Nigeria is embarking on one of the most ambitious tax reform programs in decades, aiming to fix a system that has long been broken, leaving the country’s finances in chaos.

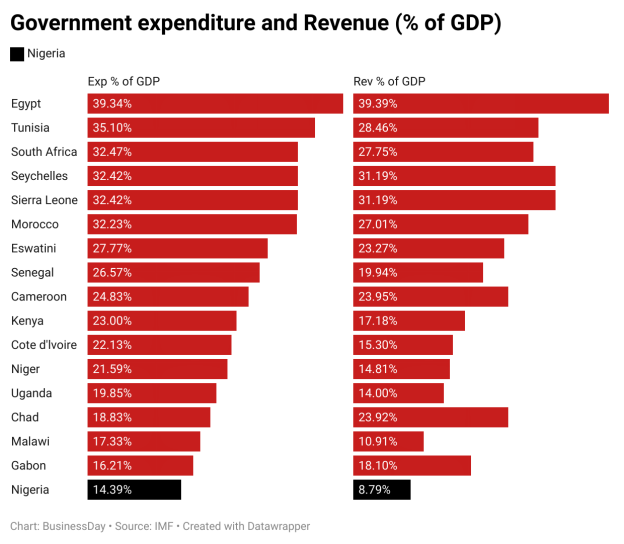

With over 60 different federal, state, and local taxes, only about 10.9 percent of the country’s GDP is collected in government revenue—well below the sub-Saharan African average of 16.5 percent.

“In a bid to relieve struggling citizens, essential goods and services such as food, education, healthcare, and rent will be exempt from VAT.”

This gap is a ticking time bomb for a nation already struggling to provide basic services and tackle an ever-growing mountain of debt. So, what do these tax reforms mean for you—the average Nigerian, your business, and the future of your country?

Why the shake-up now?

Nigeria’s finances are under immense pressure. Official data reveals that in 2023, the government spent a staggering 66.9 percent of its revenue on debt servicing—though an improvement from the eye-watering 99.3 percent in 2022. Still, this leaves little room for critical sectors like healthcare, education, or infrastructure.

In fact, Nigeria’s infrastructure stock is only about 25 percent of its GDP, well below the international benchmark of 70 percent. As a result, Nigeria ranks 22nd on the Africa Infrastructure Development Index (AIDI).

“The current tax-to-GDP ratio is dangerously low because citizens aren’t paying their fair share,” says Wale Edun, Nigeria’s finance minister and coordinating minister of the economy, speaking at an investors’ forum hosted by the Debt Management Office (DMO) in Washington, DC. “This is inadequate for a country of Nigeria’s size and ambitions.”

The new reforms aim to boost the tax-to-GDP ratio, bringing it closer to the sub-Saharan African average. While no specific targets have been set for the next three years, experts believe this could give the cash-strapped government the breathing room it so desperately needs.

Read also: Tinubu’s tax reform bills scale Senate’s second reading

Here’s how the government plans to overhaul the system:

The current maze of over 60 taxes will be simplified into fewer, clearer categories, with a focus on VAT, personal income tax, and corporate taxes. This restructuring aims to make tax compliance easier for both individuals and businesses.

In a bid to relieve struggling citizens, essential goods and services such as food, education, healthcare, and rent will be exempt from VAT.

Additionally, individuals earning below ₦1.5 million per month will no longer have to pay personal income tax, providing much-needed relief for many Nigerians.

Small businesses, with annual earnings below ₦50 million, will also be exempt from VAT and corporate income tax, a change that will benefit more than 80 percent of Nigeria’s businesses, particularly those in the informal sector.

On the other hand, the government plans to raise VAT incrementally, starting from 7.5 percent to 10 percent by 2025 and eventually reaching 15 percent by 2030. Wealthier Nigerians and larger corporations will shoulder a higher tax burden, helping to address the inequality in the system.

In an effort to tackle corruption and inefficiency, the Federal Inland Revenue Service (FIRS) is rolling out e-tax systems. These digital platforms are designed to ensure greater transparency in payments and improve the efficiency of tax collection.

Financial sector connection

These reforms will inevitably ripple through the financial sector. Banks and financial institutions will face increased demand as more businesses formalize, driving the need for greater compliance and reporting.

However, higher VAT and corporate taxes could squeeze profit margins for businesses, which may, in turn, affect their borrowing capacity.

The push towards digital tax systems is also expected to foster innovation within fintech. More Nigerians and businesses will rely on digital platforms for tax compliance, but there is a risk that small traders and informal workers may be excluded if these systems are not adequately inclusive.

What are the risks?

Tax reforms are never easy, particularly in a country where corruption and poor implementation have eroded public trust. Experts warn that without clear accountability, the additional revenue could end up funding the same inefficiencies the reforms aim to fix.

Ayozie Kingsley, a tax and audit practitioner and partner at Ayozie and Co. Chartered Accountants, emphasises the need for transparency: “If people don’t see tangible improvements in public services, it will be hard to justify asking them to pay more. The government must show that these taxes are an investment in their future.”

There’s also the risk of overburdening the middle class and small businesses. Higher VAT rates, for example, could increase the cost of living, putting even more strain on households already dealing with high inflation.

Why it matters

Nigeria’s tax reforms are not just about raising money—they represent a potential shift in the social contract between the government and its people. A simpler, fairer tax system could create jobs, improve public services, and reduce inequality. But to succeed, every naira collected must be spent effectively.

For the financial sector, the reforms represent both a challenge and an opportunity. Banks, fintechs, and insurers will need to quickly adapt to support businesses addressing these changes while leveraging the digitalization drive to expand their services.

Ultimately, these reforms could be a turning point for Nigeria’s economy—but only if they are implemented with care, fairness, and a clear focus on improving lives. An expert, who prefers to remain anonymous, says: “Tax reform is the price we pay for development. But the real test lies in delivering results that Nigerians can feel, see, and trust.”

Oluwatobi Ojabello, senior economic analyst at BusinessDay, holds a BSc and an MSc in Economics as well as a PhD (in view) in Economics (Covenant, Ota).

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp