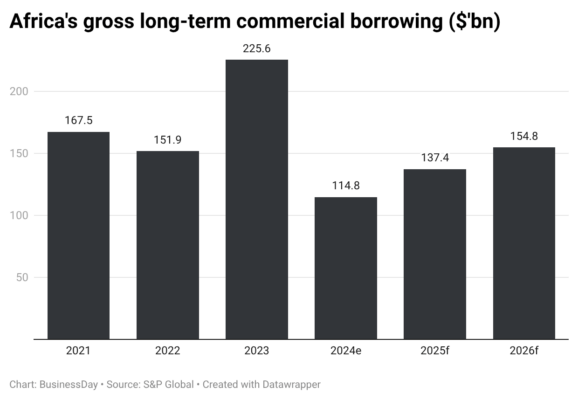

African sovereign borrowing is projected to rise to a three-year high of $155 billion in 2026, but escalating geopolitical tensions in the Middle East could cloud the outlook, according to a new report by S&P Global.

The rating agency estimates that commercial long-term borrowing by rated African sovereigns will reach $155 billion in 2026, up from $140 billion last year, driven roughly equally by maturing debt obligations and governments’ ongoing fiscal financing needs.

However, S&P warned that the ongoing conflict involving Iran, the United States and Israel poses risks to Africa’s borrowing plans through its potential impact on oil markets and global supply chains.

In the first two months of the year, Kenya, Côte d’Ivoire, Republic of Congo, Cameroon and Benin have already tapped international markets, signalling a decisive reopening of the Eurobond window after nearly two years of constrained access.

According to Bloomberg data, dollar-denominated sovereign bond sales across the region have reached $5.95 billion so far this year, the highest level for the period since 2013.

“The Middle East war and its effects on supply chains and hydrocarbon prices pose risks to Africa’s borrowing plans for 2026,” the report said. “If the conflict persists, particularly around key shipping routes such as the Strait of Hormuz, it could impair fiscal positions, inflation profiles and financing plans across Africa.”

The conflict, which began on February 28, has already pushed global crude prices above $100 per barrel, raising concerns about disruptions to energy supply routes. The crisis has affected tanker traffic through the Strait of Hormuz, a strategic waterway that carries roughly one-fifth of the world’s oil supply.

The impact is already being felt across several African economies. Nigeria, Egypt, Ethiopia and Zimbabwe have raised domestic fuel prices as higher global oil costs and supply disruptions filter into local markets.

For countries heavily dependent on imported refined fuel, rising oil prices are feeding into higher transport and production costs, potentially reigniting inflationary pressures that had begun to ease in recent months.

“Since most African countries rely heavily on refined fuel imports, rising prices could place additional strain on government finances, particularly if central banks respond by tightening monetary policy to manage inflation,” S&P said.

It added that fiscal pressures could intensify in countries such as Angola and Egypt, which maintain sizeable fuel subsidy programmes, potentially widening budget deficits.

Despite these risks, relatively favourable external financing conditions — currently at multi-year lows — could offer some relief, allowing governments to refinance upcoming foreign-currency maturities at lower costs.

Egypt, Morocco, South Africa to account for most regional issuance

According to S&P, Egypt, Morocco and South Africa will continue to account for the majority of sovereign issuance in the region, reflecting the larger size of their economies, more developed financial systems and stronger access to capital markets.

Total outstanding African sovereign commercial debt is expected to rise to just over $1.2 trillion by the end of 2026, equivalent to about 45 percent of GDP, including short-term debt.

Although borrowing needs vary across the continent, the median annual borrowing among the 27 rated African sovereign issuers is about $1.5 billion, significantly lower than global peers. This reflects the smaller size of many African economies and the continued reliance on concessional financing from bilateral and multilateral lenders.

At the same time, the continent governments face relatively high borrowing costs and a narrower investor base, often dominated by domestic banks and specialised international investors.

Borrowing dynamics also vary significantly across the region. South Africa is expected to see the largest decline in borrowing among African sovereigns, supported by a narrowing fiscal deficit and access to concessional funding, with its maturity profile remaining relatively stable at just under $6 billion.

Senegal is expected to rely more heavily on short-term domestic borrowing amid limited access to concessional financing and rising borrowing costs. S&P estimates the country could borrow about $10 billion in 2026, with around two-thirds coming from commercial markets and nearly half from domestic debt issuance.

Egypt is forecast to increase borrowing the most among African sovereigns next year, with total issuance expected to reach about $50 billion as the country finances a widening fiscal deficit. Africa’s second biggest economy traditionally relies on shorter-term domestic debt, resulting in a high rollover ratio — exceeding 30 percent of GDP annually.

Following the 2024 exchange rate liberalisation, high inflation pushed domestic borrowing costs sharply higher, leaving the country with one of the world’s highest interest-to-revenue ratios, estimated at about 70 percent in 2026.

One of Egypt’s key financing strengths, however, remains the depth of its financial sector. Egyptian banks hold large volumes of domestic sovereign debt, providing the government with a relatively stable local investor base compared with many other African economies.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp