Tax payments from companies in Nigeria rose in 2023 to the highest in at least nine years despite the tough business environment that has disputed many businesses.

The latest Company Income Tax (CIT) report by the National Bureau of Statistics shows that the tax revenue from both local and foreign firms in Africa’s biggest economy grew by 72.8 percent to N4.89 trillion last year from N2.83 trillion in 2022.

“Some companies, especially the financial services ones, made higher profits in 2023 compared to the previous years. There were also more Federal Inland Revenue Service (FIRS) audits that were conducted last year leading to more remittances,” Abiodun Kayode-Alli, tax senior manager at PwC, said.

He added that the expiration of certain incentives like the interest income on treasury bills expired in 2022, meaning that companies would pay more taxes in 2023.

CIT, which is also known as corporate tax, is a levy the government imposes on the income of a company.

The rate is hinged on zero percent for companies with gross turnover of N25 million or less, 20 percent for companies with gross turnover greater than N25 million and less than N100 million, and 30 percent for large companies above N100 million.

A breakdown of the NBS report revealed that tax payments from local firms rose to N2.51 trillion from N1.68 trillion and foreign firms’ payments also increased to N2.39 trillion from N1.15 trillion.

In terms of contribution, manufacturing activities contributed the most tax revenue to the government with N626.4 billion followed by information and communication (N466.6 billion) and financial and insurance activities (N428.8 billion).

“The tax collection efficiency has improved due to its technology called TaxPro-Max. It has been able to capture people that have been evading taxes for years,” Damilare Asimiyu, macroeconomic strategist and head of investment research at Afrinvest West Africa Limited, said.

The FIRS, in 2021, introduced TaxPro-Max, a tax administration solution for the ease of tax compliance. The technology enables seamless registration, filing, payment of taxes and automatic credit of withholding tax as well as other credits to the taxpayer’s accounts among other features.

“It is expected that CIT would increase because income revenue is a function of GDP. We had growth in GDP in Q3 and Q4. So, you would expect that revenue would increase. And you also have some sectors that have over the years been doing well in spite of the overall economic environment,” Adeola Adenikinju, president of the Nigerian Economic Society, said.

He said the various incentives that are put in place by FIRS may have led to more companies being in the tax net.

Apart from CIT, revenue from value-added tax rose to the highest since 2013, reaching N3.6 trillion, a 45 percent increase from 2022.

During the public presentation of the country’s 2024 Budget Proposals last November, Abubakar Bagudu, minister of budget and economic planning, revealed that the federal government achieved N8.65 trillion in revenue in the first nine months of this year from its pro-rata target of N8.28 trillion.

Out of the N8.65 trillion revenue, N1.42 trillion was generated from oil revenues, while non-oil revenues totalled N2.50 trillion.

CIT and VAT collections were N1.55 trillion and N318.95 billion. At the same time, other revenues amounted to N4.74 trillion, of which independent revenues from ministries, departments and agencies, as well as government-owned enterprises, were N1.28 trillion.

“The yield for non-oil tax revenue has continued to grow due to the efficiency from technology deployed by Federal Inland Revenue Service,” Yomi Olugbenro, partner and West Africa Tax Leader at Deloitte, said.

He added that the impact of exchange rate unification has also continued to have a positive impact on overall tax revenue of the government.

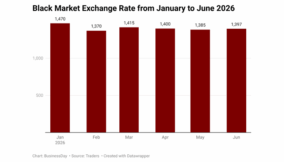

The liberalisation of the foreign exchange regime as part of measures to revive the economy led to a large devaluation of the naira.

The official exchange rate increased from N463.38/$ to N1602.8/$ as of Friday. At the parallel market, the naira depreciated to N1,605/$ from 762/$.

In January, the FIRS said it collected a record N12.4 trillion as tax revenue for the federation in 2023, surpassing its target of N10.7 trillion.

According to Zacch Adedeji, chairman of FIRS, the Federal Government has handed the agency a target of N19.4 trillion for 2024.

“What determines whatever we have comes from micro-economic indices because when the economy runs well, we are going to be taxing prosperity, not poverty,” he said.

“We will focus on the fruits and not the seeds. We need to ensure we have a viable economic environment that will lead to economic prosperity. And for us at FIRS, it is just to put the system in place to aid effective collection,” he added.

Taiwo Oyedele, president of the Presidential Tax Reform Committee last year, said Nigeria’s total tax incentive to companies is about N6 trillion annually.

He said the target is to achieve an 18 percent tax-to-GDP ratio over the next three years while ensuring reduced taxes payable by Nigerians.

Temitope Omosuyi, investment strategy manager at Afrinvest Limited, said naira depreciation is a double-edged sword.

“While this has created hardship for households and businesses through the alarming rising price level plus higher obligations in naira terms for individuals, businesses, and governments with external debt (or $ denominated debts), among others, revenue from CIT and VAT soared by nearly 60 percent in 2023,” he said.

“This looks commendable at a glance. However, when you remember that the price of the FX rate (naira to $) rose by 117.89 percent in 2023 at the official market, it becomes clearer that the purchasing power of this revenue is not very great at all. Hence, it is not time to celebrate yet,” Omosuyi added.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp