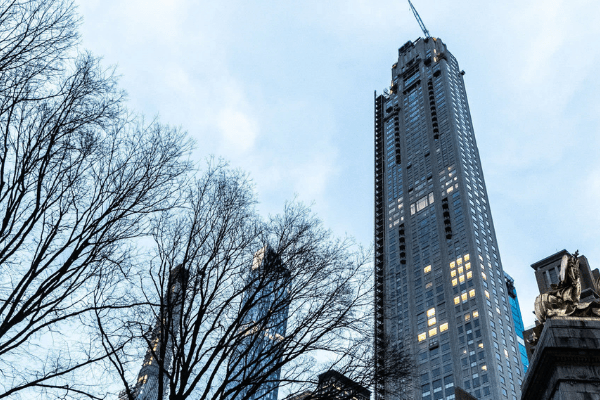

The shimmering Palace Residences apartment blocks will look out through palm trees, across calm creek waters lapping in from the Gulf towards what developers boast will be the world’s tallest structure. The futuristic, rocket-shaped Dubai Creek Tower will be a “notch” higher than the Burj Khalifa, the current holder of that title, just down the road.

Off-plan sales of the Palace Residences were launched in January, with one-bedroom flats on the market for Dh1m ($272,000), generating “significant demand”. The plan is for the 6 sq km Dubai Creek Harbour to eventually house 200,000 residents.

The project is a classic example of the “build it and they will come” development model that has served the rulers of Dubai well for the past four decades: carve out a space in the desert or on land reclaimed from the sea; build bigger and better luxury residences; offer top-class amenities; and sit back as wealthy expatriates snap them up.

Yet even as construction sites inch ever deeper into dusty desert districts, there are signs that this model may have run its course.

The skyline remains dotted with dozens of cranes, but amid a second downturn in a decade many stand idle. Construction on Dubai Creek Tower began more than two years ago, but only its foundations have been laid and no completion date has been set. Property prices are down by at least 25 per cent since 2014; real estate developers are trimming their headcounts and delaying payments to suppliers; parents speak of falling numbers at their children’s schools. Growth in gross domestic product decelerated to 1.9 per cent last year, the emirate’s slowest rate of expansion since 2010.

“The entire business model needs a radical reset,” says one company executive, who believes distress among the city state’s corporates will deepen this year. “Costs are too high to sustain these levels of activity.”

Dubai’s rulers, who brook little criticism of the economic model that transformed the emirate into the region’s trade, finance and tourism hub, appear to agree. Sheikh Mohammed bin Rashid al-Maktoum, its dynamic leader, last year turned to consultants to pull Dubai out of its funk, convening a series of meetings with business bosses to discuss ways of boosting the economy, such as cutting fees and privatising state entities to revive moribund capital markets. Dubai’s executive council has hired the PwC consulting arm Strategy& to turn some of those ideas into policy.

“The brainstorming sessions were meant to [help] understand the challenges and come up with ideas for the private sector,” says one consultant. “The executive council knows there is now a pressure to implement.”

At a time when job cuts are hitting white-collar workers, a priority appears to be boosting population growth among wealthy foreigners by providing expatriates — who make up 92 per cent of the 3.2m population and yet have no right to stay in the emirate if they lose their jobs — with a greater sense of belonging to encourage long-term investment. While official statistics show healthy growth in the foreign population, the exit of better paid, senior expatriates has chiselled away at discretionary spending in the consumer-driven economy.

Attendees urged the government to grant longer-term residency programmes to give expatriate investors more security. Traditionally, there has been a high turnover of expatriates living in Dubai but in recent years many have begun staying longer. Now — to counter rising living costs — Dubai has frozen school fees and government service charges indefinitely.

Abdulla al-Saleh, the United Arab Emirates undersecretary for foreign trade and industry, said last week that long-term visas would “go a long way to reinforce business confidence”.

A new law to allow 100 per cent foreign ownership of companies outside existing business parks, which currently exempt the need for a local partner, is another measure designed to improve the commercial climate and cut costs. But Dubai officials warn that “it will take time” for these measures to kick in.

Some business people question how much the government is listening. “It’s like we are talking a different language,” says one person who attended. “We talk about long-term investment and growth, they can’t see beyond the security risks.”

Giving foreigners more rights in what was historically a conservative, local society is unpopular among the 250,000 Emiratis in Dubai. Many fear losing even more control, while the security apparatus remains concerned about the risks of importing the region’s geopolitical woes into a traditional safe haven.

“These changes are not enough,” says a senior banker based in the emirate. “We need a new story.”

It is not the first time Dubai has been urged to change or that its brash business model has been questioned. Founded on open trade, international connectivity and a go-getting attitude, the city-state was swept up in the global financial crisis a decade ago, and at one stage was at risk of becoming the first sovereign default of the crisis.

It weathered the storm, thanks largely to a $20bn bailout from its big brother Abu Dhabi, the UAE’s oil-rich capital and by far the wealthiest member of the seven-strong federation. The lifeline exposed both Dubai’s oversized dependence on credit — in 2009 it was saddled with $109bn of debt, equivalent to 130 per cent of GDP — and the opaque nature of a system where the lines between the government and state-related entities are poorly defined.

Some of Dubai’s flagship state-affiliated companies were forced to restructure. And the crisis prompted earnest talks on the need to wean the emirate off its reliance on the cyclical real estate sector, alongside discussion of better governance and improved transparency. The rulers implemented property and financial reforms, while a sympathetic financial sector worked with Dubai to restructure debts.

The regional turmoil, triggered by the 2011 Arab spring, offered Dubai an opportunity to leverage its reputation as one of the Middle East’s most liberal and open societies to become a haven for those fleeing civil wars or their local taxman. Although Dubai has negligible energy resources, its role as a petrodollar recycling hub means its fortunes have long swung in tandem with its larger oil-exporting neighbours. So rising oil prices after the Arab spring helped the city-state.

At the same time, winning the right to host the World Expo 2020 in 2013 fed the renewed construction frenzy. The master plan for the expo, which organisers say could attract 25m visitors, envisages a 1,082-acre site, including a gated 370-acre area and surrounding residential, hospitality and logistics zones.

But within 12 months the collapse in oil prices had sparked a debilitating downturn across the Gulf. Governments, including the UAE, slashed spending and introduced taxes. The private sector, already struggling under government fees, has been battered.

Shifting regional dynamics have not helped. Abu Dhabi’s foreign policy has forced Dubai, for the first time, to choose politics over business. The UAE’s decision to join Saudi Arabia’s embargo of gas-rich Qatar forced Qataris to liquidate assets in the federation. The country’s strict implementation of US sanctions on Iran has also hit transshipment trade at Dubai’s Jebel Ali port. And the UAE’s intervention in the war in Yemen is estimated to have cost billions of dollars and sullied the country’s image.

Businesses fear this combination of factors is creating a poisonous atmosphere that poses a greater danger than the financial crash of 2008. From clothing to cars, retailers complain that sales have slumped by up to 50 per cent since the slowdown began, while retail space is forecast to increase by more than a third over the next two years. Hoteliers are slashing room rates as tourism growth slows, hampered by the strong dollar-linked currency and a surfeit of new rooms. Meanwhile restaurants are shutting their doors as wealthy expatriates are replaced by less experienced ones, who are being paid less and are saving more because of job insecurity.

Long used by multinationals as a regional base, some companies are rethinking that strategy. PepsiCo has made redundancies at its Dubai headquarters and is moving about 30 per cent of roles into larger markets such as Egypt and Saudi Arabia.

“The international business has faced a hit, so it is relocating staff,” explains Sherif El Meligy, chief operating officer of the local PepsiCo bottler, referring to an excise tax on fizzy drinks that has seen sales fall by a third since late 2017. “You can save on schooling and housing. It is localising jobs.”

David Clifton, director of strategy and growth at US engineering firm Aecom, estimates that the UAE has shed 150,000 construction related jobs in recent years. The white-collar expatriate exodus is compounding the woes of the private sector, with employment growing at its slowest rate since 2010.

“A decade ago, the government was in trouble but most of the private sector got through relatively unhurt,” says a senior Dubai official. “Now, the private sector is hurting most.”

Dubai is credited with developing one of the region’s most diversified economies, founded on trade and transportation. It has branched out into tourism, manufacturing and, more recently, finance, but it is still heavily dependent on real estate, which accounts for a quarter to a third of GDP growth.

Dana Salbak, a research associate at JLL, a consultancy, says the fall in property prices is likely to continue this year, albeit at a slower rate of decline. It estimates that only half of the 60,000 housing units under construction will be handed over this year because of delays. And while Ms Salbak says demand created by Expo 2020 could stabilise the market, others fear that some developments will end up as white elephants.

Avin Gidwani, chief executive of BNC Network, a research consultancy, says the number of projects on hold has risen to more than 980 — 28 per cent of all those under construction. “The city has too many contractors for the volume of upcoming work and is witnessing a survival of the fittest competition [between companies],” he adds.

Bankers remain relatively sanguine about the risk of a sovereign default. Dubai, including state-related entities, has been paying down debt over the past few years but still owes $122.5bn, equivalent to about 110 per cent of GDP, according to the IMF. Yet Jason Tuvey of Capital Economics fears the risks of real estate overcapacity could damage revenues at state-owned firms, harming their ability to service $30bn in debts that mature over the next three years.

Dubai has proved its sceptics wrong before — aided in part by Abu Dhabi’s backing — and it remains unrivalled as the region’s trade, tourism and finance hub, one which is pivoting to Asia’s higher-growth markets. But executives say the government must redouble its efforts to improve sentiment by cutting small business costs and reviving the emirate’s allure for big corporations.

The immediate challenge will be reversing the fall in property prices, given Sheikh Mohammed’s determination to push ahead with the type of grandiose projects that have characterised Dubai.

Yet, for some it is too late. “I am going to China, this place is dead,” says a senior executive at a Dubai-based family group. “It’s OK if you want to retire here, but I have another decade ahead of me.”

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp