There is a quiet but consequential shift underway in Nigerian economic governance, and it has nothing to do with the presidency. For the better part of a decade, the country’s reform narrative has been scripted in Abuja — devaluation decisions, subsidy removals, monetary policy pivots, credit-rating negotiations. All eyes have pointed upward, toward the federal government, as the source of either salvation or sabotage. That gaze, understandable as it once was, is now looking at the wrong level of government.

The federal macro reform agenda has done much of the hard lifting it needed to do. The naira has been unified and allowed to find something closer to its real value. Fuel subsidies, which consumed more fiscal space than the entire capital budget in their final years, have been removed. The Central Bank has tightened aggressively and begun to ease with credibility. The IMF now projects real GDP growth of 4.4 percent in 2026 — the fastest pace in more than a decade — and foreign capital importation surged to $6.44 billion in the fourth quarter of 2025, a 26.6 percent year-on-year increase. These are not trivial gains. They represent the scaffolding of macro stability that investors and businesses need before they will commit serious capital.

But scaffolding is not a building. And the construction that now matters most — the roads, industrial parks, land registries, irrigation networks, skills institutions and investor-facing institutions that turn macro calm into micro-level prosperity — happens at the state level. Nigeria has 36 states and a federal capital territory. They vary enormously in population, geography, revenue base and ambition. What they share, right now, is an unusually large envelope of cash and an unusually wide window of opportunity. Whether they use it wisely will determine whether Nigeria’s recovery is broad or narrow, durable or decorative.

THE WINDFALL AND WHAT TO DO WITH IT

At the March 2026 Federation Account Allocation Committee meeting, the three tiers of government shared ₦1.894 trillion in monthly revenue — one of the largest single distributions on record. States are flush. Oil revenues have improved with global prices. Non-oil revenues, including VAT collections, have grown as the formal economy expands. The removal of the fuel subsidy, which previously consumed intergovernmental transfers before they even reached state coffers, has increased the real value of what states receive. For the first time in years, many governors face a question they are not accustomed to: what do we actually build?

“The most investable Nigerian states will not simply be the richest. They will be the ones that use revenue windfalls to reduce the cost of enterprise — relentlessly and measurably.”

The answer, in too many cases, has been: payroll. Personnel costs absorb an estimated 60 to 80 percent of recurrent expenditure in several Nigerian states, leaving little for capital spending and even less for the productive infrastructure that could eventually reduce dependence on federal transfers. States that run this model are not just fiscally fragile — they are economically self-defeating. A state that cannot maintain its roads, power its industrial estates or register a land title in under three months is not a state that can attract the private investment needed to grow its internally generated revenue (IGR). It is a state trapped in a low-equilibrium loop, waiting for oil prices to rescue it from its own inertia.

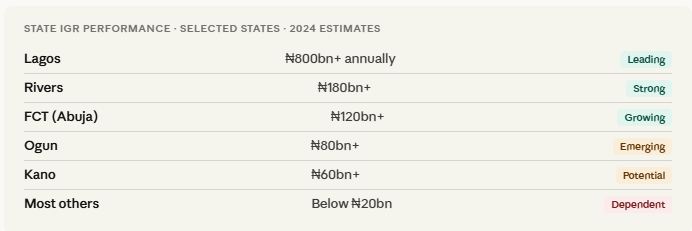

STATE IGR PERFORMANCE · SELECTED STATES · 2024 ESTIMATES

The contrast between states that have invested in their IGR base and those that have not is now stark enough to be instructive. Lagos generates more internally than the remaining 35 states combined. That is not purely a function of geography or historical advantage. It is also a function of deliberate, sustained investment in land administration, tax collection systems, transport infrastructure and business registration. Rivers State has rebuilt much of its IGR capacity following earlier political disruptions. Ogun — often overlooked — has quietly become one of Nigeria’s most active manufacturing corridors, leveraging proximity to Lagos port with industrial estate development, road investments and a relatively functional land titling system. These are not accidents.

THE GOVERNORS WHO ARE BUILDING

A useful way to assess subnational ambition is to ask not just how much a state spends, but what it builds and for whom. By that standard, a handful of states are doing things worth studying. Ogun’s Ogun-Guangzhou Free Trade Zone remains one of the most active special economic zones outside Lagos, with manufacturing clusters in ceramics, pharmaceuticals and light industry. Kaduna, despite security challenges that have rattled investor confidence in recent years, has made serious structural investments in ease of doing business — its State Investment Promotion Agency has attracted commitments in agro-processing and textiles that few northern states have matched. Anambra, with its historically entrepreneurial population and improving urban governance in Awka and Onitsha, is emerging as a logistics and commerce hub for the south-east.

What these states share is not simply money. They share a theory of how development happens: that the state’s job is to reduce friction for private capital, not to replace it. They invest in the connective tissue — roads, power, land, permits — that allows businesses to decide that the risk of setting up in Nigeria is manageable. They treat investors not as supplicants to be taxed at every checkpoint but as partners whose success generates the revenue base that makes government itself more solvent.

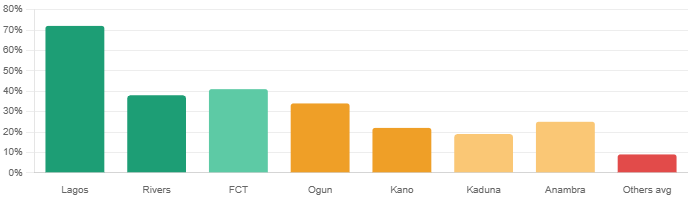

IGR as share of total revenue, selected states · Sources: FAAC, state budgets, NBS estimates.

THE GOVERNORS WHO ARE NOT

For every Ogun, there is a state where FAAC windfalls are essentially liquidity events for political patronage networks. Governors who treat monthly allocations as budgets to be disbursed rather than capital to be deployed are making a bet that oil prices will remain high enough, long enough, to sustain a government model that produces little for the citizens it is meant to serve. It is a bet that has failed repeatedly in Nigerian history, and there is no structural reason to expect different results this time.

The tell-tale signs are recognisable. States with high personnel-cost ratios and low capital budget execution rates. States where land registration takes months and requires unofficial payments at multiple stages. States where internally generated revenue has grown more slowly than inflation over the past five years, meaning the state is actually shrinking in real fiscal terms even as its nominal allocations rise.

States where the governor’s economic flagship project is a stadium or a government house renovation rather than a road, an irrigation scheme or a power substation. These choices are not neutral. They compound over years into structural underdevelopment that no subsequent policy can easily reverse.

WHAT INVESTORS SHOULD WATCH

For the private sector and for foreign investors making location decisions within Nigeria, the subnational story is becoming as important as the federal macro story. A business deciding where to site a factory, a logistics hub or an agro-processing plant is not just making a bet on Nigeria. It is making a bet on a specific governor, a specific land administration system, a specific security environment and a specific set of regulatory relationships. Getting that analysis right now matters enormously, because states that reduce business friction today will compound their advantages over the next decade.

“A business deciding where to site a factory in Nigeria is not just betting on the country. It is betting on a governor — and some governors deserve that bet far more than others.”

The metrics worth tracking are not complicated. IGR growth rate relative to inflation. Capital budget execution as a percentage of approved capital appropriations. Days to register a business and obtain a certificate of occupancy. Power supply hours per day in major commercial centres. Road connectivity between production zones and market or port access points. States that score well on these indicators — not perfectly, but meaningfully better than the average — are the ones where investment is most likely to generate returns rather than evaporate in operational friction.

There is also a financing opportunity for states that can demonstrate this kind of credibility. Nigeria’s domestic capital market is deep enough to support subnational bonds, and international development finance institutions — including the World Bank’s IFC, the African Development Bank and various bilateral development finance institutions — have appetite for subnational lending in economies where the macro environment is stabilising. A governor who can show a credible project pipeline, a functioning revenue collection system and a track record of budget execution is a governor who can access non-FAAC capital to accelerate development. Several Nigerian states have done this before. More should do it now, when their balance sheets are stronger than they have been in years.

THE TEST ABUJA CANNOT TAKE FOR THEM

There is a version of Nigeria’s future in which the federal macro reforms of the past two years become merely a historical curiosity — a moment of stabilisation that failed to translate into broad development because the subnational tier squandered the opportunity. That outcome is not inevitable, but it is not implausible either. The decisions being made right now in thirty-six state capitals — about what to build, what to reform, and who to serve — will matter as much over the next decade as anything the presidency or the Central Bank does.

Nigeria cannot be reformed from the top down alone. The country is too large, too diverse and too structurally complex for federal policy to reach every farm, every factory gate and every market stall on its own. Growth that is broad enough to reduce poverty, create employment and generate the tax base that makes governance sustainable has to be assembled piece by piece at the state and local level. That is not an argument against federal leadership. It is an argument that federal leadership, however capable, has natural limits — and that beyond those limits, it is governors who will determine whether Nigeria’s moment of macro stabilisation becomes a decade of genuine development or simply another chapter in a long story of promise deferred.

The resources are there. The window is open. The only question is whether the men and women who hold the keys to Nigeria’s thirty-six state houses understand what this moment demands of them — and have the ambition to deliver it.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp