When the Central Bank of Nigeria (CBN) was named Central Bank of the Year at the 2026 Central Banking Awards in London, the recognition reflected more than an institutional achievement. It represented international acknowledgement of a difficult and often controversial reform programme that has sought to restore macroeconomic stability, rebuild confidence in financial markets, strengthen the banking sector and bring inflation under control in Africa’s largest economy.

The award came at a time when central banks around the world continue to grapple with the lingering effects of global inflationary pressures, geopolitical uncertainties and financial market volatility. For Nigeria, the recognition is particularly significant because it follows a period marked by exchange rate instability, elevated inflation, weakening investor confidence and concerns over the resilience of the country’s financial system.

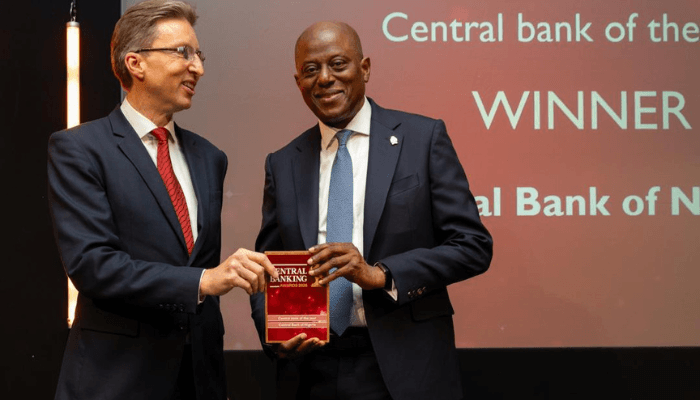

Receiving the award on June 10, 2026, Olayemi Cardoso, governor of the CBN, dedicated the honour to the institution rather than to individual leadership.

“I accept this award on behalf of the board, management and staff of the Central Bank of Nigeria,” Cardoso said during his acceptance speech.

“Above all, it belongs to the many dedicated professionals who serve our institution with integrity, expertise, and an unwavering commitment to the public good.”

The governor noted that the recognition reflected the collective efforts of the Bank’s workforce, whose contributions often occur away from public attention but remain essential to maintaining confidence in Nigeria’s economy.

His remarks came against the backdrop of a reform agenda that has increasingly attracted positive attention from international financial institutions, investors and market participants.

For much of the last few years, the central challenge confronting the CBN has been how to restore stability to an economy facing multiple pressures simultaneously. Inflation accelerated sharply, foreign exchange shortages disrupted economic activity, investor confidence weakened, and concerns mounted about the broader macroeconomic outlook.

The response required difficult policy decisions.

According to Cardoso, recent years have tested central banks globally, with Nigeria facing its own set of economic pressures and policy challenges.

He highlighted efforts undertaken by the CBN to address elevated inflation, implement major foreign exchange reforms and strengthen critical digital and financial infrastructure necessary for long-term economic development.

The significance of these efforts has increasingly been recognised beyond Nigeria’s borders.

The International Monetary Fund (IMF), in its latest Article IV Consultation Report on Nigeria, commended the authorities for reforms undertaken over the past three years that have strengthened macroeconomic stability and economic resilience.

According to the IMF Executive Directors, the reforms have helped improve policy credibility and support the country’s economic adjustment process.

The Fund specifically commended the authorities’ success in bringing down inflation, while acknowledging that external inflationary pressures remain a challenge.

Directors agreed that the Central Bank of Nigeria should continue to maintain a tight monetary policy stance while remaining data-dependent until disinflation becomes firmly entrenched and inflation expectations are fully anchored.

The endorsement represents a significant validation of the Bank’s approach to inflation management.

Few policy objectives have been more central to the CBN’s strategy than restoring price stability.

The Bank has relied heavily on monetary tightening to combat inflationary pressures, maintaining some of the highest interest rates in the country’s recent history.

At the conclusion of its 305th Monetary Policy Committee meeting in May, the CBN kept the Monetary Policy Rate unchanged at 26.5 percent.

Other key monetary parameters were also retained, including the asymmetric corridor around the MPR at +50/-450 basis points, the Cash Reserve Ratio at 45 percent for deposit money banks and 16 percent for merchant banks, and the liquidity ratio at 30 percent.

The decision signalled the Bank’s determination to sustain restrictive monetary conditions until inflation is firmly under control.

For market participants, the MPC’s decision was largely anticipated.

Razia Khan, managing director and chief economist for Africa and the Middle East Global Research at Standard Chartered Bank, said the decision came as little surprise.

“Few surprises in the actual decision, with the CBN opting to hold all parameters, including the MPR at 26.5 percent, the corridor at +50/-450 basis points, and the CRR unchanged,” she said.

According to Khan, the most important message from policymakers was their confidence that inflationary pressures would gradually ease.

“The big takeaway was that the CBN expects any near-term price pressures to be transient, with disinflation soon returning,” she said.

However, she also highlighted the challenges that remain.

“We are less convinced. We’re not sure inflation expectations are well-anchored. Fiscal policy in the run-up to the election could be a problem.”

Her observations illustrate the delicate balancing act facing the CBN.

While inflation has moderated and macroeconomic conditions have improved, policymakers remain conscious that gains achieved over the past three years could be vulnerable to both domestic and external shocks.

The IMF’s assessment similarly reflects a mixture of optimism and caution.

While commending progress in reducing inflation, the Fund encouraged authorities to continue strengthening monetary policy transmission and communication frameworks.

Directors also welcomed progress toward the adoption of an inflation-targeting framework, which many economists regard as a critical step toward enhancing policy credibility and anchoring expectations.

Inflation control, however, has been only one component of a broader reform agenda.

Another major area of focus has been the foreign exchange market.

For years, exchange rate distortions, foreign currency shortages and uncertainty over foreign exchange access weighed heavily on investor sentiment and economic activity.

The IMF welcomed the authorities’ commitment to a flexible exchange rate regime, recognising that foreign exchange interventions may play a complementary role under certain circumstances.

The Fund also encouraged policymakers to reduce reliance on portfolio flows that carry rollover risks while gradually eliminating remaining exchange restrictions, capital flow management measures and multiple currency practices as conditions permit.

The reforms have coincided with a strengthening of Nigeria’s external position.

According to analysts at the Financial Markets Dealers Association, average external reserves have continued to improve, supported by investor confidence and the gradual receipt of proceeds from earlier crude oil exports.

The improvement in reserves has become one of the most visible indicators of growing confidence in the economy.

Ayodele Akinwunmi, Chief Economist at United Capital, said the reserve accumulation would help reinforce exchange rate stability and support investor appetite for naira-denominated assets.

“This development is positive, as it will help sustain currency stability or drive naira appreciation while encouraging naira-denominated investments,” he said.

According to Akinwunmi, stronger crude oil prices, higher oil production levels and improved non-oil export performance have contributed significantly to reserve growth.

Ayokunle Olubunmi, head of Financial Institutions Ratings at Agusto & Co, also identified elevated oil prices as an important factor supporting reserves.

“Elevated remittance and the FPI have also been supportive,” he said.

The role of remittances has become increasingly important in strengthening Nigeria’s external position.

World Bank data showed that personal remittances to Nigeria reached $21.29 billion in 2024, maintaining the country’s position as one of the largest recipients of diaspora inflows in Sub-Saharan Africa.

Recognising the strategic importance of these inflows, the CBN has introduced several initiatives designed to formalise remittance channels and encourage greater participation from Nigerians living abroad.

These measures include the Non-Resident Nigerian Ordinary Account, the Non-Resident Nigerian Investment Account and remote Bank Verification Number enrollment platforms.

Analysts believe these initiatives could help deepen diaspora participation in the economy while supporting reserve growth and foreign exchange market stability.

The strengthening of reserves has also given the CBN greater flexibility to sustain ongoing foreign exchange reforms and provide a buffer against potential external shocks.

Beyond inflation management and foreign exchange reforms, the Bank’s reform programme has extended to the financial sector itself.

One of the achievements highlighted by Cardoso during his acceptance speech was the successful completion of the banking sector recapitalisation exercise.

The recapitalisation programme was designed to strengthen banks’ capacity to support economic growth while improving resilience against future shocks.

The IMF welcomed the fact that Nigeria’s financial system remains resilient, noting that recent recapitalisation efforts have helped reinforce stability.

Nevertheless, the Fund encouraged continued vigilance regarding rising non-performing loans and the sovereign-bank nexus.

Directors also called for accelerated implementation of Basel III standards, including the countercyclical capital buffer and the liquidity coverage ratio.

The IMF further stressed the importance of expanding regulatory oversight to include stablecoins and other crypto-asset activities as the financial landscape evolves.

Another significant milestone cited by Cardoso was Nigeria’s removal from the Financial Action Task Force (FATF) grey list.

The achievement represented an important boost to Nigeria’s international financial reputation and was widely viewed as evidence of improvements in financial integrity and regulatory compliance.

The IMF welcomed the development while noting that sustained implementation of reforms would be essential to preserving the gains achieved.

For the CBN, these accomplishments form part of a broader effort to restore confidence in economic management.

According to Cardoso, the Bank’s reform agenda has been guided by a clear objective: strengthening institutional resilience, rebuilding policy credibility and creating the foundation for sustainable growth.

“We receive this recognition with humility,” he said. “We see it not as a destination, but as encouragement to continue the important work ahead.”

Yet even as international institutions praise Nigeria’s progress, questions remain about the costs associated with the stabilisation programme and whether macroeconomic gains are translating into tangible improvements for businesses and households.

The Centre for the Promotion of Private Enterprise (CPPE) has welcomed the IMF’s broadly positive assessment of Nigeria’s reforms while arguing that policymakers must now place greater emphasis on growth and welfare outcomes.

According to the organisation, the reforms have delivered important benefits, including exchange rate stability, stronger foreign reserves, improved external balances, increased capital inflows and improved performance among listed companies.

“These gains are significant. After years of macroeconomic distortions, the economy is gradually moving from a regime of instability to one of greater predictability,” said Muda Yusuf, chief executive officer of CPPE.

At the same time, the group warned that excessive reliance on high interest rates could undermine long-term growth if stabilisation is not accompanied by policies that support investment, job creation and improved living standards.

The debate reflects the next major challenge confronting policymakers.

Winning the battle against inflation is only one stage of economic reform. Sustaining investor confidence, maintaining financial stability and translating macroeconomic gains into broader prosperity may prove equally important.

For now, however, the international recognition awarded to the Central Bank of Nigeria reflects a growing consensus that the institution has made meaningful progress in restoring confidence and strengthening the foundations of the economy.

The award acknowledges achievements in inflation management, foreign exchange reform, banking sector resilience, reserve accumulation, financial integrity and institutional credibility.

More importantly, it highlights how a central bank operating in one of Africa’s most complex economic environments earned global recognition while pursuing one of the most difficult policy objectives in modern economics: fighting inflation without losing sight of long-term stability and growth.

The challenge ahead is ensuring that the stability being celebrated today becomes the platform for stronger investment, higher productivity, job creation and improved living standards for millions of Nigerians. If that happens, the recognition received in London may ultimately be remembered not merely as an award, but as confirmation that Nigeria’s economic reforms had begun to deliver lasting results, said a banker.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp