Over the past decade, Nigeria’s GDP per capita—a measure of the average income per person—has fallen sharply. Data from Macrotrends and the World Bank indicate that the country’s GDP per capita has dropped from roughly $3,201 in 2014 to $1,621 in 2023.

This fall contrasts with economic trends in neighbouring West African countries, where GDP per capita has remained stable or increased.

“Over the past years, Nigeria has also grappled with persistently high inflation, which has eroded citizens’ purchasing power. According to the National Bureau of Statistics (NBS), inflation stands at 32.7 percent as of September 2024—one of the highest in the region.”

More concerning, Nigeria’s current GDP per capita is lower than it was over four decades ago. In 1981, the figure was $2,188, a level that now seems out of reach, raising questions about the country’s economic direction.

As Nigeria’s economy continues to slide, how can it build resilience to avoid another “lost decade” of economic growth?

Read also: NBS to rebase Nigeria’s GDP in November

A decade of economic challenges

Nigeria, Africa’s most populous country, has long relied on oil exports as its main source of revenue. This dependency has made the country extremely vulnerable to global oil price fluctuations, leading to economic difficulties during downturns.

The oil price collapse of 2014 was a crucial turning point, setting off a series of economic setbacks that Nigeria still faces today.

Over the past years, Nigeria has also grappled with persistently high inflation, which has eroded citizens’ purchasing power. According to the National Bureau of Statistics (NBS), inflation stands at 32.7 percent as of September 2024—one of the highest in the region.

In contrast, neighbouring countries such as Ghana, Benin, Togo, and Côte d’Ivoire have managed to keep inflation in check.

This long-standing inflation in Nigeria has pushed millions into poverty, effectively reversing much of the economic progress of the previous decades. The decline in real incomes and worsening economic outlook has resulted in a growing number of Nigerians facing financial hardship, even as regional neighbours have made strides in economic stability.

Regional comparisons and lessons

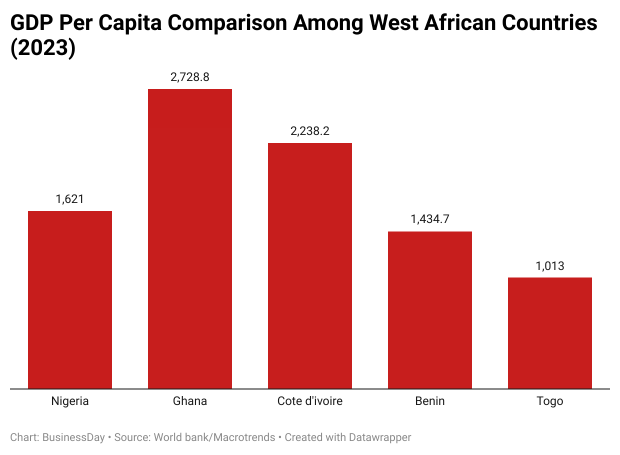

While Nigeria grapples with economic turbulence, its West African neighbours have fared better. Côte d’Ivoire, for example, has seen its GDP per capita rise to $2,728.8 in 2023, supported by policies that emphasise industrialisation and agricultural exports.

With a stable inflation rate of 3.8 percent, the Ivorian economy has demonstrated resilience in navigating global economic pressures, allowing it to sustain a level of growth that Nigeria has struggled to achieve.

Ghana has also made significant economic strides, with a GDP per capita of $2,238.2 in 2023. The country has invested heavily in sectors such as mining, agriculture, and technology, which has enabled it to maintain economic growth even amid challenges.

Meanwhile, smaller economies like Benin and Togo have reported consistent growth and lower inflation rates compared to Nigeria, showcasing effective economic policy.

Benin’s GDP per capita currently stands at $1,434.7, and Togo’s at $1,013—numbers that underscore the gains possible with focused and strategic governance.

Policy missteps and economic consequences

Critics argue that Nigeria’s economic issues stem from a pattern of ineffective policies and decisions made over the past decade. Since 2014, the country has contended with low oil prices, rising debt, and a depreciating currency.

Maintaining fuel subsidies and delaying essential reforms has only worsened these challenges. Billions of naira, spent on subsidies, have drained public funds that could have been directed towards infrastructure, healthcare, and education—investments vital for strengthening Nigeria’s economy.

The current government has taken significant steps by removing fuel subsidies and unifying the foreign exchange rate.

Although these reforms signal progress, many Nigerians continue to face hardships, as deregulation of the oil and gas sector has led to substantial increases in fuel prices, exacerbating the financial strain on families.

Rising living costs have made it increasingly challenging for the average Nigerian to manage daily expenses, underscoring the need for a more balanced approach to reform.

Read also: Nigeria’s GDP Rebasing: What it means beyond the numbers

A path forward: Balancing reforms with public impact

With recent reforms, some experts are cautiously optimistic about Nigeria’s economic prospects. Removing fuel subsidies and adopting a floating exchange rate could, over time, boost economic efficiency and attract foreign investment, setting Nigeria on a path to recovery.

However, these reforms come at a cost, particularly as inflation continues to erode the purchasing power of millions.

To truly stabilise the economy, Nigeria needs to diversify its revenue sources, investing in sectors such as agriculture, manufacturing, and technology.

This shift would reduce the country’s heavy reliance on oil exports and create job opportunities for its rapidly growing youth population.

Tackling corruption and strengthening public institutions will also be essential in ensuring that economic gains are widely shared across society.

These steps are necessary for building a resilient economy that can better withstand global economic shocks and provide a higher standard of living for Nigerians.

The Loss of Economic Progress and Future Prospects

For most Nigerians, the last decade has been marked by diminishing returns and lost progress. The drop in GDP per capita from $3,201 to $1,621 underscores a lost decade of economic growth, highlighting the urgent need for policy reforms that support sustainable growth and equitable income distribution.

The road to recovery will not be easy, and immediate improvements may take time. However, there is hope that a renewed focus on long-term structural transformation and responsible fiscal policies can help Nigeria regain lost ground and foster a more resilient economy.

As Nigeria faces these economic crossroads, a pressing question arises: How can policymakers ensure that the next decade doesn’t repeat the challenges of the past?

Oluwatobi Ojabello, senior economic analyst at BusinessDay, holds a BSc and an MSc in Economics as well as a PhD (in view) in Economics (Covenant, Ota).

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp