Lack of deal pipeline: The majority of project sponsors in Nigeria had limited capability to develop projects to a bankable level while the majority of investors would not invest without projects reaching financial close or close to.

Currency risks: The majority of infrastructure investors wanted dollar hedged returns and so looked to cover the costs of hedging from Naira based project cash flows. This reduced the number of projects that were fundable as the return expectations were accordingly raised significantly.

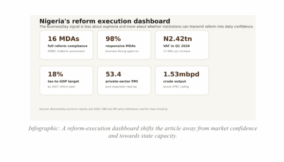

READ ALSO: Fixing market, infrastructure, regulation are ways to restore Nigeria’s power sector – experts

Pension fund demand: The Nigerian government had made a major push over the previous two years to allow pension funds to invest directly in infrastructure-related equity funds so long as such funds met strict guidelines. Nonetheless, up until the end of 2017, no equity funds had emerged in the market to meet this need.

From a capital aggregation point of view, some of the investors might be pension funds and institutional investors, and others might be insurance companies or high net worth individuals seeking asset diversification, Naira based investments, and Naira based yields. Compensation to the sponsor was comparable to a US private equity or venture capital setup, with a 2% management fee on drawn and committed funds and a 20% carry to the sponsor (after a set return to initial capital). The Infrafund sponsors expected to participate pari passu with about 5% of capital, aligning their interests with investors and keeping “skin in the game.”

READ ALSO: Gas pricing, inadequate infrastructure deters industrialization in Nigeria

From an investment point of view, Infrafund expected to keep a very tight focus on smaller ticket, shorter duration projects well under the radar of the Azura-Edo sized projects. To date, these had included schools and roads and they were expected to comprise power (including renewables), transportation (road and also seaports, airports, and rail) and basic infrastructure (water and sanitation). Africa Plus also expected to be more involved in project development with the sponsor, as opposed to the lighter on-the-ground engagement of a typical private equity fund due to the lack of skills in the Nigerian market. This Infrafund was led by a hands-on specialist in construction and project delivery, Anhad Narula (HBS MBA ’08) of DSC Group. DSC Group had been involved in some of the largest PPP and EPC projects in India and had project delivery experience in several African nations. The firm felt it had a defensible competitive advantage in project selection and project delivery thanks to its construction company origins.

A further focus for Infrafund was acting as a catalyst in shepherding some of the larger projects to financial close and then letting a larger fund or institution take the project to completion. To this end, Infrafund decided to partner with AFC for an independent review of investment opportunities and eventual co-investment, when projects developed to a larger scale and met AFCS investment criteria.

READ ALSO: Nigerian Pension Funds See Plunge in New Accounts as Jobs Dry Up

AFC was an Africa- focused multilateral financial institution covering project development, financial advisory, and principal investing.57 AFC acted both as a leading financier and adviser to its investor clients. It offered project finance, trade finance, structured debt, greenfield equity, and buy out capital as well as fixed income products. It complemented those product offerings with advisory capabilities in areas including project development, project management, capital raising, and restructurings. Since its inception in 2007, AFC had Strategic advantages of Infrafund were thought to be: to entry (in the revenue streams of projects selected). at opportunities with stable legal and operating environments and additional guarantees on revenue). life cycle of the investment (Infrafund would look for current cash yields from the asset rather than purely an asset value appreciation and sale). visibility (Infrafund would shortlist projects with construction periods of six to 18 months and use of proven technology to reduce the high risks associated with project development in the market).

Observers wondered if Infrafund had a higher-yielding risk-adjusted offer than an investment

Infrafund would take project inception risk and project delivery risk, which had greater upside potential but also substantial uncertainties based on cash flows from in-place stable assets). Observers also considered whether Infrafund, which was a first-time fund in a space in which pension fund advisors had limited experience, would be able to attract investors at a reasonable rate of return.

READ ALSO: Nigeria’s micro pension suffers setback on poor savings culture, COVID-19

Was the Azura-Edo large project format, the Infrafund setup, or the Infracredit enhancement offering the model that would unlock trillions of Naira in infrastructure investment? Which one would attract capital?

Fresh Equity, New Debt, or More Contingent Money?

To grow the Infracredit business at a rapid rate to accommodate huge infrastructure need and potential substantial interest from investors, Azubike would need to raise more capital. As Infracredit became more established, could they expect to raise additional capital from NSIA? Could they look to the Guarantco team to scale up with them – or might Guarantco determine that Infracredit was now successful and move on to another offer in the Infracredit business model attractive to new institutional investors who might add to core capital (equity), or was that avenue likely to be closed off? And if none of those avenues looked promising, should Infracredit borrow funds to have them to both invest in current assets and also as a backstop for guarantee problems? Many international banks and insurance companies indeed borrowed money to build the liabilities side of their balance sheets so they could then lend out money to build the asset side.

There was so much going on at the guarantee level that Azubike felt he should only pursue one capital structure path. Which one? The right choice could help Nigeria grow and thrive, and the wrong choice would lead to disappointment.

Concluded

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp