After 63 years of independence, Nigeria is still heavily reliant on imports, putting a damper on its efforts to boost industrialisation.

The country’s currency has depreciated above N1,000/$ on the parallel market, for the first time ever, making it difficult for businesses in the manufacturing sector to thrive. While some have stopped operations, others are not producing optimally.

Experts say that in the 1960s-early 80s when the naira was stronger than the US dollar, it encouraged import dependence but slowed the pace of growth and development in the manufacturing sector.

It has also prevented Africa’s biggest economy from tapping the opportunities of the African Continental Free Trade Area (AfCFTA) agreement launched in 2019.

“The strong naira promoted import dependence because it was easy to import. And when the naira collapsed, it became difficult to sustain the things that people were consuming and the things that our industries were using,” Muda Yusuf, chief executive officer of Centre for the Promotion of Private Enterprise (CPPE), said.

He said the structure that the country ought to have stayed with was a resource-based industrialisation, where industries are defined by what they have.

“The nature of our industries at that time was based on the resources that we had. So import dependency was not so high. But when we had the oil boom in the 1970s, there were a lot of dollars to import,” he added.

According to Yusuf, when the oil money was disappearing, the country had already lost the taste and culture towards industrialisation. “Now we are in a mess.”

Toye Folosho, an official at Manufacturers Association of Nigeria (MAN), said if the naira had not crashed against the dollar, it would have created value for investors and the cost of production would not be so high.

“More than 80 percent of the current raw materials and machines used by manufacturers are imported which are dollar quoted,” he said. “Our currency, which has been bastardised, has prevented companies that would have done backward integration and provided raw materials from coming to the country.”

Since Nigeria gained independence in 1960, successive governments have adopted various policies aimed at reducing over-dependence on imports, creating a high number of local jobs and saving the foreign exchange.

Some of the policies are Import Substitution Industrialisation, Nigerian Enterprises Promotion Decree, Structural Adjustment Policy, Small and Medium Industries Equity Investment Scheme, National Industrial Revolution Plan, National Automotive Policy and the Export Expansion Grant.

Read also: Nigeria @63: Northern women call for more gender inclusion in politics

But lack of implementation and continuity of the policies has slowed the progress of the country’s industrialisation.

According to the National Bureau of Statistics (NBS), growth in the manufacturing sector slowed to 2.2 percent in the second quarter of 2023 from 7.3 percent in the same period of 2010.

“The biggest casualties from the naira losing its value are those industries that have high exposure to imports,” Yusuf of CPPE said.

The country’s imports rose by 678.1 percent to N25.6 trillion in 2022 from N3.29 trillion in 2008, according to the NBS.

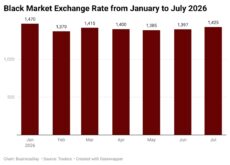

Last year, the naira depreciated against the dollar to as low as 448/$1 from 133.5/$1 in 2004 at the official market. It depreciated to 740/$1 from N134.7/$1 at the parallel market.

The floating of the naira increased the official exchange rate from N463.38/$ on June 9 to N755.08/$ as of September 26. At the parallel market, the naira depreciated to N1,000/$ from 762/$.

The high cost of dollars and the implementation of a 7.5 percent value added tax on diesel imports have pushed its pump price to as high as N1,200 per litre.

Read also: Nigeria @ 63: Entrepreneur urges govt to arrest inflation, provide infrastructure

Inflation in Africa’s most populous nation rose to an 18-year high of 25.80 percent in August from 24.08 percent in July.

“It is obvious that the naira has done so badly and each fall spells doom for the economy. Before now, businesses were booming and a lot of investors were coming into the country,” said Femi Egbesola, national president of the Association of Small Business Owners of Nigeria.

“But now, a lot of them are packing up both big and small while the rest are struggling. So there is little to celebrate at 63 years when it comes to the economy,” he added.

The number of registered manufacturing firms with the MAN dropped from 4,850 in the early 1980s to 2,000 in 2010. From 2017-2022, more than 50 manufacturing companies have shut down.

Some of them are Surest Foam Limited, Mufex, Framan Industries, MZM Continental, Nipol Industries, Moak Industries, Stone Industries, and Procter & Gamble.

Earlier in the year, Unilever, one of the oldest manufacturers, announced that it was stopping the production of its legendary OMO, Sunlight and Lux home and skin care brands.

Recently, GlaxoSmithKline Consumer Nigeria said it would exit the country after 51 years of operations.

“If the trend persists, the nation’s economic growth potential will not be realised. GlaxoSmithKline’s decision critically reflects on the nation’s poor ranking on the ease of business measures, which the chamber has constantly spoken about,” Chinyere Almona, director-general of Lagos Chamber of Commerce and Industry, said.

Dele Oye, national president of Nigerian Association of Chambers of Commerce, Industry, Mines, and Agriculture, said the sudden rise in the price of petrol and devaluation of the naira has caused a significant backlash.

“It is eroding the already earned income and trading capital of several multinational companies that had established their previous earnings based on the official naira rate at the time,” he added.

The latest aggregate Manufacturers CEO’s Confidence Index of MAN also shows that manufacturers’ confidence in the economy dropped to 52.7 points in Q2, the lowest in nearly two years from 54.1 points in the previous quarter.

Read also: Manufacturers grapple with N272bn unsold goods as inflation bites

Segun Kuti-George, national vice president of the Nigerian Association of Small Scale Industrialists, recommended that the government should declare a state of emergency on the industrial sector.

“They should quickly move in by assisting the sector through funding especially Micro, Small and Medium Enterprises ones or else local industries will continue to close up and it will only remain the foreign ones that will be surviving since they are getting funding and low interest rates from their countries,” he said.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp