Nigeria’s fiscal instability is a ticking time bomb, threatening the nation’s economic future. The country’s financial troubles didn’t start recently; they have been a growing issue for years and are getting more severe. Rising interest rates now force the federal government to spend more on paying interest on its debt.

This situation is problematic because it means less money is available for crucial sectors like agriculture, health, and education. These areas are vital for improving the lives of the citizens.

As interest rates climb, the government’s budget gets squeezed, with a larger portion going towards servicing debt. This shift means that less funding reaches sectors that could make a real difference in the quality of life for many people.

Agriculture, for instance, is more than a livelihood; it’s the heartbeat of millions. In Nigeria, it significantly contributes to the economy, providing employment and ensuring food security for families.

“This shift means that less funding reaches sectors that could make a real difference in the quality of life for many people.”

Data from the National Bureau of Statistics (NBS) shows that in Q1 2022, the agriculture sector grew by 11.55 percent year-on-year, contributing 22.36 percent to the overall GDP in real terms. Despite challenges, this sector remained a vital pillar.

However, in Q1 2023, the growth rate declined to 2.31 percent year-on-year in real terms. Severe cash crunches impacted performance, leading to a decrease in agriculture’s contribution to the overall GDP to 21.66 percent.

Read also: Prices of tomatoes, garri, beans rise 205% in one year – NBS

By Q1 2024, the sector saw a slight rebound, growing by 0.18 percent year-on-year in real terms. This modest improvement followed the previous year’s decline, with agriculture’s share of the overall GDP standing at 21.07 percent. This reflects ongoing struggles but indicates a modest recovery.

The government’s increasing expenditure on debt interest highlights a critical issue. When a significant portion of the budget is allocated to interest payments, the available funds for essential services diminish.

This situation creates a cycle where rising debt interest leads to less investment in crucial areas, which can further exacerbate social and economic challenges.

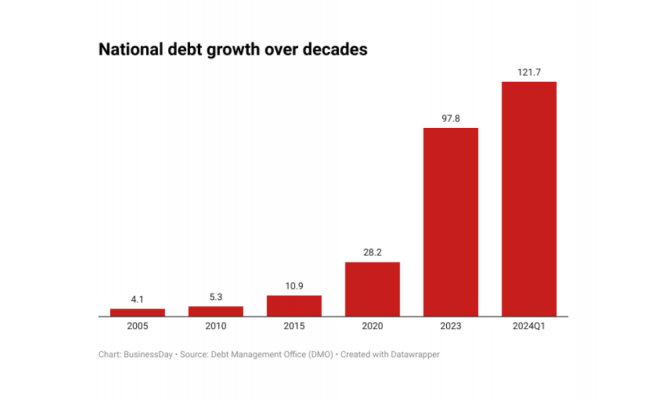

Nigeria’s debt has surged dramatically, rising from 4.14 trillion Naira in 2005 to a staggering 121.67 trillion Naira by the first quarter of 2024. This sharp increase highlights the escalating borrowing and the growing challenges in debt sustainability and fiscal management for the Nigerian government.

As Nigeria’s debt crisis deepens, it’s essential to understand the historical context and current fiscal challenges. Historically, as shown in the publication of LBS July session, Nigeria’s debt issues have deep roots. By the end of 1952, Nigeria’s total debt burden had reached £21.24 million. As colonial rule ended in 1960, the country’s aggregate debt stock stood at approximately £17 million.

The national debt burden increased significantly as the country sought to finance its war efforts from 1967 to 1970. From 1970 to 1979, Nigeria’s external debt grew at an alarming rate, accumulating rapidly when oil prices crashed in 1982, reaching over $30 billion and leading to a severe debt crisis.

In 2005, Nigeria secured a landmark $18 billion debt relief, clearing the remaining $12 billion owed to the Paris Club in 2006.

By 2023, the debt-to-GDP ratio was 46.3 percent, now 52 percent. In the first quarter of 2024 alone, N2.46 trillion was used to service public debt, highlighting the persistent challenge of managing the nation’s financial obligations.

This situation is not unique to Nigeria. Highly indebted countries are likely to experience instability, and Africa’s growing debt burden is becoming a significant concern. As borrowing continues to rise, many nations are becoming ensnared in a vicious cycle of financial distress.

Nigeria stands out as a prominent example, but it is not alone. Other heavily indebted African countries include South Africa with $294 billion; Egypt with $265 billion; Morocco with $135 billion; and Algeria with $127 billion. Nigeria ranks fifth among these nations.

Moreover, according to the Economist Intelligence Unit (EIU), Kenya, Angola, Ethiopia, Ghana, and Côte d’Ivoire occupy the 6th through 10th positions, respectively, in terms of debt levels.

This widespread debt crisis underscores a broader trend of economic vulnerability across the continent. Additionally, many African countries, including Nigeria, have significant portions of their debt in foreign currencies, which adds another layer of complexity to their financial challenges.

Amid these financial strains, Nigeria faces a series of pressing challenges. The rapidly growing national debt, combined with rising insecurity, casts a long shadow of uncertainty over the future.

This instability is affecting not only the country’s economic prospects but also driving many individuals to look for opportunities abroad, despite their high qualifications. This outflow, often called brain drain, further depletes Nigeria’s pool of skilled professionals and worsens the existing talent shortage.

Read also: Nigeria’s debt service-to-revenue ratio to hit 110.4% in 2024

Adding to the complexity, Nigeria is grappling with a highly polarised political climate. The deepening divisions within the political sphere are making it harder to reach consensus on essential reforms and policies.

This lack of unity hampers the government’s ability to effectively address the nation’s crises and stabilise the situation.

Moreover, many manufacturing firms have already left Nigeria, fleeing the ongoing political and economic instability. Their departure not only reduces the country’s industrial capacity but also impacts employment and slows economic growth.

Experts caution that one of the greatest threats facing Nigeria is the potential loss of investor confidence. If the economic and political crises continue, investors may start viewing Nigeria as an unsafe place for their money.

Such a shift could drastically limit the country’s ability to attract foreign investment and secure necessary loans. Without these financial lifelines, Nigeria may find itself trapped in a dangerous debt spiral, struggling to meet its obligations and further destabilising its future.

Unfortunately, Nigeria is shifting from a sustainable debt path to a debt trap. The high external debt-service-to-revenue ratio is alarming, with data from the Economist Intelligence Unit (EIU) showing it at 77.22 percent, far above the benchmark of 23 percent.

This highlights the urgent need for Nigeria to significantly boost its revenue generation capacity, as presented by Bismarck Rewane in the July publication of Lagos Business School’s breakfast session titled “Death or Debt Trap? 21st century road to economic salvation.

The implications of this high ratio are severe, suggesting that a substantial portion of Nigeria’s revenue is being diverted to service external debt, leaving limited funds for developmental projects and social services. This situation could lead to increased borrowing, further exacerbating the debt cycle and pushing the country closer to a debt trap.

Read also: Debt servicing gulps 65% of Nigeria’s revenue in 2023, hits N7.7trn

Segun Muda, an investment banker, said that as a concerned citizen, seeing that Nigeria’s external debt service-to-revenue ratio is 77.22 percent, compared to the benchmark of 23 percent, is alarming.

This high ratio means that a substantial portion of our country’s revenue is dedicated to servicing external debt rather than being invested in essential public services like healthcare, education, and infrastructure.

“It’s disheartening to think about the impact this has on our daily lives and the future of our children. This situation makes it clear that we need significant changes in how our government manages debt and generates revenue,” he added.

The Professional Update Forum (PUF) states that analysing Nigeria’s fiscal situation reveals a troubling external debt service-to-revenue ratio. This indicates that the country is devoting a disproportionate amount of its revenue to debt servicing, which can hinder economic growth and development.

Historically, Nigeria’s debt issues have deep roots, as highlighted in the Lagos Business School’s July session publication. This high debt servicing requirement limits the government’s ability to invest in critical areas that could stimulate economic growth and diversification.

To address this, Nigeria must enhance its revenue generation through diversified economic activities and improve fiscal policies to ensure sustainable debt management.

A financial analyst who prefers to remain anonymous states that Nigeria’s external debt service-to-revenue ratio of 77.22 percent poses significant risks to its economic stability.

This ratio, much higher than the 23 percent benchmark, suggests that the country is at risk of a debt trap, where increasing portions of revenue are used to service debt, leaving little for developmental projects.

The current high ratio underscores the need for immediate and effective fiscal reforms. Enhancing revenue generation through broadening the tax base, improving tax collection efficiency, and encouraging foreign investments are critical steps.

Additionally, prudent fiscal management and transparent governance are essential to restoring investor confidence and ensuring long-term financial stability.

The nation is currently facing nationwide protest over high cost of living. Young Nigerians are on the streets demonstrating lack of jobs, poor government accountability and economic performance.

It has turned into a bloody protest with several Nigerians killed.

Oluwatobi Ojabello, senior economic analyst at BusinessDay, holds a BSc and an MSc in Economics as well as a PhD (in view) in Economics (Covenant, Ota).

Wasiu Alli is a business and finance journalist at BusinessDay who writes about the economy, business trends, and politics. He holds a BA. Ed. and M. Ed. in English Language and Education.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp