In Beirut, the capital of Lebanon, common paracetamol is scarce, prices are out of control and social unrest has spilled onto the streets. What is going on there, 4,000km away, shows what Nigeria risks for failing to reform its economy as Egypt did in 2016.

Lebanon is presently facing its worst economic crisis in history; the economy is in free fall. Prices of goods and services are accelerating, poverty ravaging and protesters are taking to the streets amid a pandemic. All are pushing the country to the edge; a similar picture is gradually playing out in Africa’s biggest economy.

But Lebanon’s economic woes did not just start overnight. It is the result of several years of keeping an unsustainable subsidy that has snowballed into an unbearable weight, pushed the country into a financial crisis the pandemic has worsened.

The Lebanese experience

From wheat to medicine down to the price of fuel, Lebanon imports nearly everything.

The government subsidises these items by providing importers with foreign currency at an official rate of 1,507 Lebanese pounds per dollar – six times lower than the market rate. This subsidy keeps prices at which these goods are sold at the domestic market stable. The government also gives a preferential exchange rate of 3,900 pounds to importers of 300 basic items, which is also far below the current black market rate of 9,000 pounds per dollar.

Put together, the country spends roughly $6 billion every year on subsidies, according to official figures.

Read Also: Nigerians more ‘miserable’ than African peers

But it was not too long when the attempt to keep bread, drugs and fuel cheap backfired. When the pandemic struck in 2020, halted dollar inflows and emptied the government’s coffers, it was unable to pay for the subsidies. It threw the Lebanese economy into disarray.

From a high of $30 billion a year ago, the foreign reserve of Lebanon almost halved to $16 billion, there were not enough dollars to bankroll the subsidy agenda.

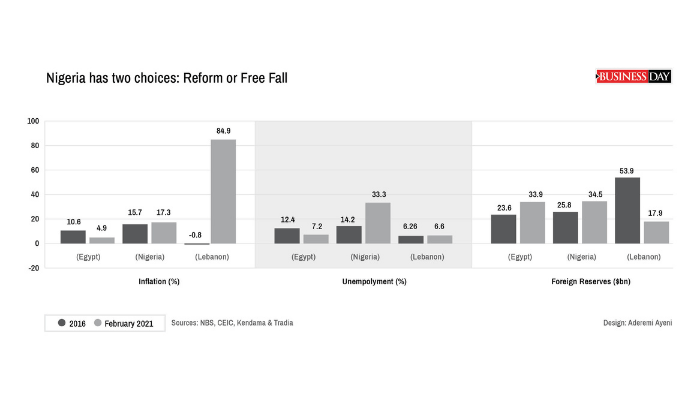

Consequently, Lebanon began to experience a rapid rise in prices as the inflation rate jumped to 84 percent last year; food prices hit 402 percent in December.

Lebanon was unable to pay for a $30 billion loan last year. With no reforms or payment plans agreed since, it could not borrow or attract investors, while the pandemic and banking crisis hit businesses.

More than half the population has been pushed into poverty and people’s savings have lost value. Public debt is crippling, and the local currency has plunged, losing nearly 80 percent of its value. The health sector is buckling under the financial strain and coronavirus pandemic.

The situation has got worse to the extent that Lebanese are back to hoarding basics, such as water and fuel like they did during the country’s 15-year civil war. That is the newest stage in the economic collapse of the country with a population of 6.8 million, which was once a regional hub for banking, real estate and medical services.

When the Lebanese government began to withdraw food subsidies and increase fuel prices, to save dwindling foreign reserves it was too sudden, too late; the people took to the streets.

To reform or not to reform

1n 2016, Nigeria and Egypt were faced with hard choices: reform or risk the Lebanon experience. Nigeria unlike Egypt shied away from undertaking the tough reforms that would spur growth and attract the needed investment to create jobs.

Egypt, instead, floated its currency to reduce the ballooning budget deficit; it phased out petrol and electricity subsidies and started other reform programmes as part of conditions for a $12 billion loan from the International Monetary Fund (IMF).

The reforms paid off. Inflation is under control, the economy is growing, a stable exchange rate has restored competitiveness, the budget deficit and public debt are declining, there are jobs and vulnerable groups are protected.

Of late, Egypt is close to being a regional energy hub. It has ramped up power production capacity to 54,000mw and is exporting its excess production of natural gas and electricity to neighbouring countries.

Nigeria’s story is the exact opposite of Egypt’s successful economic reform. Trillions of naira has been spent on subsidising petrol in the domestic market, as well as electricity.

Aside from this huge amount of subsidies eating deep into government coffers, it has also come at the expense of the country’s infrastructural development in health and education.

Underlying economic problems from 2016 have made matters worse since the pandemic struck, pushing the economy to record a negative growth rate and strangling government finances.

Prices rose to the highest level in four years in February, and the number of jobless Nigerians has swollen to 23 million (one-third of the labour force are unemployed) according to data from the National Bureau of Statistics. More than 40 percent of its 200 million population are living in poverty with six more getting poorer every minute.

“If there is a lesson to learn from Egypt, it is likely that initially-difficult reforms, including FX liberalisation and the lifting of subsidies, can eventually have important economic stability results,” said Razia Khan, head of research for Africa and the Middle East at Standard Chartered, in an email response to BusinessDay.

Damilola Adewale, a Lagos-based economic analyst, said reforms to move the country forward were well known to policymakers just that they lack the will to implement them.

“Such reforms include the creation of a supportive business environment through policy consistency, review of the FX management framework, public-private partnerships led infrastructure development model, deepen deregulation reforms in the oil sector, regulations that support business growth, aggressive diversification efforts, favourable trade and investment policies, tapping to idle assets to unlock liquidity and security architecture must be fixed,” Adewale said.

The pain before the gain

At first, after Egypt floated its currency, inflation went as high as 30 percent, eroding consumers’ purchasing power and the poverty rate increased.

Tough times they say don’t last, and it didn’t take long before the country’s inflation rate began trending downwards to one of its lowest levels. This has put the Central Bank of Egypt in a comfortable position to lower the benchmark interest rate and drive growth. The key interest rate in Egypt was cut to 8.25 percent from the high of 14.75 percent in 2016.

On two occasions last year, the naira was devalued due to pressure on the foreign reserve from declining dollar inflows. Yet, the currency trades at an almost a 15 percent discount from what is obtainable at the parallel market.

Although oil prices, trading at $64 a barrel from the low of $12 last year, bring in more dollars to Nigeria’s reserve has continued to dwindle. It has fallen to $34.5 billion because the CBN is the major supplier. In addition, the rise in imports is unmatched by exports, resulting in a N7 trillion trade deficit in 2020.

Though the pump price of petrol has increased from N145 to N165, the government is struggling to phase out the subsidy, which guzzled over N1.5 trillion in 2019. There is still controversy around the current price as it fails to reflect increasing global oil prices.

“Nigeria already has ongoing reforms but they are not moving well,” said Muda Yusuf, director-general, Lagos Chamber of Commerce and Industry (LCCI), said.

“Nigeria needs reforms in oil and gas as the sector has the potential to attract a lot of foreign capital. Secondly, we need foreign exchange market reform because what we have now is allocative administration of foreign exchange, rationing and banning of items. We need to expand the scope for the market to drive allocation for forex,” Yusuf said, noting other reforms in Customs, regulation, trade and industrial policy.