For decades, small and medium enterprises (SMEs) in Nigeria operated outside the formal financial system despite their central role in economic activity. These businesses, which account for most employment and commercial transactions, faced barriers that limited access to banking services, credit, and digital tools.

This structural gap placed SMEs in a position where they were economically relevant but financially excluded. Without business accounts, payment infrastructure, or credit access, many operated in cash-based systems that restricted growth and participation in formal markets.

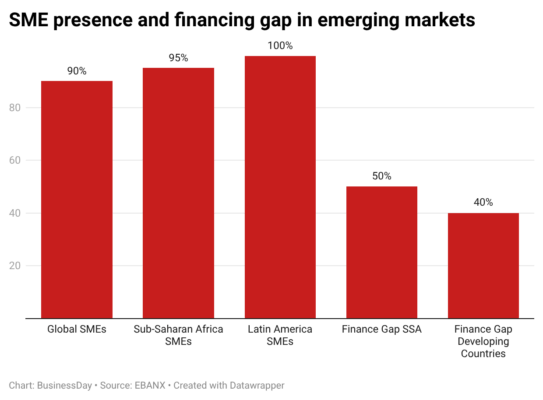

Across Sub-Saharan Africa, SMEs account for about 95 percent of businesses, compared to a global average of 90 percent, according to the World Bank.

Read also: How financial inclusion is becoming a core revenue strategy for African finance institutions

These account for about 60 percent of employment across many developing economies. In Brazil, the number of formal microentrepreneurs rose by 19 percent in 2025 to nearly 17 million, while Colombia has about 2.4 million registered small businesses.

Despite this scale, 40 percent of SMEs in developing countries face constraints in accessing finance, rising to 50 percent in Sub-Saharan Africa.

In Nigeria, the structure mirrors this trend. SMEs account for a large share of employment and output, yet access to finance remains limited. This financing gap extends beyond credit and into the ability of businesses to participate in digital commerce.

Financial exclusion and its impact on commerce

The Access to Finance (A2F 2023) survey by EFinA disclosed that 26 percent of Nigerian adults (roughly 1 in 4) are financially excluded, meaning they have no access to formal or informal financial services. While this represents an improvement from 32 percent in 2020,

The absence of financial access has had direct implications for B2B commerce. Without digital financial infrastructure, SMEs are unable to carry out basic business functions such as paying suppliers online, accessing digital services, or managing inventory through formal channels.

The Beyond Borders 2026 report by EBANX states that “Without financial inclusion, there can be no digital B2B commerce,” highlighting the link between financial access and participation in the digital economy.

This limitation has historically confined many Nigerian SMEs to informal markets, where transactions are fragmented, and growth opportunities remain limited.

Fintechs as entry points into formal finance

The emergence of fintech platforms has altered access to financial services for SMEs. In Nigeria, companies such as OPay, Moniepoint, and FairMoney have built systems that enable businesses to open accounts, receive payments, and access credit through mobile applications.

These platforms remove traditional barriers such as documentation requirements and branch visits, replacing them with digital onboarding and transaction-based services.

The report notes that digital wallets and neobanks are extending financial services to underserved businesses by leveraging existing consumer adoption. “Once you have adoption within the base for P2P, you can enable it for B2B. This has a huge impact on unlocking digital supply chains,” said Juliana Etcheverry, country growth director for South LatAm at EBANX.

This model is relevant to Nigeria, where fintech adoption has grown through consumer use cases before expanding into business services.

Payments remain the primary entry point for SME inclusion. Fintech platforms provide merchants with tools to accept transfers, manage balances, and process transactions without relying on traditional banking systems.

Agency banking and PoS networks have played a key role in Nigeria’s transition. These systems allow businesses to accept payments and generate transaction histories that can be used for financial services.

According to the EBANX report, these platforms “bridge the gap by offering instant payments and microloans directly on mobile,” reducing barriers to entry for SMEs.

Data from the Nigeria Inter-Bank Settlement System (NIBSS) shows that total electronic payment transactions, including NIP and PoS, reached N284.99 trillion in Q1 2025, representing a 17.7 percent increase compared to Q1 2024. However, only mobile money transactions hit N20.71 trillion in Q1 2025.

Brazil’s Pix shows infrastructure impact

According to the EBANK report, Brazil provides a case study of how payment infrastructure can accelerate SME inclusion. The launch of Pix by the Central Bank of Brazil in 2020 expanded instant payments across the economy.

Between December 2020 and December 2022, the number of business accounts doubled. By 2025, more than 22 million companies had conducted transactions using Pix, representing a 41 percent increase since early 2024. Companies are also more likely to use Pix through digital banks than traditional institutions.

The shift has altered the market structure. Corporate relationships with digital banks increased from fewer than 3 million to 9.2 million between 2020 and 2022, while traditional banks recorded a decline in corporate clients. About 40 percent of companies now operate exclusively with digital banks.

Among smaller firms, adoption is higher. More than 40 percent of sole entrepreneurs in Brazil use digital institutions as their primary banking providers, compared to 15 percent of medium-sized companies, according to Oliver Wyman.

Maximiliano Damian Rodrigues, general manager at Nubank Empresas, said mobile delivery of financial services has removed structural barriers. He noted that eliminating maintenance and transaction fees allows businesses to retain more capital for operations.

Data-driven credit reshapes access

As SMEs adopt digital payments, they generate transaction histories that can be used for credit assessment. This reduces reliance on collateral, documentation, and long-standing banking relationships.

According to Mastercard, 78 percent of SMEs in Latin America reported improved access to credit after adopting digital payments.

Tiffani Montez, principal analyst at EMARKETER, said fintech platforms are addressing gaps left by traditional systems and repositioning financial inclusion within digital finance.

Nequi reports that 68 percent of its credit disbursements go to users with limited or no prior credit history, while 3.8 million users manage business funds on the platform. The company said its approach combines credit, financial management, and advisory tools based on transaction data.

Access to digital accounts and credit is changing how SMEs participate in commerce. Businesses are moving from being payment recipients to active buyers within B2B ecosystems, using digital balances and financing to procure inventory, software, logistics, and advertising services.

OECD data shows rising SME participation in digital commerce across Latin America. In Brazil, online sales by micro and small enterprises grew by 1,200 percent between 2019 and 2024, reaching $2.4 billion.

Sector data from PCMI indicates that B2B demand is concentrated in software services, social media, and online education, with additional volume in retail and travel.

Alternative payments dominate B2B flows

Despite this growth, corporate credit card access remains limited, the EBANX report reveals. In Colombia, only 14.5 percent of companies have corporate cards, and credit limits are often low.

As a result, alternative payment methods dominate. In Brazil, Pix and Boleto remain widely used. EBANX data shows that Pix transaction values more than doubled in 2025, while Boleto has maintained annual growth of 34 percent since 2020.

Microenterprises account for 79 percent of companies using Pix on EBANX platforms. However, only 15 percent of B2B buyers use Pix exclusively, indicating reliance on multiple payment methods.

In Africa, patterns are similar. A GSMA report shows that 67 percent of Nigerian SMEs prefer bank transfers, while 61 percent of Kenyan SMEs rely on mobile money. In Kenya, M-PESA has recorded growth in its business segment.

In Egypt, where cash remains widely used, Fawry has expanded merchant and supply chain services, supporting the digitisation of B2B transactions and contributing to revenue growth.

Read also: How financial inclusion through insurance can help take people out of poverty

Inclusion expands participation in global trade

For Nigerian SMEs, the expansion of fintech infrastructure is creating a pathway to formalisation and participation in digital trade. As businesses adopt digital payments, build transaction histories, and access credit, their ability to operate within supply chains improves.

The integration of payments, credit, and financial management into mobile platforms is changing how businesses engage with markets. SMEs that previously operated outside formal systems are now able to transact, access services, and participate in cross-border commerce.

This shift reflects a broader restructuring of financial access. Beyond payments, it is redefining how businesses enter and operate within the digital economy, with implications for trade, credit access, and economic participation.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp