries. Resources that could have financed roads, hospitals and schools were instead used to keep petrol prices artificially low.

The bargain offered to Nigerians was explicit: accept immediate economic pain, and the savings would be redirected to infrastructure, education, healthcare and social protection. The reform was also expected to reduce borrowing, curb corruption and strengthen investor confidence. Three years later, the subsidy has gone. The real test is whether the promised dividend followed it. That question can be answered only by examining what happened to public finances and whether those gains translated into visible improvements in citizens’ lives.

Why the policy had to change

By 2023, the subsidy had become one of the largest recurrent lines in the federal budget. The World Bank estimated petrol subsidies at about N4 trillion in 2022, and budget projections suggested the bill could have exceeded N6 trillion in 2023 had the programme continued, at a time when debt-service costs were consuming almost all retained federal revenue.

The economic case for removal was reinforced by its distributional logic. Because higher-income households consume more fuel, they captured the largest share of the benefit, making the subsidy an inefficient instrument for supporting the poor. The International Monetary Fund, the World Bank, and the African Development Bank had argued this point for years. The World Bank later put the fiscal gain from removal at about 2.6 percent of GDP in 2024, one of the largest single improvements to Nigeria’s fiscal position in recent memory.

The fiscal case worked

On the public finance test, the reform delivered. Government revenues rose sharply, FAAC allocations reached record levels, and fiscal pressures eased. Pump prices moved toward import parity almost immediately and were pushed higher still by exchange-rate liberalisation. Gross revenue collected by Nigeria’s major revenue agencies rose from N16.5 trillion in 2023 to N29.5 trillion in 2024, reflecting the combined effect of subsidy removal, a unified naira, and stronger collection.

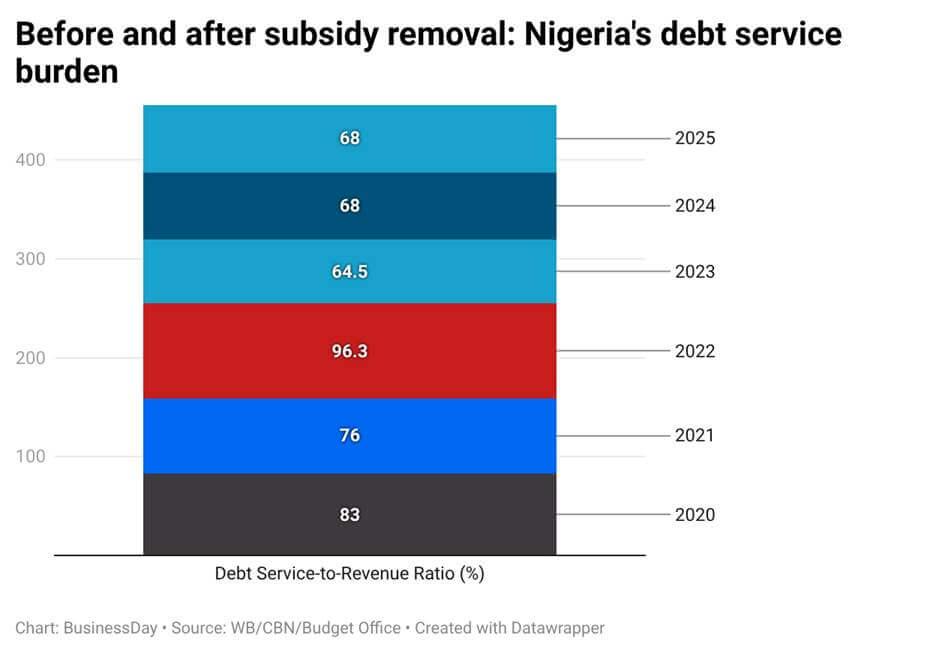

The consolidated fiscal deficit narrowed from about 5.4 percent of GDP in 2023 to roughly 3.0 percent in 2024, and the debt-service-to-revenue ratio fell from 96.3 percent in 2022 to 68 percent in 2024 as revenues climbed, according to World Bank data.

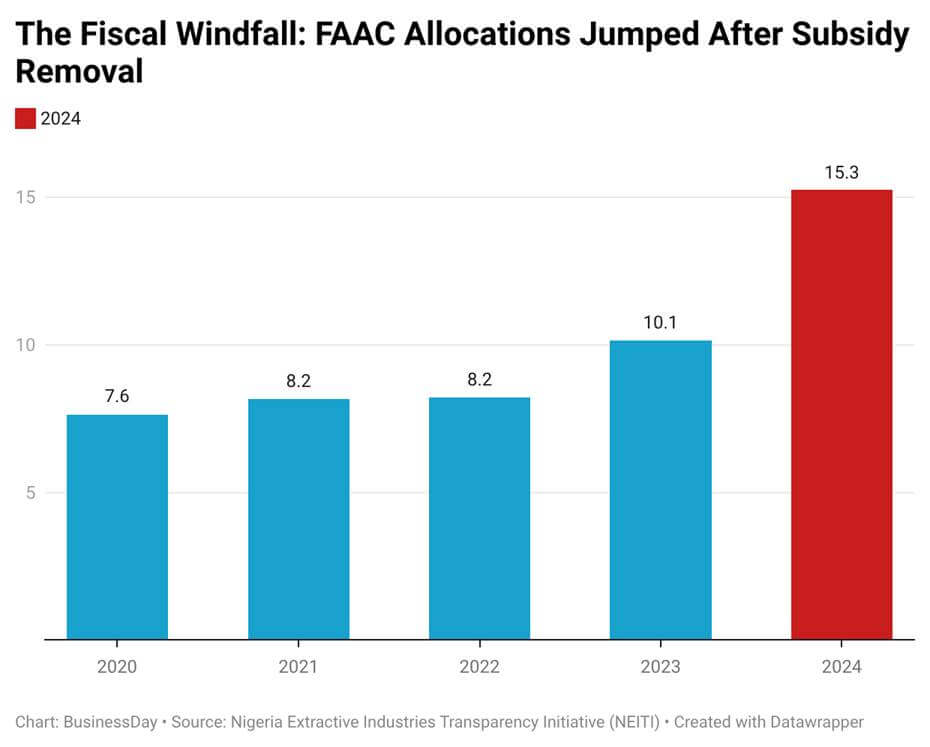

Higher Federation revenue flowed to all three tiers of government. Federation Account Allocation Committee (FAAC) distributions increased from N10.14 trillion in 2023 to N15.26 trillion in 2024, a 50.5 per cent jump in a single year, compared with N8.21 trillion in 2022 and N7.64 trillion in 2020. Several states subsequently recorded their highest allocations on record, strengthening their capacity to pay salaries, reduce borrowing and finance capital projects. Some appear to have converted this fiscal windfall into measurable development outcomes. Governors of Enugu, Katsina, Adamawa, Borno and Jigawa, among others, received recognition at the 2026 BusinessDay States Competitiveness and Investment Readiness Awards (SCIRA) for improvements in infrastructure, agriculture, internally generated revenue and public sector reforms. While the awards do not prove causation, they suggest that stronger fiscal resources, when matched by effective governance, can translate into better development outcomes.

Markets responded in kind. Fitch revised Nigeria’s outlook to positive and Moody’s upgraded the sovereign rating from Caa1 to B3. Nigeria also returned to the Eurobond market in late 2024 with an order book several times the size of its issuance, while the current account swung to a surplus of about $17.2 billion, equivalent to roughly 9 percent of GDP.

By every standard fiscal indicator, the policy created room that did not exist before. Fiscal space, however, is not the same as fiscal transformation. That distinction is where the debate now sits.

Measured against its original objectives, the reform produced mixed results. It clearly improved public finances, reduced fiscal leakages, strengthened investor confidence and created additional budgetary space. Yet the objectives that mattered most to households, better public services, stronger social protection and improved living standards, have been harder to identify. The policy therefore succeeded on its fiscal objectives faster than it succeeded on its social ones.

The transmission gap

The most important qualification came not from critics but from the World Bank. Although the implicit subsidy was only fully removed in October 2024, the Nigerian National Petroleum Company Limited began transferring the resulting gains to the Federation Account only in January 2025, and then remitted about half, retaining the balance to offset legacy obligations. Of roughly N1.1 trillion in relevant revenue in 2024, only about N600 billion reached the Federation Account.

The accounting treatment may be legitimate. The challenge is that the increase in public revenues did not automatically translate into visible improvements in public services. Despite FAAC allocations rising to a record N15.26 trillion in 2024, many Nigerians still struggle to identify projects, services, or social programmes directly linked to the savings from subsidy removal. The signalling problem is not. Citizens were asked to absorb a large and immediate shock on the understanding that the savings would fund visible development. When a substantial share is absorbed by arrears before it reaches the Federation, the link between sacrifice and benefit becomes difficult to trace, and that weakens public confidence in the reform even where the books ultimately balance. Transparency, in other words, is not a presentational nicety. It is the mechanism through which a difficult reform retains its mandate.

The cost was immediate, the relief was slower

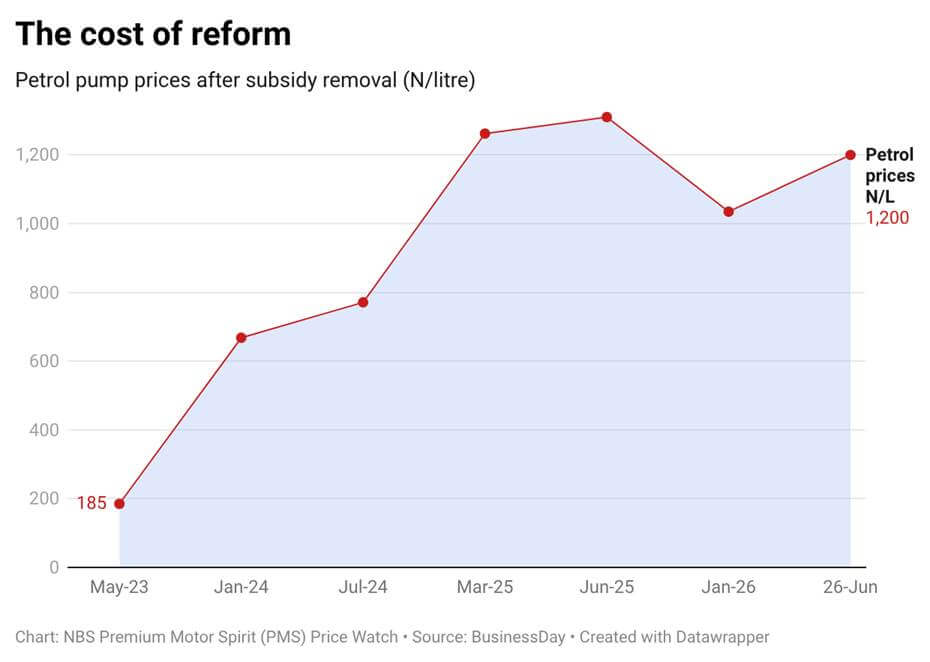

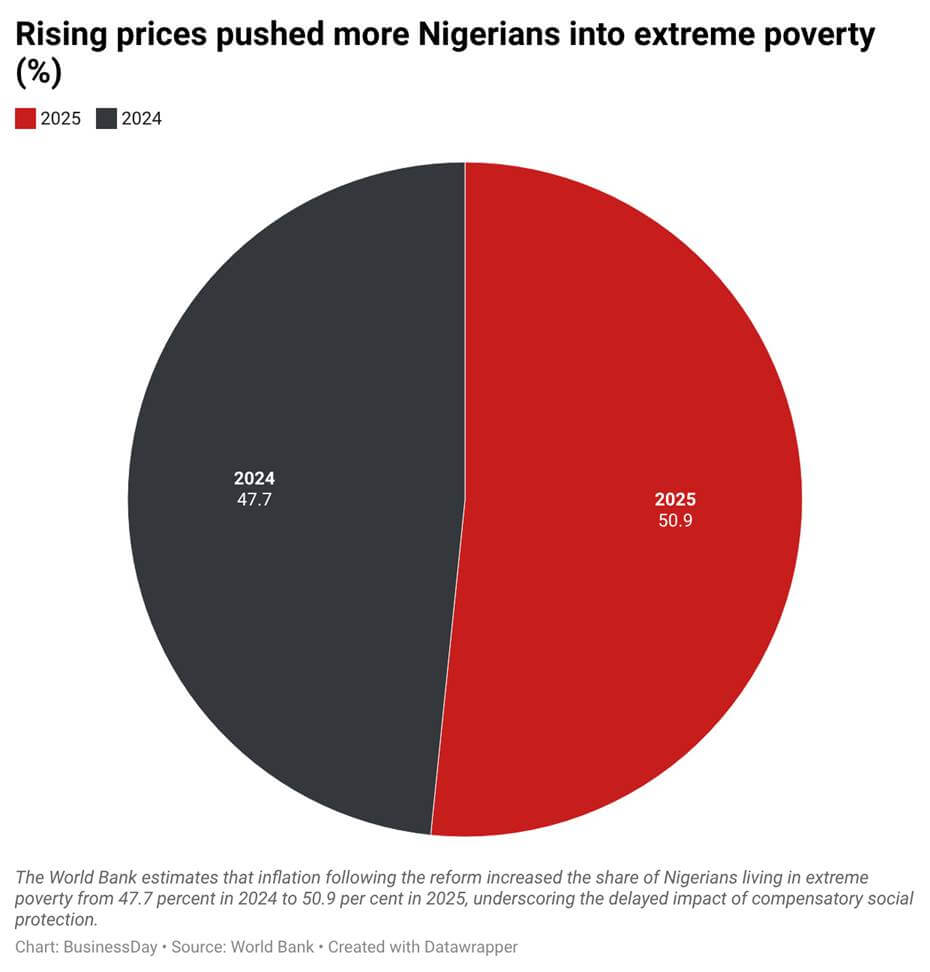

The adjustment was rapid, and its early incidence fell hardest on households. Average petrol prices rose from about N185 per litre before deregulation to roughly N668 by January 2024 and peaked above N1,260 in early 2025, before easing towards N1,050 by early 2026 as increasing output from the Dangote Refinery reduced Nigeria’s dependence on imported fuel. That relief proved temporary. Rising geopolitical tensions in the Middle East, particularly concerns surrounding disruptions to shipping through the Strait of Hormuz, pushed crude oil prices higher and drove domestic pump prices above N1,300 per litre between March and June 2026. Prices have since moderated but remain above N1,200 per litre, underscoring Nigeria’s continued exposure to global energy market shocks. Transport and food prices tracked fuel costs upward. Annual average inflation reached about 31 percent in 2024, and the World Bank estimates that rising prices increased extreme poverty from 47.7 percent of the population in 2024 to 50.9 percent in 2025.

Sequencing made the pain sharper than it needed to be. Countries that have successfully removed energy subsidies, including Indonesia and Brazil, generally scaled targeted cash transfers before or alongside the price adjustment. Nigeria attempted both reforms almost simultaneously, during a period of already elevated inflation. The compensating cash-transfer programme, designed with support from the World Bank, had reached about 5.5 million of a targeted 15 million households by early 2025. The pain arrived faster than the relief.

Who gained and who paid

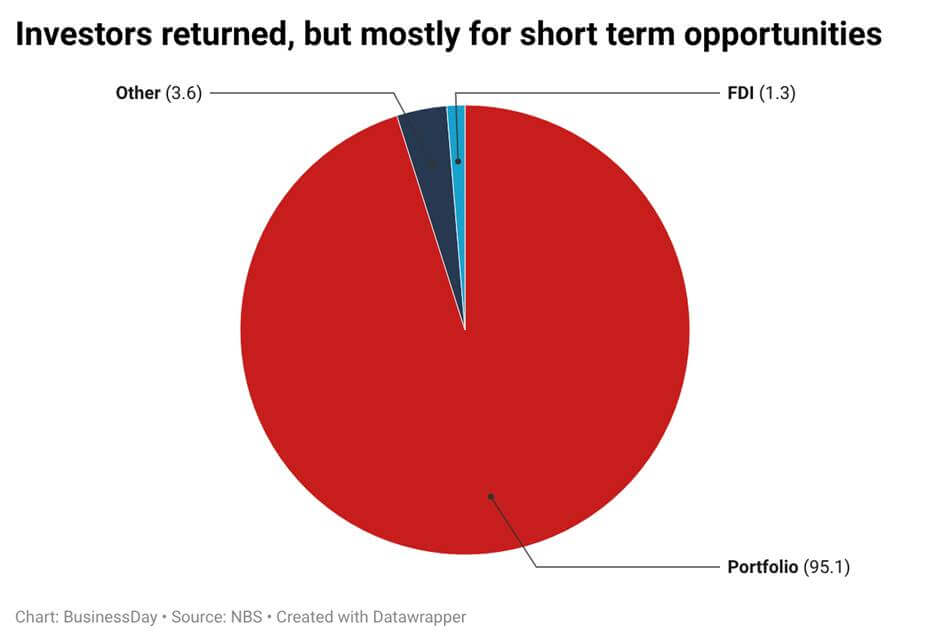

The clearest beneficiary was the government itself, which converted a costly recurrent expenditure into fiscal headroom and stronger credibility. State governments gained financially through record allocations, although higher receipts have not consistently translated into visible improvements in services, a reminder that more revenue does not automatically produce better governance. Investors responded positively, but the response should be read with care. Capital importation reached $10.37 billion in the first quarter of 2026, the highest in years and an 84 percent annual increase, yet roughly 95 percent of it was portfolio investment and only about 1.3 percent was foreign direct investment. The inflows reflect confidence in yields and reform direction more than long-term commitment to productive capacity.

Households carried the burden. Real incomes lagged prices, transport and food costs rose, and small businesses and manufacturers absorbed higher energy and logistics costs that many passed on or could not survive. The group most often cited to justify the reform, the poor, has so far benefited least, because the compensating measures were delayed and thinly spread.

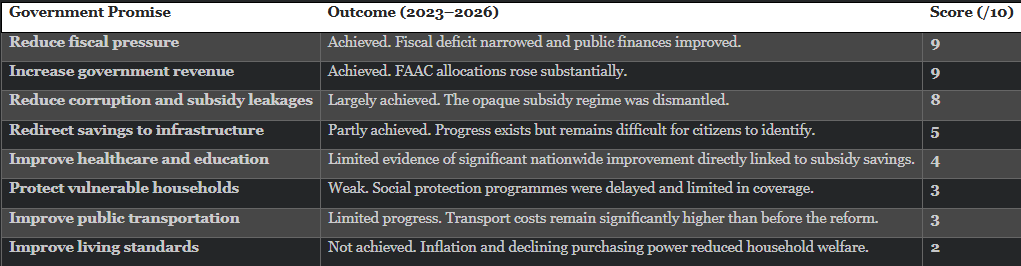

Policy scorecard

What would have strengthened the reform

The shortcomings lie less in the decision than in the management of the transition. Four measures would have improved it. Social protection should have been scaled before the price shock rather than after it. A transparent savings framework should have allowed citizens to track how much was saved, where it was allocated, and what it financed.

A defined portion of the savings should have been ring-fenced for visible projects in transport, primary healthcare, schools, and strategic roads, where tangible results sustain public support. And the reform should have been paired with a credible mass-transit response, given how heavily logistics weigh on household budgets.

The final policy verdict

Three years after its implementation, fuel subsidy removal remains one of the most consequential economic reforms in Nigeria’s recent history. The policy addressed a genuine fiscal problem and succeeded in eliminating a costly and distortionary expenditure that had become increasingly difficult to sustain. From a public finance perspective, the reform worked. Yet good policy is not judged solely by what it removes. It is also judged by what it creates.

The central weakness of the reform lies not in the decision itself but in the government’s ability to convert fiscal gains into visible improvements in citizens’ lives. Nigerians can clearly identify the costs of subsidy removal because those costs appear every day in transport fares, food prices, and household budgets. The benefits are harder to see.

That is why the debate persists. The question is no longer whether subsidy removal was necessary. Most economists agree that it was. The unresolved question is whether the government has done enough with the savings to justify the sacrifice.

Until citizens can point to better roads, stronger schools, improved healthcare, reliable public transportation, and more effective social protection funded by those savings, the fuel subsidy dividend will remain more visible on government balance sheets than in the daily lives of Nigerians.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp