Financial inclusion has shifted from policy language to operating strategy across Africa’s financial system, as institutions redesign products, partnerships, and infrastructure plans to reach populations outside formal finance.

According to the 5th edition of the African Financial Industry Barometer 2025 report, institutions now link inclusion to growth targets, distribution expansion, and platform integration, with measurable adoption across sectors.

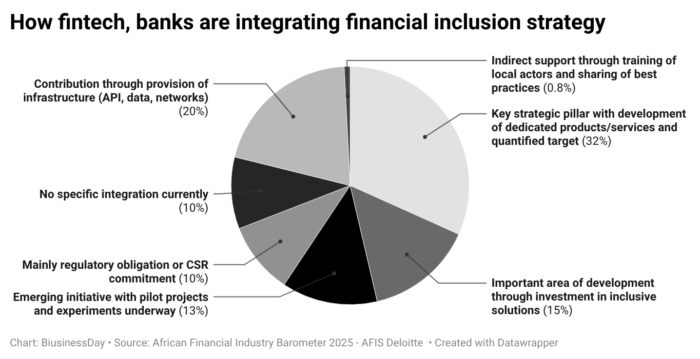

The report states, “Microfinance institutions report full alignment, and fintech firms report 67 percent. Banks record 20 percent classification as a core pillar and 35 percent as a focus, producing 55 percent active engagement. Insurance firms report 41 percent adoption.

It said that 24 percent of institutions report limited integration. 12 percent state no integration, and 12 percent restrict activity to compliance or social programs. The report notes the concentration of this position among capital market operators and regional firms, where half report no integration or compliance positioning, and 38 percent of regional firms report a similar status.

Read also: Africa’s startups raise $2.2bn in 2025 as growth outruns Europe, China and India

Geographic distribution shows 50 percent pillar adoption among pan-African groups, compared with 36 percent among international institutions and 37 percent among local institutions. The report links this pattern to scale, which determines reach, cost structure, and distribution capacity.

Sector findings show different incentives. Microfinance institutions and fintech firms built models serving populations outside banking. Insurance firms target segments with low coverage through products such as micro-health, agriculture cover, and simplified life policies distributed through digital channels.

Why banks report selective investment in access points, agency banking, and simplified products, citing acquisition cost and support requirements tied to transaction size. Capital market operators place inclusion outside their core activity because their services centre on securities and asset management. The report states that this limits participation in savings and investment.

Partnerships for financial inclusion: telecom operators, MFIs, and fintechs lead the way

The AFIS report disclosed that, regarding partnership data, telecom operators represent 25 percent of alliances with inclusion, microfinance institutions 26 percent, and fintech firms 22 percent.

It states, “The preferred partners for financial inclusion bring complementary capabilities,” linking telecom firms to infrastructure, microfinance institutions to local data, and fintech firms to technology systems.

Insurance firms report reliance on microfinance ties for rural distribution, with 82 percent using them. Pan-African groups report 72 percent use of these partnerships, compared with 33 percent among fintech firms. International groups report 73 percent preference for telecom partners and pan-African groups 78 percent, compared with 53 percent among local firms. The report links this difference to scale and negotiating power.

Fintech firms report 83 percent partnership rates with digital operators for joint product development, compared with 55 percent among banks and 35 percent among insurers. Banks and insurers focus partnerships on distribution rather than product design.

The report states, “This complementarity masks structural asymmetries in access to strategic partnerships,” noting that some institutions secure national agreements while others rely on intermediaries. Support services record low allocation.

Financial education represents 4 percent of partnerships through non-government groups, and digital identity represents 1 percent through public institutions. The report links this to limited usage after account opening.

Financial inclusion is when individuals and businesses have access to useful and affordable financial products and services that meet their needs—transactions, payments, savings, credit, and insurance—and are delivered responsibly and sustainably.

According to the 2022 MICS report, the importance of financial inclusion, which is a key enabler to reduce extreme poverty and boost shared prosperity, has been identified as an enabler for seven of the 17 Sustainable Development Goals (SDGs) 2030.

“Financial inclusion has been described as an enabler of seven of the SDGs and a vital tool for reducing poverty and boosting prosperity.”

Read also:From social media panic to AI reality: we are learning to slow down

“It helps to reduce the rate of poverty, generates employment, creates wealth, improves general welfare and standard of living, and drives overall economic growth,” it added.

Enhancing Financial Inclusion and Advancement (EFInA) disclosed that Nigeria’s financial inclusion rate grew to 74 percent in 2023 from 64.1 percent in 2020. However, it said the country targets 80 percent financial inclusion by 2030.

Interoperability and digital infrastructure: the missing links to expanding financial inclusion

According to the Access to Finance (A2F 2023) survey by EFinA, the excluded adult population of 28.9 million recorded in 2023 fell from 38.1 million in 2020, meaning 9.2 million adults left the exclusion circle in two years to 2023.

Authors of the AFIS report disclosed that, despite Nigeria and African countries still reporting high exclusion rates, factors or sectors still have a role to play in the transformation that will have the greatest impact on financial inclusion in Africa by 2030.

It said institutions rank system connection as the leading transformation priority, cited by 28 percent. Fintech firms and capital market operators each record 50 percent support, and banks record 35 percent.

The report links this to the need for connections across payment and data systems, noting that infrastructure, with 23 percent citing connectivity, energy supply, and identity systems as requirements for reaching populations outside finance.

Local institutions record 32 percent and international groups 27 percent. Financial education through technology ranks third at 14 percent, including 18 percent among insurers and 38 percent among other institutions. Regulation records 12 percent, and economic model viability records 8 percent.

The report states, “The 2030 vision reveals two complementary approaches, consisting of connections among 1.1 billion mobile money accounts to generate network effects and expansion of infrastructure to reach rural populations.”

It said that fintech firms and capital market operators emphasise system connection, while microfinance institutions and insurers emphasise infrastructure expansion.

Institutions expect change driven by continental firms, technology operators, and cross-border initiatives.

The report stated that education will support account usage and that technologies such as satellite systems, digital currency, and artificial intelligence may influence access models before 2030.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp