The Central Bank of Nigeria (CBN) took its latest step towards stabilising the naira after selling almost $90 million in the spot FX market on Tuesday, its first sale of dollars in the market since September 2023.

Sources familiar with the matter told BusinessDay that the CBN sold the dollars at a rate as low as N1490 per dollar, with more than half of the 34 banks that bidded securing between $2-5 million.

The sale is aimed at improving dollar liquidity in the market and breathing life into one of the world’s worst-performing currencies this year.

“Rather than fix rates, the CBN called banks to bid freely, and that’s good for the market,” a source told BusinessDay.

The CBN had frozen dollar sales at the spot market in order to deal with a foreign exchange demand backlog that was undermining investor confidence in the apex bank’s latest currency reforms.

The apex bank’s intervention in the spot market has been a long time coming. The CBN had said it would intervene in the market from “time to time” as far back as October 12, 2023.

“As market liquidity improves, these CBN interventions will gradually decrease,” the apex bank said in a circular dated October 12.

The latest intervention by the CBN however pales in comparison to the average of $25 million it sold daily in the market last year.

“CBN being back in the market is highly commendable, as its presence will boost trading liquidity,” another source familiar with the matter said.

Analysts, however, say the CBN needs to conduct the sale professionally and consistently in order to reap the full gains of its interventions.

“This is step one; the next step is to establish a pattern for the sales, and then the exchange rate trajectory will begin to change,” one of the sources said.

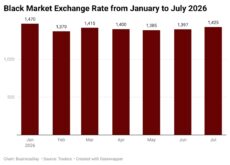

The naira gained on Tuesday to N1499/$, according to data by FMDQ Securities Exchange, which calculates the rates. That’s up from Monday’s record-low of N1,534.39 per dollar.

The CBN’s intervention in the market is the latest in a long list of moves aimed at boosting liquidity in the FX market and holding the rates in the official and black market from flying apart like they did after the naira was first allowed to trade freely against the dollar last June.

The Abuja-based bank has introduced better transparency around pricing in the official market, asked banks to offload excess dollars and removed the cap on transactions done by International Money Transfer Operators (IMTO)s to lure in diaspora dollars.

The CBN has however been urged not to lose sight of fully clearing the backlog if it wants to fully restore investor confidence in the market. Governor Olayemi Cardoso put the dollars owed by the CBN in forward contracts alone at $2.2 billion in an interview this month.

“Settling the CBN’s overdue dollar obligations will help rebuild confidence in the central bank and the naira,” one investor said.

“Sharing comprehensive information on Nigeria’s reserves position would facilitate a more complete assessment of the external situation,” the investor added.

Nigeria’s external reserves data has been viewed with suspicion since US-based JP Morgan’s shocking revelation that the CBN only holds about 10 percent of what it claims to have in net external reserves. JP Morgan is the Nigerian government’s foreign banker.

The International Monetary Fund (IMF) this week projected that Nigeria’s foreign reserves may see a record fall to $24 billion in 2024.

The CBN denied the JP Morgan report, but its struggle to clear the dollar backlog owed to investors and businesses raises questions about whether it does have the $33 billion in external reserves that it claims.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp