By Osaro Eghobamien and Tare Olorogun

Introduction

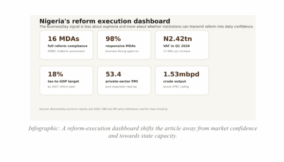

The new administration has undertaken a series of notable measures aimed at invigorating the nation’s economic landscape. A pivotal stride has been the cessation of the fuel subsidy, a financial endeavor previously estimated to consume a substantial proportion of the country’s revenue, alleviating a significant fiscal structure burden. In sync, a crucial reform enacted by the government entails the consolidation of the foreign exchange framework. While many contend that these endeavors signify a commendable progression, a cohort of critics assert that the true benefits of these governmental actions have yet to fully manifest.

A case in point is the unification of the foreign exchange window, which ostensibly aimed to enhance currency stability. Regrettably, the value of the naira has continued its downward trajectory, declining from a pre-unification rate of about 400 naira per dollar (official rate) to its present valuation of nearly 900 naira per dollar. This persistent depreciation raises queries about the efficacy of the unification strategy.

Additionally, the constant devaluation of the naira holds significant implications for the manufacturing sector. Importers are now facing the effects of the devalued currency on Letters of Credit. This instrument, once dependable, has lost its value, making it almost ineffective for importing purposes.

To illustrate, a previously issued Letter of Credit at a rate of 400 naira per dollar for a 2-million-dollar sum has surged to 800 naira per dollar, creating a considerable hurdle for manufacturers who rely on imported materials.

On the other hand, the removal of the fuel subsidy, while envisaged to yield positive outcomes, has inadvertently introduced hardships for the common citizenry.

The anticipated benefits have yet to be realized, and it is imperative that the government provide a transparent breakdown of the savings resulting from the subsidy removal and elucidate the allocation of surplus funds.

Furthermore, the administration led by Tinubu is proposing a significant reform involving the divestiture of its stake in government-owned entities. While divestment aligns with the principle that governance should not equate to commercial control, alternative avenues to optimize the value of these assets warrant exploration. In the realm of public finance, governments are increasingly turning to innovative methods to secure funds for vital projects, infrastructure, and economic advancement.

A technique gaining traction is securitization, a financial process that transforms revenue streams from government-held assets into tradable securities.

The journey of securitization begins by identifying valuable government assets that generate income (pertinent to note that dead assets that do not generate any income can also be securitized, this is nevertheless the subject of a distinct and separate paper). These assets can range from toll roads to public utilities.

To separate these assets from the government’s financials, a Special Purpose Vehicle (SPV) is established. This distinct legal entity safeguards the assets and forms the basis for the securitization process.

These selected assets are strategically grouped together into a diverse collection. This combination serves several purposes: it makes the securities more attractive to investors and reduces the risks associated with individual assets. The securities created from these asset collections fall into two categories: Asset-Backed Securities (ABS) and Collateralized Debt Obligations (CDOs). These categories reflect varying levels of risk and potential rewards. This is significant as creating instruments with different grades allows, for instance, pension funds to invest in securities that have A grades.

Pension funds are only permitted to invest in graded securities and grade A notes which are quite rare. This enables the application of pension funds that would otherwise be idle.

To give comfort to investors, techniques to enhance credit are integrated into the process of securitization. These techniques might involve setting up reserve funds to counter possible defaults, obtaining insurance or guarantees, and categorizing securities based on their levels of risk. A thorough examination is conducted to provide potential investors with a clear understanding of how these assets have performed historically and the associated risks.

The next step involves promoting these securities to institutional investors, including pension funds, asset managers, and hedge funds. Detailed documents are created to explain the advantages and potential risks tied to investing in securitization. Once investors decide to invest in these securities, they are formally issued and then traded in secondary markets.

As revenue generated by the underlying assets accumulates, it is channelled through the SPV. The government’s role in this process is multifaceted. Firstly, it entails supervising the securitization process to guarantee transparency and adherence to regulatory standards.

This responsibility is usually handled by an independent contractor and servicing agents as an added level of protection to increase investors’ confidence in the integrity of the transaction. Secondly, the government allocates the revenue to fund infrastructural undertakings, debt repayment, or strategic initiatives that foster economic development.

Upsides to securitizing government assets

The adoption of securitization for the Nigerian government proffers numerous benefits. Firstly, it provides governments with immediate access to funds that can be allocated to critical projects, such as infrastructure development or social initiatives.

Secondly, the diversification of investors reduces the government’s reliance on traditional sources of funding. Moreover, securitization spreads risk among investors, minimizing the impact of asset underperformance on the government’s finances. More importantly, the securitization structure resolves the issue of political risk by ringfencing the receivables in an SPV. It is a known fact that oftentimes, securitization projects are long term thus, they transcend the political cycle.

While the issue of project continuity and political cycles is not peculiar to Nigeria, however, the issue of project continuity remains relevant in Nigeria. This trend of abandoned projects seriously undermines investors’ confidence; investors need to be assured that legislation passed by any future administration will not affect their investment and securitization provides the necessary safeguard for the project from political intervention.

Regardless of its advantages, sustained vigilance over the SPV’s operations, asset performance, and fiscal health is indispensable. Regular reporting to investors and regulatory bodies cultivates transparency, nurturing investor confidence and upholding the credibility of the securitization endeavour. Looking forward, the dynamic landscape of public finance is poised to witness an expanded embrace of securitization as governments explore novel avenues to finance their ambitious projects.

The concept of securitization offers a promising avenue for governments to channel financial resources from existing assets, thereby propelling development, infrastructure, and economic progress. By navigating the intricate phases of asset selection, structuring, credit enhancement, and investor engagement, governments can adeptly harness the potential of securitization to create a mutually beneficial scenario for both public finance and private investment.

In summation, the government’s initiatives towards economic enhancement have elicited both commendation and criticism. While strides have been made in subsidy removal and foreign exchange unification, the tangible outcomes are yet to fully materialize.

Addressing the evolving challenges, particularly the currency devaluation’s repercussions on manufacturing and the optimal recharacterization of government assets, will necessitate a judicious approach that balances economic efficacy with social welfare. The benefits of securitization should be explored to the maximum extent to fuel development, infrastructure, and economic growth. As securitization continues to evolve, its potential to reshape the landscape of funding strategies for government initiatives remains both tantalizing and transformative.

By Osaro Eghobamien, SAN, Managing Partner,Perchstone & Graeys

Tare Olorogun, Partner, Perchstone & Graeys

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp