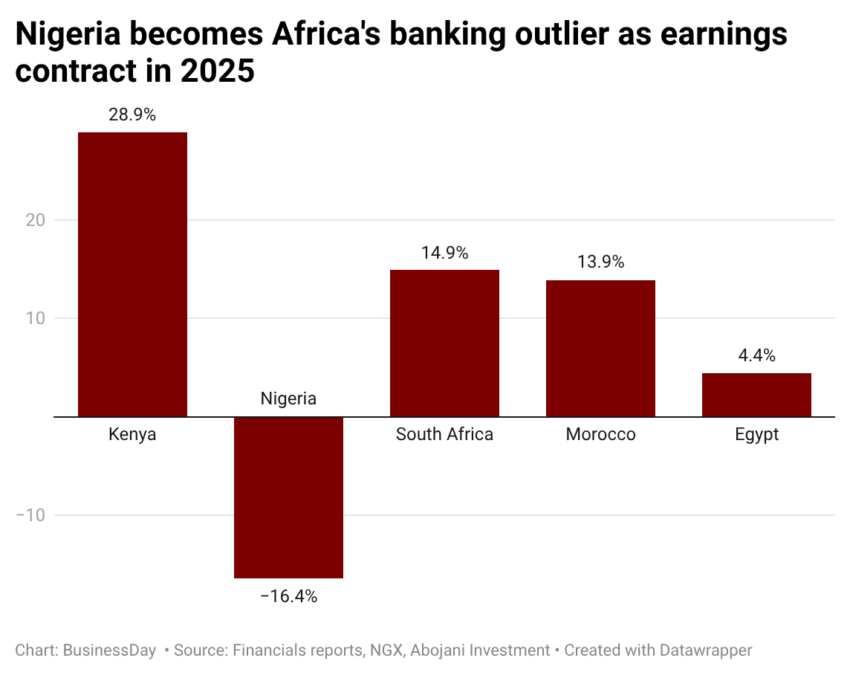

…Kenyan, South African, Egyptian, and Moroccan lenders extend earnings growth

Nigeria's banking sector, once the continent's standout profit story, is losing momentum.

After posting record earnings over the past two years on the back of naira devaluation gains and elevated interest rates, the

```

Members Only

Login or create an account to continue

This article is available to registered BusinessDay readers. Please login if you already have an account, or create a new account to continue reading.

New to BusinessDay? Register now and start reading.

```

Bunmi Bailey

Bunmi holds a degree in Economics from the University of Lagos and has over eight years of experience in content writing and journalism.

Her career spans roles as a financial and business journalist at BusinessDay Media and TechCabal, and as Head of Research at SBM Intelligence, an Africa-focused market intelligence and strategic consulting firm.

She also served as Editor at Finance in Africa, a subsidiary of Businessfront and is currently Assistant Editor, Finance (Africa), at BusinessDay.