Across Nigeria, unregulated investment channels promise high returns, collect millions through personal accounts, then vanish, leaving victims with heavy losses. In this report, BusinessDay Investigations exposes how these platforms recruit investors, exploit gaps in verification and transaction monitoring, and disappear without a trace, leaving victims with mounting losses and little recourse. SODIQ OJUROUNGBE writes.

When Chukwu Okafor (not real name) received a Telegram message from a woman who introduced herself as Chioma Adebayo, nothing about the opening exchange sounded like fraud. The tone was welcoming and formal.

She claimed to operate a closed, VIP betting system powered by paid analytics, gaming algorithms, and insider knowledge of match outcomes.

Adebayo claimed she could convert a modest investment into millions of naira within hours. The returns were tempting and were backed with screenshots of past winnings and testimonials from ‘other clients’ inside a private Telegram channel.

Read also: Why informal land market is preferred destination for investors

For Okafor, though the invitation looked risky, he was assured a refund plus 30 per cent compensation if anything went wrong.

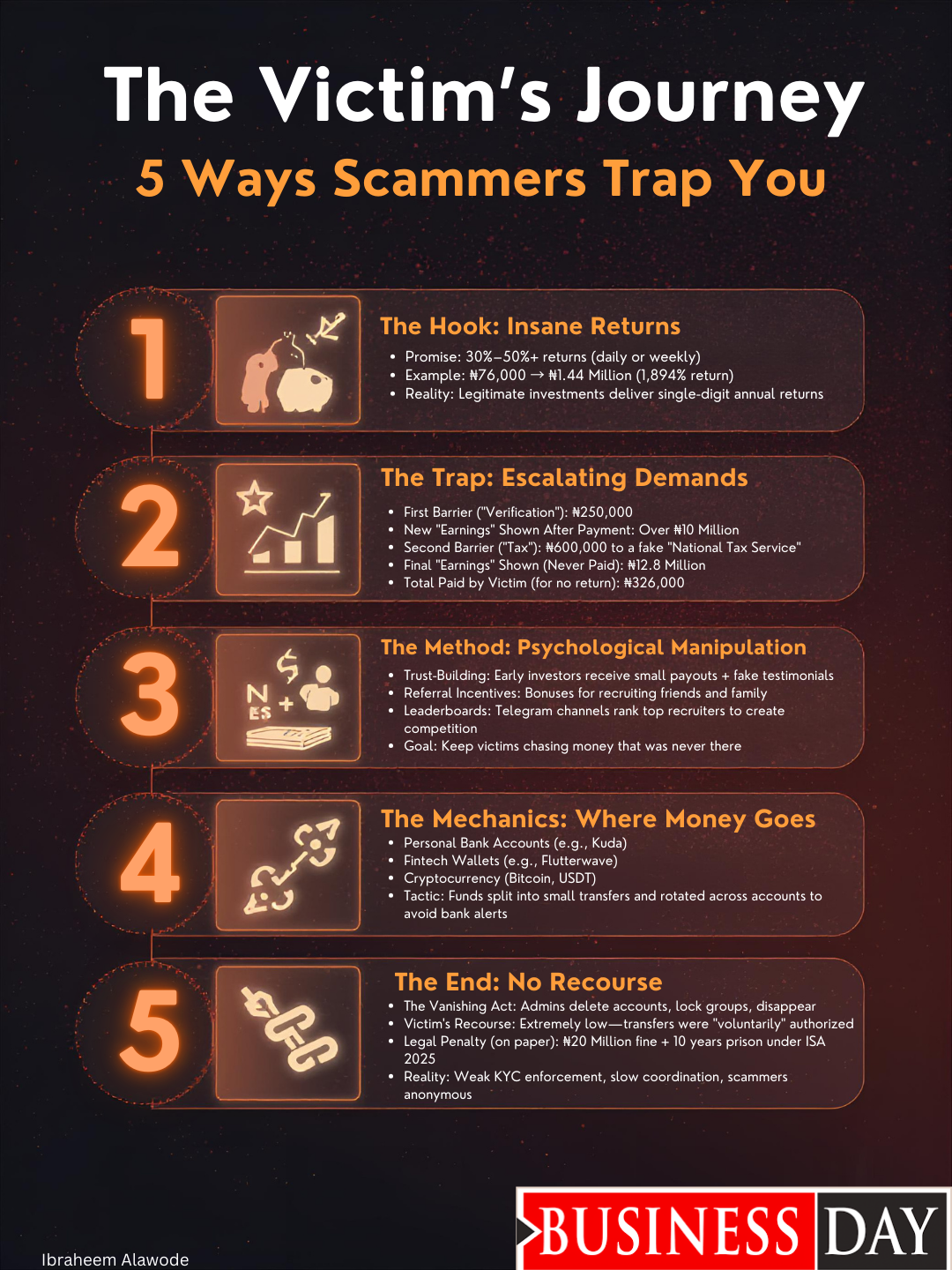

When Okafor agreed to proceed, he was presented with three investment tiers. The lowest option required N76,000 and promised a minimum return of N1.44 million within hours.

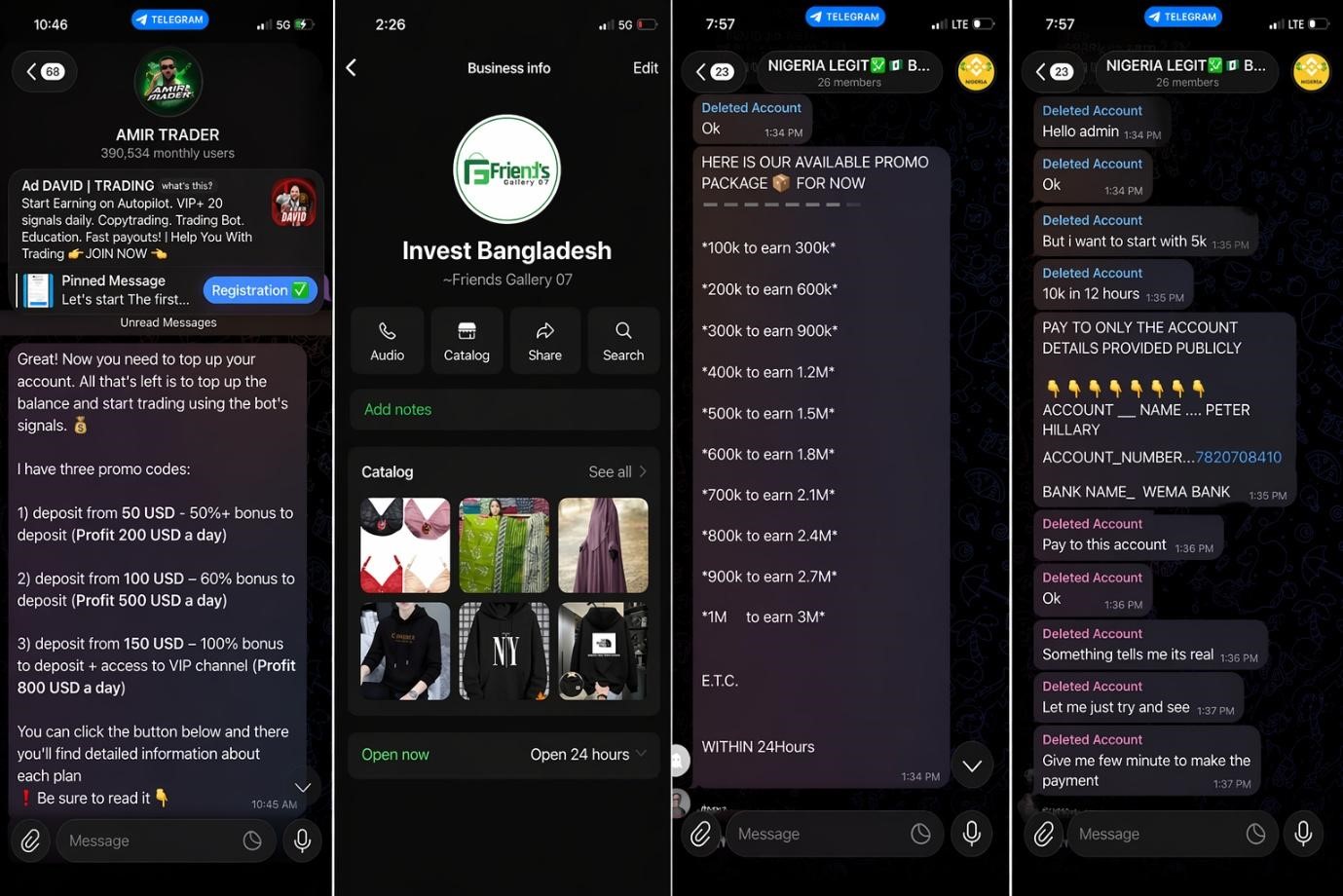

Okafor chose the lowest plan and paid N76,000 into a Moniepoint account number 9033991676, with the name, Kizito Chikamnele Olabisi, expecting N1.44 million in return.

Days after, he was told his earnings had risen to over N10 million. But to withdraw the money, he had to pay N250,000 naira for verification. Okafor made another payment, this time into a different account held with Guaranty Trust Bank, account number 0449784925, registered under the name Nwanna Emmanuel Kosisochukwu.

After the verification payment, the supposed winnings increased again, this time to N12.8 million. But instead of a payout, another barrier appeared.

Adebayo told him that an additional N600,000 had to be paid as a tax charge through a so-called “National Tax Service” before the funds could be legally released, however, such an agency does not exist in Nigeria.

“It was that time that I started growing suspicious of the investment scheme, but she kept insisting I had to pay the money before my returns would be processed,” Okafor said.

Each payment came with bigger promises, but no payout. The winnings kept rising, and so did the demands. When Okafor questioned the process and revealed he was a journalist, the tone changed, the response stopped, but the money never came.

The property shares that vanished

Unlike Okafor, Mariam Adepokiki did not wander into the scheme by accident. She was invited by a friend to join a Telegram group promoting what appeared to be a property shareholding investment. The offer was to invest in real estate projects and earn weekly returns in naira.

She was familiar with online investing and the capital market boom. Her husband used Risevest to buy dollar assets, including property. What stood out was the promise of fast weekly payouts instead of long-term growth.

Adepokiki searched the name Emaar and found Emaar Properties, a well-known real estate company in Dubai, United Arab Emirates (UAE). Seeing the name gave her confidence. The Telegram group repeatedly mentioned Emaar projects and shared messages about high profits. Large investments were promised returns of up to 50 percent per week. Members were urged to invest more to earn more.

After signing up, she was asked to pay into a private Kuda account to secure her slot. She questioned it, but was told it would make transactions faster.

Read also: Investors need transparent regulation and bankable projects Otto Canon

At first, she was able to withdraw money twice. That built her trust. Encouraged by group messages, she invested more, including the returns from the initial investment.

That was when the withdrawals stopped. Her dashboard still showed a balance, but when she clicked to withdraw, nothing happened. Messages sent in the group went unanswered. Eventually, the group’s coordinator’s Telegram account disappeared, and the group itself went silent.

What appeared to be a structured property investment scheme was, in reality, a hoax. It used a respected company’s name to gain confidence, delivered small early payouts to build trust, and collected money through personal accounts before vanishing without a trace.

“It looked legitimate because the name was real. That’s what convinced me. But the real company had nothing to do with it. By the time I realised that, the group was gone,” she told BusinessDay Investigations.

Like Adepokiki’s experience, BusinessDay found that many Telegram-based investment groups misappropriate corporate brand names, promise unusually high returns in short periods, collect payments through personal and fintech accounts, and disappear once enough capital has been extracted from unsuspecting victims.

Behind the disappearances

An investigation by this Newspaper into illegal investment operations on Telegram and Facebook showed that the experiences of Okafor and Adepokiki are not isolated incidents but part of a well-rehearsed operational framework used by fraudsters.

More than 10 victims who have lost millions of naira in such a scheme told our correspondent how they came across the investment, mostly through Telegram platforms.

Many told BusinessDay that by the time they realised what had happened, the administrators’ profiles had vanished, group chats were locked, and payment accounts were no longer active.

They lamented that attempts to recover funds through banks often yielded little success because transfers were authorised voluntarily, even if under deception.

Following complaints and patterns identified from these cases, BusinessDay Investigations conducted a review of online investment platforms targeting Nigerians.

Our correspondent used keyword searches such as ‘investment platform’ and ‘daily earnings’ and observed public groups and pages, documenting screenshots, links, and activity strictly from publicly available content.

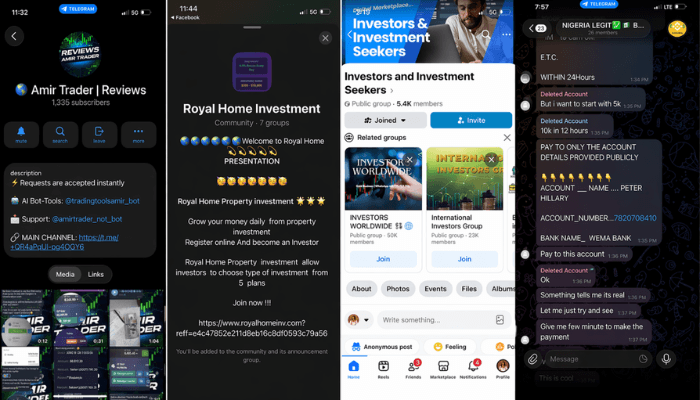

One of the platforms operated under the name Dubai Investment Fund, also referred to as Amir Trade. On the Telegram group, our correspondent observed that an administrator known as Amir frequently posted updates and recruitment messages.

Read also: UPDC REIT investors back SFS Capital as fund manager in unanimous resolution

New members were guided through pinned onboarding instructions, giving the platform a structured, almost corporate appearance.

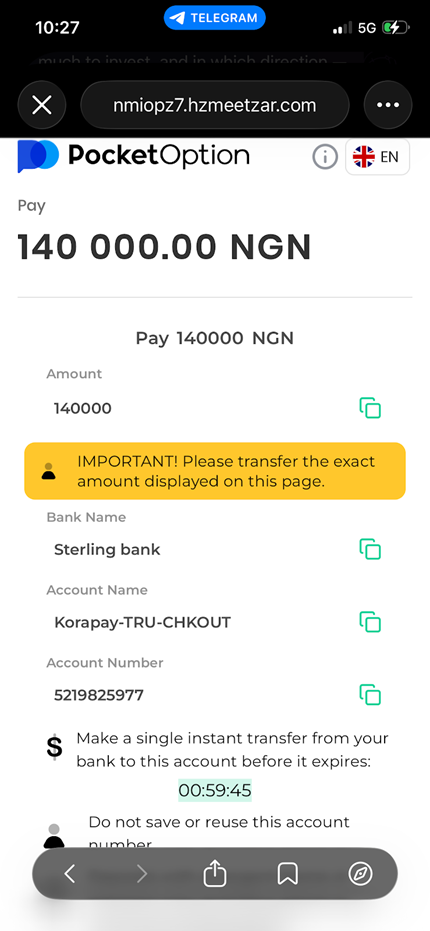

It was discovered that the scheme relied on referral links within Telegram channels to attract participants. Promises included high returns and rapid profits, while deposits were collected via direct bank transfers.

Some red flags found included repetitive testimonials using similar language and posts that emphasised urgency, pushing participants to make high minimum deposits to accumulate large sums quickly.

Another platform, Royal Home Investment, operated primarily through Facebook, redirecting users to Telegram and WhatsApp groups. It promised daily earnings and charged a ten percent administrative fee, while using cryptocurrency wallets for payments. Frequent promotional posts created urgency, often warning that only a limited number of ‘slots’ remained.

Also, a platform identified as Investors and Investment Seekers operated as a loose network of anonymous individuals who post opportunities on Facebook and direct participants into private WhatsApp chats.

During investigations, BusinessDay found that the group had no identifiable company structure, registration, or functional website, only direct bank transfers and shifting digital conversations.

Across all platforms, BusinessDay Investigations found that these platforms promised guaranteed or daily returns that are unrealistic in legitimate markets.

They relied heavily on Telegram and WhatsApp to operate, direct payments into personal bank accounts or cryptocurrency wallets instead of regulated corporate accounts, repeatedly used testimonials as social proof, and encouraged referrals to grow their reach without formal advertising.

It was observed that many of the platforms eventually became inactive without warning. Administrators stopped responding, groups were abandoned, and some Telegram channels restricted screenshot functions, making independent verification difficult.

BusinessDay Investigations show that the stories of Okafor and Adepokiki align with these operational patterns, with early credibility built through small initial successes or convincing demonstrations, escalating demands over time, and shifts in communication when scrutiny increased, all relying on platforms that allow anonymity, rapid transfers, and sudden disappearance.

Read also: Dangote Cement eyes London Listing, 10% stake sale to foreign investors

Marvellous Balogun, a victim of such a scam, explained, “This mechanism does more than expand the scam’s audience; it also deepens the psychological investment of those already involved. Once you bring others into the network, you feel a responsibility for the potential gains of your recruits, which encourages continued contributions and reinforces the cycle of trust and dependency.”

Investigations by this paper showed that some Telegram channels actively track referrals, displaying leaderboards that rank participants by the number of new members they bring in. These leaderboards create competition, giving the illusion of legitimacy, and ensuring a steady inflow of fresh capital into the scheme.

BusinessDay Investigations also discovered that these fraudsters rarely confine their operations to a single platform.

Our correspondent documented such schemes operating across direct messaging platforms such as Telegram and WhatsApp, as well as social media platforms, including Facebook and Instagram, creating a multi-channel ecosystem that keeps victims engaged while obscuring the movement of funds.

It was observed that Telegram often serves as the operational hub, providing onboarding instructions, daily updates, and recruitment messages that present the platform as a structured and formal entity, while using WhatsApp as a direct channel for communication with members.

Findings by BusinessDay showed that this mobility across platforms enhances anonymity. Accounts can be deleted on one platform while operations continue elsewhere under a different name.

It was discovered that administrators routinely rotate usernames, reuse bank or digital accounts across channels, and shift funds into cryptocurrency wallets to avoid detection.

It was gathered that the constant movement of activity and funds creates a digital footprint that is difficult to trace, leaving victims and regulators chasing disappearing targets.

Exploiting fintech and banking loopholes

Despite Know Your Customer regulations and anti-money laundering obligations, findings by BusinessDay Investigations showed that fraudsters exploit weak enforcement at the individual account level.

Apart from Opay, which mostly flags suspicious transactions during transfers, it was discovered that private bank accounts, e-wallets, and some fintech apps without this feature are often used to collect deposits.

Some of these fintechs require minimal identification to open personal accounts, which allows fraudulent operators to set up multiple accounts with relative ease.

Read also: Tinubu courts global investors in Paris as Nigeria records 11.2% dollar-term growth

Investigations showed that funds are often rotated across several accounts, sometimes split into smaller transactions to avoid triggering alerts.

It was gathered that when banks or fintech providers detect suspicious activity, operators quickly switch accounts, platforms, or even brands.

In October 2025, the Securities and Exchange Commission (SEC) said Nigerians lost about N316bn to Ponzi schemes and illegal fund managers.

This is not inclusive of the Ponzi scheme called Crypto Bridge Exchange, popularly known as CBEX, that carted away N1.3 trillion from unsuspecting Nigerians.

Digital loopholes in regulation

BusinessDay Investigations found that virtually all platforms documented were operating outside Nigeria’s legal framework, flouting regulatory safeguards aimed at protecting investors.

Under Nigeria’s Investments and Securities Act (ISA) 2025, promoting or operating unregistered investment schemes is explicitly criminalised.

Section 196(3) of the Act stipulates fines of not less than N20 million, prison terms of up to 10 years, or both for offenders. Anyone considering an investment is advised to verify the operator’s registration on the Securities and Exchange Commission (SEC) database before sending funds.

Despite these legal provisions, it was discovered that fraudsters exploit the low-cost, high-reach digital ecosystem to evade detection. Most platforms canvassing investors on Facebook, WhatsApp, and Telegram had no visible SEC registration, were absent from public registers, and made no credible disclosures about revenue sources or risk.

While the legal framework is robust on paper, findings by BusinessDay showed that enforcement is difficult when fraudulent operators use encrypted messaging apps like Telegram.

Regulatory oversight extends beyond the SEC. The Central Bank of Nigeria (CBN) plays a key role in protecting the financial system through anti-money laundering and counter-terrorism financing (AML/CFT) supervision.

The CBN guidelines require banks and fintechs to implement strict Know Your Customer (KYC) procedures, monitor suspicious transactions, and report activity that may indicate money laundering or illicit flows.

In recent years, CBN intensified expectations for real-time transaction monitoring and strengthened anti-financial crime systems, including draft standards for AI-based tools to detect complex patterns that might elude manual oversight.

Despite these guidelines and policies, BusinessDay Investigations found that many illegal platforms exploit gaps in these safeguards.

It was discovered that funds are collected through private bank accounts or unmonitored fintech wallets, bypassing institutional controls.

Experts and regulators stressed that while the Investments and Securities Act 2025 provides a strong legal framework, its effectiveness depends on robust enforcement and continuous oversight.

Daniel Okoye, a capital markets analyst and lecturer at the University of Lagos, told BusinessDay Investigations that laws alone cannot stop fraud if enforcement mechanisms lag behind the pace of digital innovation.

According to him, fraudsters operate across borders, on encrypted platforms, and exploit regulatory gaps. Investors remain vulnerable until regulators can monitor, track, and take swift action against these operators.

Okoye explained that digital investment scams exploit both speed and anonymity.

“Unlike traditional investments, online platforms allow administrators to appear credible in minutes, build trust through early payouts, and then vanish before authorities can respond. This creates a sense of legitimacy that can mislead even cautious investors,” he said.

Corroborating him, Ngozi Eze, a senior compliance officer with a leading fintech in Nigeria, reinforced this point, adding that many schemes rely on a classic Ponzi-like structure.

“These platforms often promise extremely high returns, sometimes daily or guaranteed profits. What is rarely explained is that these returns are funded by the deposits of new participants rather than actual investment activity. The system works only as long as new money keeps flowing in; once recruitment slows, the scheme collapses, leaving most investors with total losses,” she said.

Eze emphasised that these characteristics, guaranteed returns, early payouts, and continuous pressure to reinvest or recruit others, are red flags that regulators and investors alike should recognise.

How enforcement can catch up

Okoye noted that the solution begins with matching the speed of fraud with the speed of regulation.

According to him, enforcement agencies must move from reactive investigations to predictive monitoring.

“Digital scams evolve in real time. Regulators cannot wait for a collapse before acting. They need integrated surveillance systems that flag patterns across banks, fintechs, and digital platforms simultaneously,” he stated.

Okoye argued that deeper collaboration between the Securities and Exchange Commission, the Central Bank of Nigeria, the Nigerian Financial Intelligence Unit, and law enforcement agencies is essential.

SEC keeps mum

On February 20, 24, and 27, our correspondent attempted to reach SEC spokesperson Efe Ebelo by phone and WhatsApp, but he did not answer, and messages remained unanswered at the time of filing this report.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp