…As CBN mandates $25,000 BDC’s weekly purchase from authorised dealers

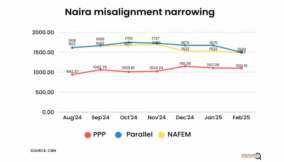

The gap between the official foreign exchange (FX) and the parallel market rates is closing, following the various policies of the Central Bank of Nigeria (CBN).

The naira on Wednesday appreciated to N1, 585 per dollar, crossing the N1,600 psychological point in the black market. In the official FX market, the naira closed flat on Wednesday as the dollar was quoted at N1,499.76 compared to N1,498.95 quoted on Tuesday, according to data from the FMDQ Securities Exchange Limited.

Consequently, the FX spread or gap between the official and black market has closed by N85.24/$.

Compared with the past month, the naira has gained five percent, rising by N80 from N1,665 traded at the beginning of the year in the parallel market, popularly called black market.

On Tuesday, the local currency closed flat at an average rate of N1, 600 per dollar as against N1,599.33 quoted on Monday at the black market.

Also, on Tuesday at the official foreign exchange (FX) market, the naira steadied at N1,499 per dollar at the Nigerian Foreign Exchange Market (NFEM), the official FX platform of Africa’s fourth largest economy, data from the CBN showed.

Currency dealers attributed the naira appreciation to improved dollar supply and moderation in demand for the greenback, following the central bank’s policies.

Olayemi Cardoso, governor of the Central Bank of Nigeria (CBN), said in his Monetary Policy Committee personal statement released on Wednesday that “the increased capital flows and relative stability in the foreign exchange market, alongside the narrowing of exchange rate disparities across different market segments, has been largely due to the bold tightening measures since the beginning of the year.”

Aloysius Uche Ordu, a member of the Monetary Policy Committee (MPC), noted in his personal statement that the exchange rate remained relatively stable for most of the second half of 2024, reflecting increased capital inflows on account of attractive yields.

Although external reserves declined to $39.55 billion as of February 4, 2025, Bala Moh’d Bello, another member of the MPC, said the reserves’ position grew remarkably to $40.88 billion as of November 21, 2024, from $40.06 billion at end-October 2024, a development that strengthens the needed buffer to mitigate unforeseen risks and reinforces the importance of ongoing efforts at sustaining improved foreign exchange supply.

Read also: Naira crosses 1600 mark, appreciates to 1,590 to dollar in black market

The rising reserves position, alongside the relatively stable exchange rate, would enhance Nigeria’s position as an attractive investment destination.

Bandele A.G. Amoo, another member of the MPC, said the total foreign exchange flows through the economy stood at $6,175 billion in September 2024 compared with $2,570.6billion in August 2024.

Furthermore, foreign reserves at the end of October 2024 stood at $39.68billion, equivalent to several months of import cover.

According to him, external reserves are projected to further increase by year-end due to expected reduction in import demand pressures arising from the full deregulation of the downstream oil sector, reduced petroleum products importation regime, increased inflows and other process management by the CBN.

The CBN further clarified that the foreign exchange purchased by BDCs must be sold to end-users at a rate not exceeding a 1 percent margin above the buying rate. This margin will apply to all funds, regardless of the source.

“Foreign exchange cash purchased by BDCs from Authorised Dealer Banks shall be sold to foreign exchange end-users at a rate not exceeding 1 percent margin above the buying rate,” the CBN said.

BDCs are also required to provide daily returns on their foreign exchange purchases from authorised dealers and other sources, as well as sales, through the Financial Institutions Forex Reporting System (FIFX).

Funds purchased by BDCs are restricted to specific eligible transactions, including Business Travel Allowance (BTA), Personal Travel Allowance (PTA), overseas school fees, and overseas medical fees. The maximum disbursement per transaction is set at $5,000 per quarter.

Additionally, records of all transactions must include the BVN of the end-user and the endorsement of the amount disbursed in the International Passport of the beneficiary.

“It is to be noted that Authorised Dealer Banks and BDC operators shall ensure strict compliance with the provisions of Anti-Money Laundering Laws and observance of appropriate KYC principles in the handling of these transactions,” the CBN stated.

The circular warned that any authorised dealer or BDC that violates these guidelines or diverts funds will face appropriate sanctions, including the suspension of their dealership license.

“Authorised dealers shall sell foreign exchange cash to BDCs subject to a maximum of $25,000.00 to a BDC per week,” the circular noted.

“A BDC shall approach its preferred authorised Dealer Bank (ADB) and can only procure the said amount from only that bank of its choice in a week. Any breach of this condition will attract appropriate sanction.”

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp