The tangled web of Chinese banks and the investment products they sell is growing more muddled as analysts attempt to gauge the impact of new rules unveiled by the country’s authorities.

The proposed new rules would require some banks to provision for losses against wealth management products (WMPs), which funnel money from retail investors into securities ranging from stocks to corporate bonds and real estate, in an effort to insulate the lenders from future losses.

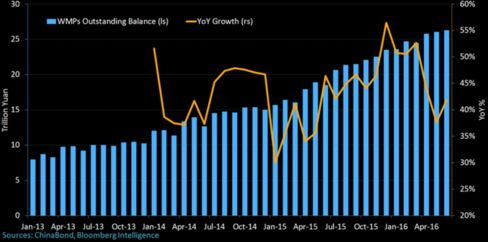

The 26.3 trillion yuan ($3.9 trillion) worth of WMPs outstanding have emerged as key cog in China’s so-called shadow banking system as investors often expect to be reimbursed for on any losses on the WMPs banks manage — an expectation that could weigh on the lenders if the products begin to sour.

But with analysts scrambling to digest the impact of the draft rules on banks, fresh concerns are emerging including: the degree to which banks have been using WMPs to repackage and invest in other such products, their use as a way for to gain exposure to riskier corporate securities, banks’ tendency to borrow money to boost returns on WMPs, and the potential for the new WMP rules to impact other assets.

1. WMP-squareds, anyone?

Banks may be using WMPs to repackage and invest in other WMPs in an attempt to avoid rules introduced in 2013 that similarly sought to shore up the financial system by limiting the amount of money lenders can invest in ‘non-standard’ securities to 35 percent of total assets. Such a move would have parallels with some of the more complex collateralized debt obligations (CDOs) that exacerbated subprime losses at U.S. banks in the run-up to the 2008 financial crisis.

“For a bank that is bumping into the 35 percent limit, investing in other WMPs — which then invest in the non-standard asset — could be a way to get around the cap,” said CreditSights Inc.’s Matthew Phan. “In effect it is another channel by which to route off-balance sheet lending. This led to some concerns about WMPs sold to other WMPs, or ‘WMP-squared,’ an allusion to the ‘CDO-squared’ structures that led to huge losses in the U.S. financial system.”

The proportion of WMPs bought by other banks jumped from 0.49 trillion at the end of 2014 to 4 trillion a the end of the first half of 2016, though the exact proportion of any such ‘WMP-squareds’ is unknown.

2. Boom go the corporate bonds

While the 2013 rule was similarly aimed at shoring up China’s financial system, it may not do much in the face of a debt boom that has seen the country’s companies sell trillions of yuan worth of corporate bonds as these securities count as ‘standard’ assets.

“Regulators introduced the restriction on ‘non-standard assets’ in March 2013 and have not changed it. However, trends in corporate bond issuance, especially in the second half of 2015, may have circumvented its effectiveness in terms of restricting flow of investor funds to low-quality companies,” said Phan.

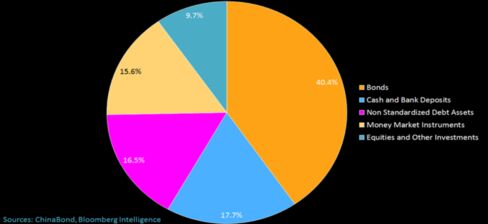

Analysis by Bloomberg Intelligence’s Tom Orlik and Fielding Chen found that funds raised through WMPs ultimately find their way into bonds (40 percent), cash or bank deposits (18 percent), loans (17 percent), the money market (16 percent) and equities and other investments (10 percent).

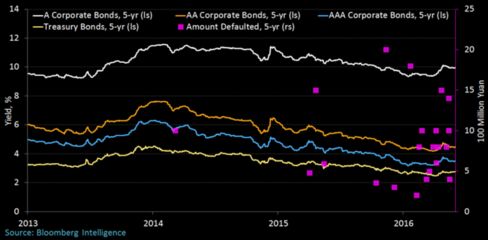

But with such investments offering increasingly meager returns — at the end of the first half of 2016, the yield on five-year corporate debt rated AA+ was just 3.8 percent — banks may be tempted to buy bonds sold by riskier but higher-yielding companies or borrow money to boost their returns.

3. Lots of leverage

Such borrowed money, or leverage, may be needed as banks seek to offset declining profitability.

“With a typical WMP offering returns around that level [3.8 percent], and the bank requiring a spread on top of that to cover costs and show a profit, that’s not enough,” Orlik and Chen wrote in a note. “In order to keep returns elevated, the shadow banks managing WMP investments appear to be turning to the interbank market as a source of leverage.”

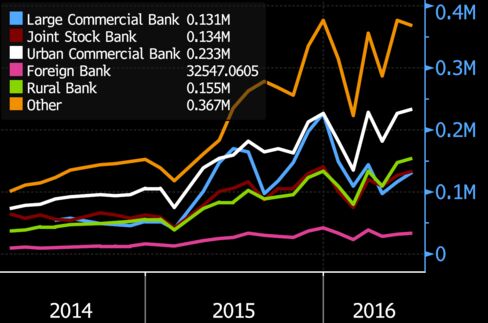

The application of leverage may be borne out by statistics in the Chinese interbank market, where lending rose to 59.8 trillion yuan in August this year, up from 13.7 trillion yuan in November 2013, when the data began, the analysts said. Orlik and Chen note that the biggest players in this market are small banks and ‘other’ financial institutions — or the firms originating and managing the WMP funds.

Bank lending to ‘other’ financial institutions has increased 44 percent from a year ago, which may be one reason why the Chinese authorities are pressing for new rules to buffer lenders from losses.

4. A bad cycle

Ironically, banks may need to buy riskier securities or use more leverage as they fight slumping profits and a shrinking pool of WMP fees induced by the draft rules. Even if they resist that temptation, reduced demand for their WMPs may end up clipping appetite for other assets such as bonds and stocks, causing a downward spiral in asset prices.

“The proposed new regulations on the bank-managed WMP market, which may come out within months if not weeks, may further dampen bank-managed WMP sales going forward, in our view,” Bank of America Merrill Lynch strategists led by David Cui wrote last week. “As the biggest funding source for the shadow banking sector, we believe that any significant slow-down in its sales may have important implications on asset prices across the board, especially bonds’ and stocks’, and possibly properties.'”

“Given the potential shocks to financial system should bank-managed WMP sales slow down sharply, we consider it a key risk that needs to be monitored closely,” they concluded.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp