It has been almost a decade since the Central Bank of Nigeria alongside monetary authorities/FG have been actively combatting double digit inflation, yet with every policy thrown at it, inflationary pressures just keep rising and eating deep into the country’s economy’s core as well as the purchasing power of individual households.

While 2021 was a year of strong economic recovery for the Nigerian economy, that recovery however, was neither sustainable nor complete. Unfortunately, prospects for 2022 now look worse than the IMF forecasted last October as it has declined from 5.9 percent to 4.4 percent. According to the IMF’s recent World Economic Outlook (WOE), it argues that the main culprits for this downgrade include Omicron Covid-19 variant, supply shortages and unexpectedly high inflation rate across various economies.

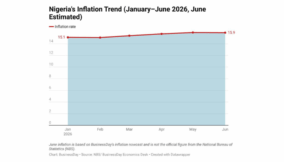

Data culled from the National Bureau of Statistics (NBS) by BusinessDay revealed that Nigeria’s inflation rate for 2015 averaged 7.4 percent, however, inflation rate today stands at 15.63 percent as it accelerated by 23bps last month (majorly due to food inflation) to close the year (2021) and still shows signs of prospective increase in the coming months.

We are less than one year away from the 2023 general elections and Nigerians aren’t faring any better than they were when the current administration took seat in office in 2015 as the current inflation rate has almost doubled its 2015 figures on the average.

The Nigerian government has been saddled with ample opportunities at its bosom to rectify the many structural defects identified within its economic space. However, due to the Federal Government’s slow paced economic reforms, inflationary pressures have been piling and the consequences are evident in the country’s current economic conditions. However, like the popular saying goes… ‘It’s better late than never’.

The World Bank in it’s development update for Nigeria last year titled “Time for business unusual”, noted that even if food production improves, and supply and distribution constraints are eased, a combination of fx shortage, expansionary monetary policy funding of fiscal deficit will continue to generate inflationary pressures and the ripple effects would begin to spread its tentacles to other sectors of the economy.

The World Bank in its publication highlighted medium term (3-18 months) policies that the FG could employ in order to reduce some of these macroeconomic pressures the country currently faces.

The bank in its publication indicated that for inflation to be tackled in the medium term, the FG would need to adopt a mechanism to allow increased borrowing (while managing costs) to cover additional financing needs arising from revenue shortfalls.

“To help contain the growth of money supply, the CBN should enforce the legal limit for the use of CBN overdrafts to the allowed minimum of 5 percent of the previous year’s fiscal revenues,” the report read.

We are less than one year away from the 2023 general elections and Nigerians aren’t faring any better than they were when the current administration took seat in office in 2015

However, in the near term (3-6 months), the report recommended that the country should adopt a single market driven exchange rate as well as enhance exchange rate management.

Emeka Ucheaga, a financial analyst at Credit Direct Ltd stated this policy would require allowing the currency initially to be devalued before it eventually normalizes.

“In the short term, it would create more inflation, however, in the long term it would normalize.

“For example, people are saying that they are expecting another 2022 currency devaluation as they do not feel that the current N416/$1 is the right price for the dollar.

“So if the FG allows the currency to be driven by market forces, then they can anticipate the exchange rate to fall and if the exchange rate falls, then you would subsequently get the inflation rate we are trying to avoid,” Ucheaga said.

The report further provided policy alternatives to help catalyze private investment. It recommended that the FG should reduce trade and transportation costs by addressing delays in border and port clearance by simplifying and harmonizing documents, streamlining and automating procedures and making more information available.

It further indicated that the CBN should clearly communicate the exchange rate strategy to build credibility and improve the availability and accessibility to FX as well as carry out measures to deepen the FX market.

Read also:

“This could be achieved by re-establishing the dollar interbank market and re-enabling commercial banks to trade FX on their own behalf and not solely to fill client orders. This would help increase the depth and liquidity of the FX market while improving price discovery,” the report read.

This would enable the banks to absorb some unexpected FX demand and supply shocks, gradually lessening the need for CBN interventions, while still being subject to open position limits and other prudential requirements.

“The re-establishment of the dollar interbank market would also help participants reallocate FX liquidity and comply with prudential standards,” the report read.

Premium Motor Spirit (PMS) prices has been one trending conversation that has been on the lips of Nigerians lately. Data from NBS’s PMS price watch revealed that average prices paid by PMS consumers last month increased on a year-on-year basis and is anticipated to rise in the coming months depending on policy measures that would be put in place by the FG.

The report indicated that removing the PMS subsidy could lead to a one time 2 to 3 percentage point increase in inflation at the time of the subsidy removal. The report however indicated that the increase could be contained through other complementary measures over the next few months.

The bank recommended that the FG either regulate PMS pricing or set price levels/price ceilings that cover costs of efficient supply.

Omobola Adu, a senior investment officer at Afriinvest told BusinessDay that “With the FG’s current decision to postpone PMS subsidy by another 18 months, is just delaying the inevitable as well as increasing its debt burden”.

“This decision nonetheless would have long-term inflationary impacts that might be worsened as a result of the debt accumulation combined. This also dissuades foreign investors considering the inconsistency in policy/legal decisions,” he added.

The bank in its report further indicated that if FG is to address issues surrounding fiscal pressures, then it would need to rationalize its ineffective tax incentives, fully implement VAT and CITcompliance programs, make tax audits more effective and ensure prompt VAT refunds after putting in place strong controls to encourage higher voluntary compliance.

The Minister of Finance, Budget and Planning, Zainab Ahmed at the federal government’s 2022 Budget Public Presentation, stated that revenue generation remained the major fiscal constraint of the federal government and that her team would vigorously pursue the administration’s Strategic Revenue Growth Initiatives to improve its fiscal position in the year.

She stated that section 30 of the Finance Act designed to amend section 10, 31 and 14 of VAT is in relation to VAT obligations for non-resident digital companies and the mechanism that will be used is to restrict VAT obligations mainly to digital non-resident companies who supply individuals in Nigeria who can’t themselves self-account for VAT.

“Several measures are being instituted under the Administration’s Strategic Revenue Growth Initiatives to improve government revenue and entrench fiscal prudence with emphasis on achieving value for money,” Ahmed said.

With regards COVID-19 and the current economic conditions, the report advised expansion of covid-19 vaccination to enable the economy to open up more rapidly especially to private sector investment.

As for the poor and vulnerable, the bank suggested that the FG should integrate the NHGSFP and other social assistance programs into the National Social Register (NSR) and State-level social registers.

It further encouraged the FG to expand the NSR and state-level social registers so that other existing and future social programs could use the available data to quickly identify and enroll households for future support and ensure programs effectively reach targeted groups.

It also suggested that the government reduce the impact of the pandemic on human capital accumulation by bridging the learning loss through adjusting the curriculum to help catch up the nearly year long school closure.

It then concluded by recommending that FG redouble efforts to collect detailed and consistent evidence on Nigeria’s workers, through labor force surveys and Nigeria’s firm’s through enterprise surveys.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp