Nigeria’s inflation rate rose for the third consecutive month in May, but the bigger concern for policymakers was not the headline figure. It was the acceleration in core inflation, a measure that shows whether price pressures are becoming entrenched across the economy.

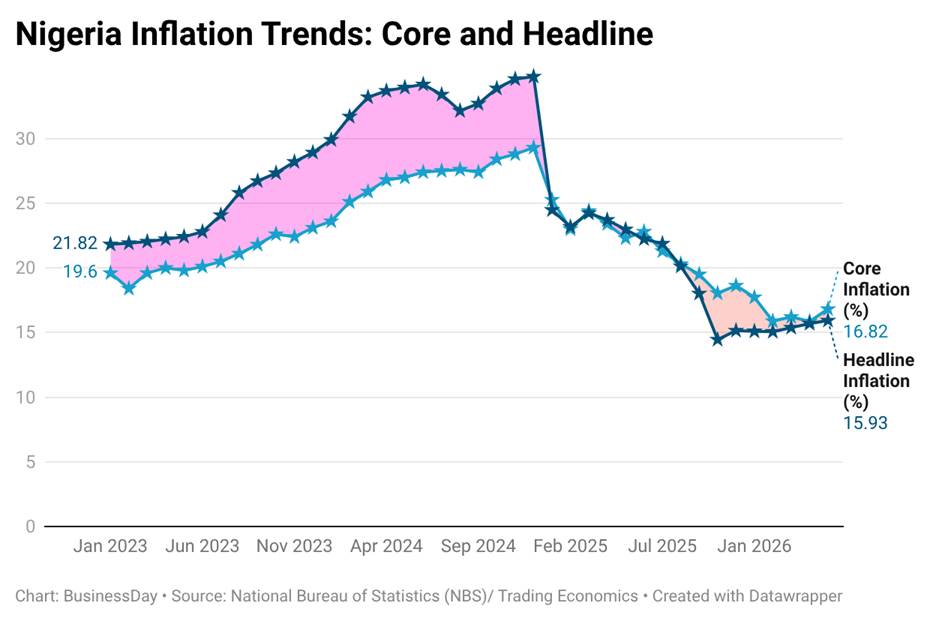

Data from the National Bureau of Statistics (NBS) showed that headline inflation increased to 15.93 percent in May 2026 from 15.69 percent in April and 15.38 percent in March, interrupting an eleven-month period of declining inflation that had raised hopes that Nigeria’s inflation crisis was gradually easing.

While the increase in headline inflation was modest, core inflation delivered a more cautious signal. It stood at 16.82 percent year-on-year in May, while monthly core inflation accelerated sharply to 1.94 percent from 1.03 percent in April. The divergence between headline and core inflation is the most important message from the latest inflation report.

For the Central Bank of Nigeria (CBN), the distinction matters. Headline inflation reflects the pressure households experience through daily expenses, but core inflation provides a clearer indication of whether those pressures are spreading across the wider economy and becoming more persistent. That could determine how quickly the CBN can reduce interest rates.

Why core inflation matters

For households, inflation is experienced through the rising cost of food, transportation, school fees, electricity, cooking gas and rent. Food inflation remains a major challenge. It stood at 16.96 percent year-on-year in May, with the NBS linking higher prices to items including onions, maize grain, egusi, tomatoes, wheat grain, yam tuber, plantain and cowpea.

However, food inflation is often influenced by factors outside monetary policy, including harvest cycles, insecurity, weather conditions, logistics disruptions and transportation costs.

Read also: Brent crashes below $80 for first time since March

Core inflation captures a different challenge. By excluding volatile agricultural products and energy-related items, core inflation measures broader price movements across housing, healthcare, education, restaurants, accommodation and personal services. The acceleration in core inflation suggests that businesses may still be passing higher operating costs to consumers through energy expenses, imported inputs, wages and financing costs.

Abayomi Fashina, Lead, Enterprise Risk Management at STL Capital Group Limited, said persistent core inflation shows that price pressures are becoming more connected to the wider operating environment for businesses. “The concern is that when businesses continue to face rising costs across production, logistics and financing, these pressures become embedded into prices. At that point, inflation becomes more difficult to reverse,” Fashina said.

Sheriff Abdusalam, Corporate and Alternative Investment Analyst, said the latest inflation trend creates a difficult balance for policymakers. “The earlier decline in headline inflation was encouraging, but the recent rebound and movement in core inflation suggest the disinflation process is not yet secure. The market will continue to watch whether underlying inflation pressures are weakening before expecting faster monetary easing,” Abdusalam said.

Why the CBN is likely to remain cautious

The latest inflation data provide important context for the CBN’s decision to maintain a cautious policy stance. In February 2026, the Monetary Policy Committee (MPC) reduced the Monetary Policy Rate (MPR) by 50 basis points to 26.5 percent, marking the first easing move after one of Nigeria’s most aggressive tightening cycles.

The benchmark rate had risen from 11.5 percent in 2020 to 27.5 percent by late 2024 as policymakers battled inflation and exchange-rate instability. The rate cut raised expectations that a broader easing cycle had begun. However, at its May 19–20 meeting, the MPC kept the MPR unchanged at 26.5 percent.

The decision reflected concerns that inflation pressures had not fully disappeared. Although headline inflation remained significantly below previous highs, it had increased for three consecutive months, while core inflation accelerated.

Read also: Health inflation rises to 11.8% as price pressures persist

A faster reduction in interest rates would support economic activity by lowering borrowing costs and encouraging investment. But easing too quickly could weaken inflation expectations and reverse some of the gains achieved through monetary tightening.

Idris Oyekan, Credit and Capital Market Analyst at Quantum Zenith, said persistent core inflation could influence the pace of monetary easing and credit recovery. “Investors and businesses need confidence that inflation expectations are firmly anchored. Until that happens, interest rates may remain elevated, affecting borrowing costs and investment decisions,” Oyekan said.

The challenge beyond monetary policy

Nigeria’s inflation challenge extends beyond what the CBN can solve. Higher interest rates can influence demand, liquidity and inflation expectations. They cannot repair agricultural supply chains, reduce logistics costs or increase productivity.

Muda Yusuf, Chief Executive Officer of the Centre for the Promotion of Private Enterprise (CPPE), said sustainable price stability requires addressing deeper structural weaknesses.

“Monetary policy has a role, but inflation is also driven by production costs, infrastructure challenges, logistics constraints and productivity issues. These supply-side problems must be addressed for inflation to moderate sustainably,” Yusuf said.

The distinction matters because Nigeria’s two inflation pressures require different solutions. Food inflation requires improvements in agriculture, transportation, storage and distribution. Core inflation requires confidence that monetary policy can keep broader price pressures under control.

Why investors are watching core inflation

For investors, persistent core inflation sends a different signal. If the CBN maintains a cautious approach and keeps rates elevated for longer, Nigerian fixed-income assets may continue to offer attractive yields compared with many frontier markets. Treasury bills, government bonds and money-market instruments are likely to remain attractive to investors seeking higher returns.

Read also: Ripple backs Flutterwave with undisclosed funding as Africa’s stablecoin battle intensifies

Recent capital flow trends show that foreign investors are already responding to Nigeria’s high-yield environment. However, much of the interest has been concentrated in portfolio investments rather than long-term commitments to productive sectors. That distinction matters.

Portfolio investors respond quickly to interest rates, liquidity and exchange-rate stability. Foreign direct investors consider deeper economic factors such as infrastructure, power supply, regulatory certainty, security and productivity. High yields can attract financial capital. They do not automatically attract factories.

The difficult balance between yields and growth

The persistence of core inflation is creating a difficult policy dilemma for Nigeria’s economy. For investors, slower monetary easing could keep the yield environment attractive for longer. Treasury bills, government bonds and other fixed-income instruments may continue drawing interest from investors seeking higher returns.

This could support portfolio inflows and provide additional stability to financial markets, particularly if exchange-rate conditions remain favourable. But the same policy stance creates pressure on businesses.

High interest rates increase the cost of credit, making it more expensive for manufacturers, small businesses and companies planning expansion to finance operations and investment. Over time, prolonged tight monetary conditions could slow private-sector recovery, weaken business confidence and delay economic expansion.

The challenge for policymakers is managing this trade-off. Cutting rates too quickly could risk reviving inflation expectations if core inflation remains elevated. Keeping rates high for too long, however, could restrict growth by limiting access to affordable credit.

Nigeria’s next monetary policy challenge is therefore not only defeating inflation. It is finding the balance between preserving price stability and supporting economic recovery. The latest inflation report carries a message beyond the headline number. For households, headline inflation remains the measure of daily pressure.

For the MPC, however, core inflation may determine how quickly Nigeria can enter a sustained rate-cut cycle. The headline number shows where prices are today. Core inflation shows where they may be heading.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp