The Central Bank of Nigeria (CBN) has announced a ten-fold jump in minimum capital requirements for banks, nearly two decades since the last exercise.

The apex bank aims to enhance the resilience of an industry faced with high inflation, naira devaluation and weak economy.

Read also: CBN removes limit on PAPSS for trade payment services

Olayemi Cardoso, the CBN governor, has set the minimum capital requirements for Nigerian banks as follows: N500 billion for those with international authorization, N200 billion for commercial banks with national authorization, and N50 billion for those with regional authorization.

According to BusinessDay calculations, the recapitalization of these banks will bring in N3.3 trillion into the system.

Ayodele Akinwunmi, relationship manager, FSDH bank, said the exercise will position the industry well to take advantage of the expected growth in the economy.

“In addition, the recapitalisation process will attract foreign investors into the banking industry through Foreign Direct Investments, therefore helping the country to drive part of the much-needed long-term foreign currency investment into this important and attractive sector to stabilise the value of the naira,” he said.

For the CBN governor, the current capital requirements for banks, which were established in 2004, are insufficient to support the demands and opportunities presented by an expanding economy.

He noted that recapitalisation would empower banks to extend greater credit to the productive sectors, contributing to the achievement of a $1 trillion Gross Domestic Product (GDP) by 2025.

Recapitalization involves bolstering a bank’s long-term capital to meet regulatory requirements and safeguard shareholders’ investments, often to enhance financial stability or restructure its financial framework.

Essentially, it entails raising a bank’s operational capital to an acceptable threshold set by regulatory authorities.

Similar to the 2005 recapitalization, which reduced banks from 89 to 24, the proposed move will significantly impact Nigeria’s banking sector. Currently comprising 24 commercial banks, Nigeria’s banking landscape may witness further consolidation if the proposed recapitalization materializes.

However, this consolidation aims to cultivate a more robust banking sector capable of supporting Nigeria’s one trillion naira economy, aligning with the overarching vision of the recapitalization initiative.

The move which was initially disclosed by Cardoso, in his address to the Annual Bankers’ Dinner in November 2023, was to enhance banks’ resilience, solvency, and capacity to continue supporting the growth of the Nigerian economy.

History of bank recapitalisation in Nigeria

Nigeria’s banking sector has undergone numerous reforms since 1952, with a recurring theme of increasing the minimum paid-up capital requirement.

In 2005, Charles Soludo, the then CBN governor, mandated banks to increase their minimum capital base to N 25 billion

This measure aimed to fortify the banking industry and stabilize the economy, addressing issues from the banking crises of the 1990s.

Consequently, the sector witnessed mergers, acquisitions, and closures, strengthening remaining banks.

Now, eighteen years later, Cardoso has proposed another bank recapitalization in 2024.

Reason for the Recapitalisation

Olumide Adeshina, an analyst said the apex bank is adopting such a strategy to tackle the insolvency of banks and prevent future possibilities of financial difficulty.

“The CBN is also aware that an efficient and effective Nigerian financial system is not only vital for the promotion of efficient intervention but also for the protection of depositors, maintenance of certainty in stability and protection against system risk and collapse,” Adeshina said.

Breakdown of the recapitalization

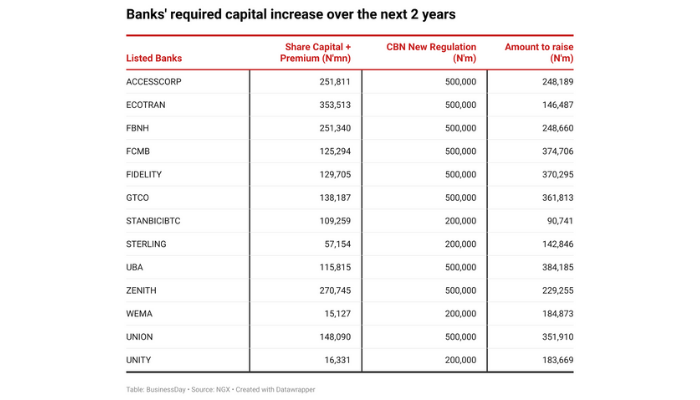

Here is a breakdown of the new minimum capital requirement for existing banks, from the CBN.

The new requirement puts the minimum capital base for banks with international authorisation at N500 billion.

CBN also raised the minimum capital base for commercial banks with national authorisation to N200 billion, while those with regional authorisation were jerked up to N50 billion.

Also, the minimum capital for merchant banks is now N50 billion, while the new requirements for non-interest banks with national and regional authorisations were raised to N20 billion and N10 billion, respectively.

The minimum capital refers to the amount of money a bank needs to have on hand to function safely and absorb potential losses. This new requirement specifies that only a bank’s paid-up capital (the portion of its shares that investors have paid for) and share premium (the additional amount shareholders pay above the face value of a share) will be considered towards meeting this minimum.

The CBN clarified that a bank’s shareholders’ funds (total equity capital including retained earnings) and additional tier 1 capital (AT1) cannot be used to meet the new minimum requirement.

This means that the CBN is prioritizing direct capital injections into Nigerian banks rather than relying on accounting entries to satisfy recapitalization requirements.

AT1 capital is a special type of bond that acts like equity but has some unique features. Additional Tier 1 capital (AT1) is a special type of bond that acts somewhat like equity (ownership) in a bank, but with some key differences like regular equity, its capital can absorb losses if the bank faces financial trouble. AT1 instruments typically come with a fixed coupon rate, similar to a bond. The bank is obligated to pay this interest as long as it’s solvent.

Are Banks Capable?

Access Bank’s Paid-up capital added to its share premium is about half of what the CBN is asking for. While its shareholder’s fund is N2 trillion according to the guidelines, it can not be used for recapitalization.

According to findings by BusinessDay, Access Bank Plc, the country’s biggest bank which also has vast international operations, needs to raise N500 million within the next two years. Currently, it has N251.81 billion in share capital premium, leaving N248.19 million to be raised to meet CBN regulations.

Among the tier-one banks listed, the United Bank of Africa is set to raise the largest sum, amounting to N384.19 billion, to fulfil the new CBN recapitalization requirement. Currently, it possesses N115.82 billion in share capital plus premium.

On the other hand, Ecobank Transnational Inc., a tier-two bank with international authorization, requires the smallest amount to be raised. It currently holds N353.51 billion in share capital plus premium, with N146.48 billion left to meet CBN regulations.

How can they raise more capital?

Gloria Fadipe, head of research at CSL Stockbrokers Limited said that there are only 24 banks so there won’t be too many mergers and acquisitions.

“The big banks will raise money and inject through a right issue, private placement,” she said.

Fadipe added that banks have the option to raise capital either through public offers or by incorporating foreign debt into their financial portfolios.

“We would see banks opting for public offers to raise funds in the market, smaller banks may struggle and that’s where we may see M&A ” Fadipe said.

Yinka Ademuwagun, Treasury and investment manager at Piggyvest said that the CBN was a bit more specific about the type of capital raise that would qualify.

He said they mentioned the right issues, offer for subscription, private placement, merger and acquisition, and upgrade or downgrade of license.

“Of all the above options Right issue and downgrade of the license is the only one that won’t have a dilutive impact,” he said.

He said in all of these the banks have to issue new capital, “So you can issue new capital and use it to fund a Fintech subsidiary or another form of expansion they want to undertake.”

Bond issuance: The banks can raise capital by issuing bonds. Bonds are essentially loans made by investors to the issuer. Investors purchase bonds receive interest payments over a set period, and then receive their principal back at maturity.

Initial Public Offering: is the first public offering of a company’s stock on a stock exchange. This allows the company to raise capital by selling shares to a large pool of investors. After an IPO, the company.

Private placement: In contrast to an IPO, the banks can go for private placements which involve selling shares or bonds to a limited group of pre-selected investors, such as institutional investors or wealthy individuals. This allows companies to raise capital without the scrutiny and expense of a public offering.

Right issue: This is a way for the banks to raise capital by offering existing shareholders the right to buy new shares at a discounted price. This allows existing shareholders to maintain their ownership stake in the company proportionally if they choose to exercise their rights to buy new shares.

Merger & Acquisition: Some banks can merge into a single new entity. Acquisition is when a larger bank (the acquirer) buys another bank (the target) and takes control of its assets and operations and together has more capital.

Ademuwagun said that he expects banks to lobby for the addition of shareholders’ retained earnings.

“If the lobby fails then we might see more bonus issues in the future (though bonus issues do not qualify for this capital requirement exercise),”

“The realization that retained earnings and other reserves or additional tier-1 capital does count should prompt banks to move those items after share premium up the equity statement in the future and the way to do this is via bonus issues,” he said.

Other requirements of CBN capitalisation

Currently, the CBN requires that banks with international subsidiaries maintain a capital adequacy ratio (CAR) of 15 percent while banks without international subsidiaries maintain a CAR of 10.0 10 percent.

The minimum requirement for systemically important banks is 16 percent (although the CBN has been giving a forbearance). Following the implementation of Basel III, an additional tier 1 capital is required for a capital conservation buffer of 1 percent of total risk weighted assets .

A countercyclical capital buffer , to be determined by the CBN periodically taking into consideration the prevailing macroeconomic conditions and developments within the financial sector may also be required.

Implications of the recapitalisation

Ademuwagun mentioned that recapitalization translates to a stronger banking system.

“Banks that can withstand external shocks,” he said.

He also explained that if a bank goes for the dilutive options then that might translate to a drop in their valuation on the exchange.

“If a bank acquires another bank it might lead to the delisting of one bank and the improvement or drop in the valuation of the new bank, it all depends on the form of capital raise used, ” he said.

According to Olumide Adesina, an analyst, jobs will likely be cut, and some banks, especially the low-tier banks, will be acquired.

“Although the Central Bank has permitted mergers and acquisitions, this suggests it anticipates that some banks might struggle to meet the new capital requirements,” Adeshina said.

A report by Fitch stated that tighter monetary policy and the CBN’s progress in clearing the backlog of FX forwards has driven a modest recovery in the naira, to about 1,300/USD on 27 March from about 1,600/USD at the end of February.

“This has caused foreign-currency risk-weighted assets to deflate in naira terms and provided some support to the banking sector’s capitalisation,” the report said.

Analysts at CSL Stockbrokers Limited said in a recent note that in dollar terms, banks have seen a significant reduction in capital given the recent steep devaluation of the naira.

“During the banking consolidation exercise of 2004, the minimum capital requirement for banks was raised from N2 billion to N25 billion. The dollar equivalent of N25 billion at that time is significantly lower than what it is today, and many believe this may be the reason behind the proposed recapitalisation,” they said.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp