Health insurance is one of the most powerful tools available to any government seeking to protect its citizens from the financial ruin of illness. The principle is simple: pool the risks of a large number of people, distribute the financial burden through prepayment, and ensure that people can access care without catastrophic costs at the point of need. For Nigeria, a country of over 220 million people, achieving universal health insurance coverage is not merely a policy aspiration. It is a survival imperative.

Yet decades after the first attempts to build a national health insurance framework, Nigeria remains one of the most underinsured nations in the world. Out-of-pocket payments account for over 70% of total health expenditure, the highest proportion in Africa.

The Insurance Journey in Nigeria

Nigeria’s health insurance story began in 1962, when the first attempt to establish a formal health insurance system was made, but the Nigerian Medical Association resisted it. It was not until June 2005 that the Federal Government of Nigeria formally launched the Formal Sector Social Health Insurance Programme under the National Health Insurance Scheme, with the ambitious target of covering at least 30% of Nigerians and achieving universal health coverage by December 2015.

That target was not met. By 2015, a comprehensive appraisal identified five critical failures: the non-mandatory nature of contributions, low enrolment of just 5%, poor adherence by over 50% of enrollees, the absence of an equity fund for vulnerable groups, and persistently high out-of-pocket spending. Nigeria’s out-of-pocket expenditure, already among the highest globally, increased from 60% in 2000 to 77% in 2017.

In response, the NHIS was decentralised in 2016, and State Social Health Insurance Agencies (SSHIA) were established in 35 of 36 states to drive sub-national enrolment. The Basic Health Care Provision Fund was introduced under the National Health Act of 2014 to provide an equity fund for vulnerable populations-children under five, pregnant women, the elderly, the physically and mentally challenged, and indigent citizens. The most significant turning point came on May 19, 2022, when President Buhari signed the National Health Insurance Authority Act into law. The NHIA Act made health insurance mandatory for all Nigerians and legal residents, enforced a Basic Minimum Package of Health Services across all schemes, strengthened private-sector participation, and embedded digital technology as core infrastructure for the insurance ecosystem. ecosystem.

Financing: Progress and contradictions

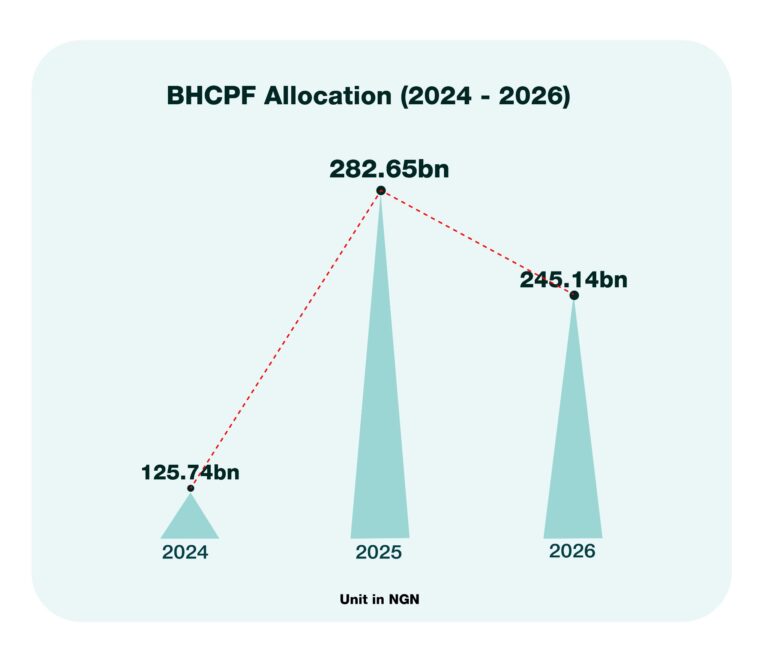

The Federal Government’s financial commitment to health insurance operates through several channels. The BHCPF, funded by a statutory 1% of the Consolidated Revenue Fund, saw its total budget rise from N125.74bn in 2024 to N282.65b in 2025: a significant increase that reflects growing political acknowledgement of the financing gap. But this also declined in 2026 to ₦245.14b. Of this, 45% is channeled to the NHIA Gateway to subsidise premiums for vulnerable citizens, amounting to ₦110.31b.

Also, the direct budget line for the NHIS in the 2026 federal budget, about ₦920.46m, tells a sobering story. This relatively modest allocation is likely intended for the agency’s operational costs (personnel, office overhead, ICT upgrades, and monitoring) rather than for funding actual medical care for citizens. It sits within a N2.51tn total health sector allocation that, despite being a nominal record high, represents only approximately 5.2% of the total ₦68.32tn 2026 federal budget.

Where coverage actually stands

The Q4 2025 Health Insurance Coverage data captures 21,737,130 total enrollees across all 37 states and the FCT, spanning 13 programmes including SSHIA, BHCPF, Federal Formal Sector, GIFSHIP, TISHIP, Global Fund, NHIA, and HMO Private Plans. Against a population exceeding 220 million, this represents approximately 10% national coverage, a marginal improvement from the 5% that characterised the NHIS era but still profoundly inadequate for a country committed to universal health coverage.

The coverage distribution is deeply unequal. Delta leads at 2,925,353 enrollees, followed by Lagos at 2,757,892. Kano and Kaduna are the only other states exceeding one million. At the other end, Taraba records just 213,935 enrollees, Benue 245,001, and Borno 266,762; states that carry high disease burdens and whose populations most urgently need financial protection from catastrophic health costs. The SSHIA programme is the largest contributor nationally at 9,744,758, followed by the Federal Formal Sector at 4,228,346: confirming that coverage remains heavily concentrated among government employees and formal sector workers. In contrast, the informal economy, which constitutes the majority of Nigeria’s working population, remains largely excluded.

The path forward

The challenges facing health insurance in Nigeria are structural, financial, and political simultaneously. Achieving universal health coverage requires the federal government to honour its Abuja Declaration commitment by consistently allocating 15% of the budget to health, not just nominally. The recent Senate passage of the BHCPF allocation from 1% to 2% is commendable. However, the amendment bill must be expedited through the lower chambers and backed by full and regular release of funds, with state counterpart funding enforced as a non-negotiable condition. In addition, the NHIA must develop credible mechanisms for enrolling informal-sector workers, including non-monetary premium-contribution options and community-based enrolment systems. Service quality at accredited facilities must improve materially, since enrollment is directly tied to the quality of care that enrolled citizens experience.

Finally, accountability mechanisms must be strengthened at every layer: from federal BHCPF releases to state agency performance to facility-level service delivery. Citizens, civil society, and the media must be empowered to track, question, and demand results. The NHIA Act of 2022 provides Nigeria with the strongest legal foundation it has ever had for achieving universal coverage. Whether it becomes a functioning reality or another unfulfilled commitment will depend on three things: the political will to sustain it, the institutional capacity to implement it and the accountability systems to ensure resources actually reach the people they were designed to protect.

Oyeleke Dare is the Assistant Program Officer of the Strengthening Health Systems Unit at BudgIT Foundation

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp