In a last-gasp attempt to rescue an economy that has contracted twice in five years, President Muhammadu Buhari has tapped Doyin Salami to become his chief economic adviser much to the muted excitement of the business community due to the lateness of the appointment.

Buhari’s appointment of a chief economic adviser has been seven years in the waiting, with the position last held by Nwanze Okidegbe, who served under former President Goodluck Jonathan from 2011 to 2015.

Some business leaders say the appointment is long overdue and questions why it took so long to appoint a chief economic adviser, especially when the economy’s dwindling performance has yearned for one since Buhari first rode into power in 2015.

The business leaders are also sceptical of the impact Salami as chief economic adviser will have on the economy when his recommendations as chairman of the Presidential Economic Advisory Committee, a marked departure from the President’s actions, have so far fallen on deaf ears.

“The appointment is certainly a belated one as it comes seven years into his tenure and when little can be done,” Muda Yusuf, former director-general, Lagos Chamber of Commerce and Industry (LCCI), says.

“However, if the President takes Salami’s advice, then we can at least arrest the economic rot. But expectations must be tempered as we are now just a year away from the next presidential elections,” Yusuf notes.

Nigeria’s economic travails have warranted an economic adviser since Buhari first came into power in 2015, with the metrics showing Nigeria was headed for an economic downturn on the back of lower oil prices.

Read also: NIGERIA IN 2022: What to expect from economy

The crash in oil prices, which began mid-2014, did not however have to lead to a recession in 2016, according to several economists, but the lack of a sound economic management strategy, which a chief economic adviser would have spearheaded, cost the economy.

“If the President cared enough about the economy, an economic adviser should have been appointed long ago. So, why has it taken so long?” a business leader who does not want to be named, asks.

“But for this President, appointing a chief economic adviser at this time may not mean much given that the same person is the chairman of his (Buhari) economic advisory committee, and his views are not popular with this administration,” the business leader says.

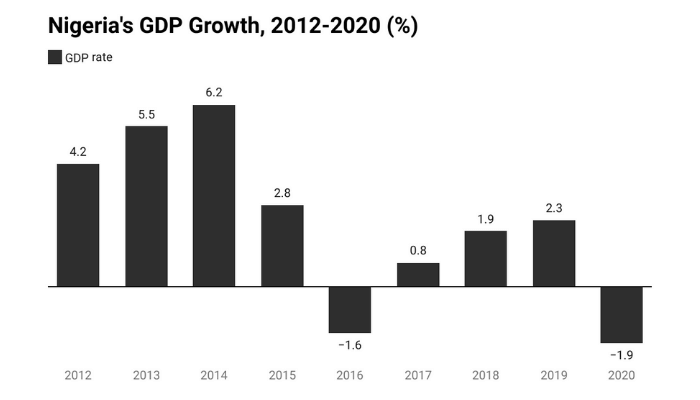

The economy contracted by 1.62 percent in 2016 before expanding by 0.8 percent the following year, but never really recovered as growth has been below the population growth rate of 2.6 percent. This means that Nigerians have grown poorer every year since 2016, as the economy fails to keep up with the rate at which the population is expanding.

In 2018, the economy grew 1.92 percent and 2.21 percent in 2019 before contracting again in 2020 by 1.79 percent amid the ravaging COVID-19 pandemic. The 2021 full-year growth rate is yet to be published but is currently running at an average of 3 percent using data from the first three quarters.

But even that growth rate is nothing to cheer as it has solely reflected the low-base effect from the past year when there was a lockdown and businesses were shut. The World Bank estimates that Nigeria will end up with a GDP that was the same size as in 2010 by the end of 2021, an indictment on the economic management of Buhari.

The unemployment rate is also at the highest since the National Bureau of Statistics (NBS) started collating data, rising five-fold in the last 10 years from 6.4 percent in 2010 to 33.3 percent at the end of 2020. That is the second-highest globally behind Namibia.

Inflation has also been above the CBN’s target of between 6 and 9 percent since 2016.

“President Buhari has signalled an interest in forging a legacy before his time is up, but his legacy projects should have started when he won the second election which makes me wonder if it is too late now,” another business leader states.

“It may just be for the optics,” the person says.

Salami’s views on the economy are well publicised and they are a departure from the way the government has run the economy since 2015.

Salami is an advocate for a greater role in the economy for the private sector rather than the government trying to do everything. He has also openly criticised the central bank’s funding of the Federal Government and has called repeatedly for the elimination of the costly petrol subsidy regime.

Some business leaders say the appointment of Salami, whose views are widely welcomed in the business community, is symbolic and are hoping he finally gets the President’s ears.

“Salami’s appointment is one that would have been better cheered in the investor community if it happened six years ago, but maybe something can still be done to salvage the situation Nigeria finds itself in if the President listens to him,” an investor who does not want to be named, says.

“If he does get the President’s ears then it will be a significant departure from the way the economy is currently being run and that would be of much help to the economy,” the investor states.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp