Peter Obi, the presidential candidate of the Labour Party, says people in the government are responsible for the massive oil theft that has blocked Nigeria from benefiting from the boom in oil prices and deprived Africa’s largest economy of much-needed petrodollars.

“People in the government are the ones stealing oil. Nobody here can steal oil,” Obi said during the Lagos Chamber of Commerce and Industry (LCCI) private sector economic forum on Monday.

“There’s no way under my watch that we will not find a solution to oil theft,” Obi, who estimated that Nigeria has lost about $5 billion in the months of July and August alone to oil theft and other challenges affecting oil production, said.

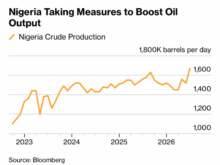

Nigeria’s oil production fell to a three-decade-low of below 1 million barrels daily in the month of August, according to OPEC data.

That has seen the country lose its position as Africa’s largest oil producer and is now behind Angola and Libya.

Read also: Nigeria’s oil rig count falls for first time in 2022

Government officials estimate that over 400,000 barrels of crude oil are lost to oil theft daily. The county’s chief of naval staff however disputes those figures, leaving Nigerians playing a guessing game of how much crude is actually lost to theft.

Between January and July, the NNPC said the country lost an average of 437,000 barrels of oil a day to criminal entities and individuals who illicitly tap pipelines onshore and offshore in the Niger Delta region.

The stolen oil was worth more than $10 billion at the average oil price in that period, according to the NNPC’s calculations, nearly three times what the federal government earned between January and April, when debt service costs surpassed revenues by 18 percent.

In the meantime, the low oil production and attendant loss of revenues has starved the country of dollars and caused the exchange rate to depreciate sharply. Although the naira exchanges officially for N421 per dollar, it trades much weaker at the more accessible parallel market at around N700 per dollar.

The collapsing naira is making imports more expensive and has pushed up inflation to a 17-year high of 20 percent in August with several businesses shutting down as a result.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp