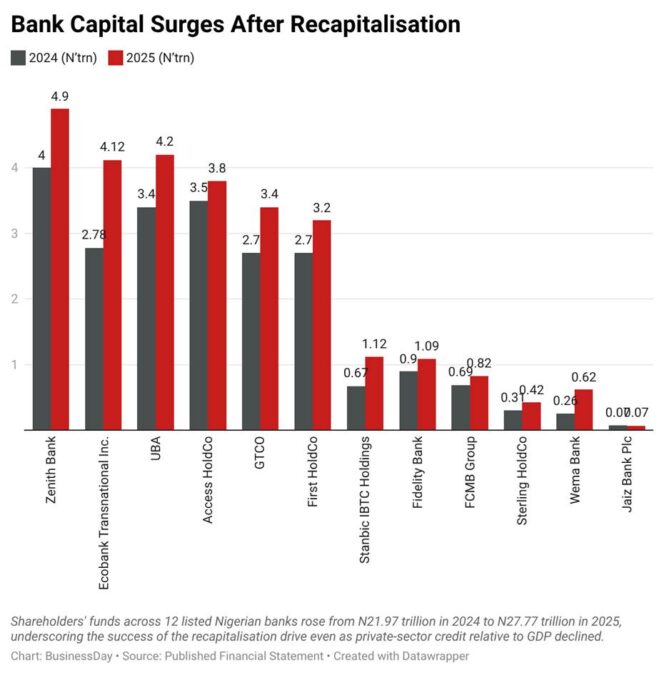

Nigeria's banks have more capital than at any point in their history. Yet businesses are receiving less credit. That contradiction may be one of the most important stories in the country's financial system today. While twelve listed banks increased aggregate shareholders' funds from N21.97 trillion

```

Members Only

Login or create an account to continue

This article is available to registered BusinessDay readers. Please login if you already have an account, or create a new account to continue reading.

New to BusinessDay? Register now and start reading.

```

Oluwatobi Ojabello

Oluwatobi Ojabello, PhD, is a dynamic and multi-dimensional Assistant Editor for Economy and Markets with over two years of professional journalism experience. He delivers authoritative, data-driven coverage of fiscal policy, financial institutions and capital markets, using clear analysis to explain Nigeria’s most complex economic developments. His work focuses on macroeconomic policy, financial stability and corporate performance, turning technical issues into accessible narratives that inform both experts and everyday readers.