Imagine walking into your favourite clothing store and after shopping for some outfits, you are told the price is 0.00062 BTC rather than N10,000. Or you are taking a trip and you don’t need to take any physical cash and from the plane tickets, accommodation and food all paid with Bitcoin and everyone receives it without question.

Digitization is taking over the world, changing how we communicate, shop and work. Money is also changing.

Money has evolved from barter to coins, to paper money, to cheques and then plastic money which is the use of debit and credit cards. More recently, money has evolved to the use of digital currency such as cryptocurrency.

While fiat money still clearly dominates the way people move money, the crypto system is quickly gaining ground and there are speculations that it could just be the future currency.

Interest in crypto on the rise

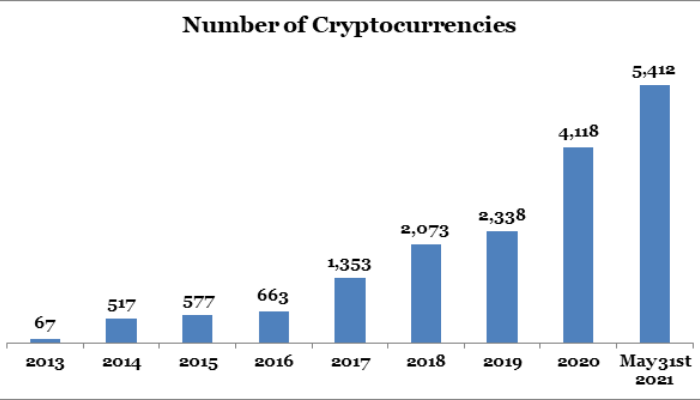

Before 2017, there was very little interest in cryptocurrency as well as limited media coverage. Now, cryptocurrencies have become increasingly popular over the past several years and nearly everyone is talking about it.

According to data from Coinmarketcap, the number of crypto currencies has risen from 67 to 4,118 between 2013 and 2020. As of May 31st 2021, the number has hit 5,412.

The number of users of various cryptocurrencies has grown by 66 million between 2018 and the last quarter of 2020.

A report by Citigroup also showed that the total market value of cryptocurrencies has more than tripled from its prior 2017 peak and search interest is steadily rising. Bitcoin has led the surge, accounting for about two-thirds of the total crypto market value.

Unlike 2017 when Bitcoin activity was mainly by retail investors, global institutional investors, and corporates are much more involved in the 2020-21 rally.

What is cryptocurrency and how it works

Cryptocurrency is a purely digital type of currency. It enables transactions between online users, and cryptocurrency “coins”, or units, can be exchanged for actual currency, or for goods and services.

Cryptocurrency is designed to allow the storage and transferral of value without anyone administrating the flow of currency; it is decentralised, as opposed to traditional currencies which are controlled or overseen by banks or governments.

For instance, the Naira is usually controlled by the Central Bank of Nigeria established by the Federal government. On the other hand, cryptocurrencies do not have this central control, it is controlled algorithmically.

They are exchanges via online trading platforms and apps. Examples of current popular cryptocurrencies are Bitcoin, the largest cryptocurrency, Dogecoin, Ethereum, Ripple, Litecoin and Cardano.

The term “blockchain” is central to understanding how crypto currency works. Blockchain technology forms the basis of the exchange of cryptocurrencies.

Just as the name implies, blockchain is a linked body of data made up with units called blocks, containing information about each and every transaction carried out including date, time, total value, buyer and also seller. Blockchain is a system of recording information in a way that makes it difficult or impossible to change, hack, or cheat the system.

For example, when A sends some bitcoin to B, the computers in the Bitcoin network (blockchain) will check to make sure that you haven’t already sent the data representing the cryptocurrency to another person earlier. When the blockchain has verified this, B is credited and A is debited. The computers in the network are preventing you from “double-spending.”

Why people are interested in cryptocurrency

While some see cryptocurrency as an investment, for others it is a way to navigate some of the challenges associated with paper money especially in Nigeria.

“If you get lucky to go abroad, find work and want to send money home to mom, you will have to pay ridiculous fees to do that, if it is an emergency, those funds might not get there on time but Bitcoin fixes that,” Bernard Parah, a twitter user said.

“Even if you try to save some money, food prices keep increasing and your currency loses 25 percent of its value against the US dollar in a year. This means you are working harder but getting poorer but Bitcoin fixes that,” he tweeted.

The Naira keeps losing value as the local unit was devalued three times last year by 24 percent to N381/$ from N360/$ at the beginning of the year. An impact of this is that imported goods become more expensive and it stimulates inflation.

Read Also: Crypto & money: Notes & arguments (1)

Inflation hit 18.12 percent in April, this is the first time it has slowed in 19 months since it has been rising steadily with food prices skyrocketing.

Investing in crypto is seen as a way to hedge funds against inflation rather than save in the bank and the value is eroded by the day.

“Driven by greed, youthful and irrational exuberance and loss of confidence in the system and currency. The estimated value of cryptocurrencies in Nigeria is $200mn,”said Bismarck Rewane, CEO Financial Derivatives in a recent presentation on cryptocurrency from a regulators perspective.

Interestingly, the first Cryptocurrency, Bitcoin was invested in 2009 by a programmer or possibly, a group of programmers under the pseudonym Satoshi Nakamoto shortly after the 2008 global financial crash.

Shortly after the creation of Bitcoin, Nakamoto left a code message “Chancellor on brink of second bailout for banks,” with many interpreting this to mean that Bitcoin was formulated in response to the reckless banking that caused the crash. Bitcoin ushered in a new age of blockchain technology and other decentralized digital currencies.

Can crypto be the money of the future?

Simply put, money in its most basic form is any method to transfer some type of value from one person to the next. It is any object that is generally accepted as payment for goods and services and repayment of debts.

The absence of money would mean people would have to operate a barter system where people trade goods and services for goods and services. The drawback of the barter system is that there must be a double coincidence of wants. This means whenever a yam farmer wants rice, the farmer would have to find a farmer who wants yam at that particular time and negotiate how many yams a bag of rice is worth.

It is easier for people to have their wants satisfied if all the members of a society agree to accept money, which is generally recognised and acceptable. However, how well something serves as money depends on how well it serves as a medium of exchange, a unit of account and a store of value.

How well cryptocurrencies can serve those functions relative to existing money likely will play a large part in determining cryptocurrencies’ future value.

First, can crypto serve as a medium of exchange? Currently, there has been an increase in businesses accepting bitcoin as well as other currencies as a medium of exchange. According to coinmap.org, there are currently just over 15,000 businesses that accept bitcoin or that offer bitcoin ATMs around the world. However, there are several others not accepting crypto yet.

Unlike the naira and other government-backed currencies, cryptocurrencies are not legal tenders, which mean sellers are not legally mandated to accept them in exchange for goods. For instance, a car dealer can refuse to accept bitcoin as a means of payment although it might be equivalent to the price of the car. Consumers and businesses also may be hesitant to place their trust in a decentralized computer network of pseudonymous participants that they may not completely understand.

Secondly, crypto must also be able to serve as a unit of account. A unit of account is something that can be used to value goods and services, record debts, and make calculations. The extreme volatility of cryptocurrencies is a problem when becoming a unit of account.

For instance, Elon Musk has an almost hypnotic control of the cryptocurrency market. Bitcoin’s upheaval came on the back of Elon Musk’s tweets. It soared when Musk said that Tesla will accept Bitcoin in payments for its cars. It nosedived after Musk said that the company will no longer accept Bitcoin as payments. Additionally, China has banned crypto transactions. Recently, in a single day Bitcoin dipped 30 percent to $31,000, wiping out $500 billion from its peak market value. Ethereum was down 40 percent and Dogecoin was down 45 per cent.

This volatility means that retailers would have to recalculate prices frequently and this can be costly and confusing. The uncertain market value of digital currencies would make it very difficult to use as a valid reference point for setting consumer prices.

Thirdly, for an asset, commodity or currency to be considered as a reliable store of value, it should have its value either increase or stay stable over a long time so that the owner can sell the asset for a similar or higher value than the price at which it was initially bought. Currencies are usually considered to be a good store of value given their higher liquidity levels.

For instance, gold can store value because it is scarce and has the ability to retain its value for a long period of time without losing its value. The unpredictability of the price of cryptocurrencies makes it difficult to refer to them as a store of value.

It has also been argued that features such as scarcity, divisibility, decentralised security network makes it a good store of value.

Some benefits of cryptocurrency over existing currency

Crypto has some benefits that have increased its use and acceptability over the years. First, in the traditional banking system, there is a transaction fee to be paid on every transaction carried out. If a lot of transactions are done every month, the fee would be whopping. Crypto makes it possible to carry out the same transactions with little or charge on the transaction fee.

Another advantage of crypto is the privacy it provides for the users. All data transmitted is literally hidden from unauthorized persons. Furthermore, transactions carried out using cryptocurrency can’t be changed or forged, and it’s transmitted in extremely high-security networks. However, financial records can still be traced for proof.

There is also a possibility of making high profit because the cost of cryptocurrencies changes constantly and often the difference is hundreds of percent over months or even weeks.

There is also the advantage of flexibility of use compared to stocks, bonds, and mutual funds. As more shops and restaurants begin accepting payments in cryptocurrency, it makes it easy for users to convert their assets into goods and services with a single click.

However, one major risk associated with cryptocurrencies is that they are currently unregulated by both governments and central banks. It’s hard for the government to track down any user by their wallet address or keep tabs on their data. Bitcoin has been used as a mode of exchanging money in a lot of illegal deals in the past, such as buying drugs on the dark web. There is also the possibility of human error or hacking.

Central banks in the arena

The declining use of cash spurred by the pandemic has necessitated contactless payment and this has made digital currency a point of focus in recent times. Central banks are also concerned with the loss of control over their own money supply and are engaged in studying digitally issued money which is also known as Central Bank Digital Currencies (CBDCs).

Central Bank Digital Currencies (CDBCs) are issued by governments or central banks as a digital form of fiat money and is controlled centrally.

A 2020 survey conducted by the Bank for International Settlements found that ’86 percent of the world’s central banks had already started to conceptualise and research the potential for CBDCs’. Of all the countries surveyed, 60 percent have begun research work while 14 percent are already in the pilot phase.

While some countries are still in the research stage, countries like China have developed its Digital Currency Electronic Payment (DCEP) CBDC in 2014 and tested a pilot in 2020. The digital yuan is now ready for use in regular transactions.

In Nigeria, a few months after the central bank ordered banks to stop serving the crypto industry, it also announced that it has plans to float a digital currency.

CBDCs would allow central banks to challenge cryptocurrencies like bitcoin and digital coins. Unlike cryptocurrencies, like Bitcoin, that operate via blockchain networks in a decentralized way, a CBDC is controlled by the central bank.

CBDCs would offer some benefits as it enables faster and easier transactions via mobile application, reduced cost of financial services such printing notes and it also allows for monitoring through the central bank ensuring high security.

Another key advantage of a CBDC is that it could be deemed a legal tender. This implies that everyone is mandated to accept it for any legal purpose.

However, the advantage of privacy that cryptocurrency offers would be absent as central banks would have increased control over money supply and would also know how people spend their money.

CBDC would also depend largely on internet availability. In a country like Nigeria with electricity outages it would be hard to have a successful CBDC system. This is because the transactions would require good internet connection and speed.

Also, digital currencies require work on the part of the user to learn how to perform fundamental tasks, such as opening a digital wallet and how to store the assets securely. The processes may have to get simpler to be widely adopted.

The future money

It is obvious that CBDCs offer some advantages that can rival crypto as a means of payment for goods and services.

“I believe if you are a central banker today and you love Bitcoin, you are crazy. It is a bit like the taxi driver being excited to see Uber come into their market,” Henri Arslanian, PwC Global Crypto Leader said in a recent interview with Citigroup.

“While there is a potential debate on privacy in payments, reality is that CBDCs give us a fighting chance against money laundering and illicit activities,” Arslanian said.

Naveed Sultan is a Managing Director and Chairman of Citi’s Institutional Clients Group (ICG) also pointed out that at the moment, classic Bitcoin is firmly in the realm of alternative investment. If people believe the price will go up, it is unlikely they will use the instrument as a method of payment.

However, Sultan said CBDCs could be a category killer.

“We should be extremely wary of silver bullets as they often have unintended consequences. Why is it that digital payments have taken over from physical? It is because there are thriving private markets in digital payments. There has been huge innovation and investment. CBDC could be a ‘category killer’ in digital payments and drive out private investment and development.

Having said that, a well-formed CBDC might play a role in the future of payments, but it will need to find its ‘goldilocks zone’… too big and it will drive out the private sector. Too small and it will be immaterial from a policy perspective,” Sultan said.

Although it is unlikely that cash will cease to exist as the safest form of money any time soon. People would be less willing to use crypto as a form of payment if they perceive the price would go up, which means it is seen as an alternative investment. As central banks create their own digital currencies, attention must also be drawn to convenience, accessibility.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp