Bank of America (Bofa) Securities has put out a comprehensive market note on Nigeria and BusinessDay here offers our readers excerpts from the report.

President Bola Tinubu’s political capital has delivered fuel subsidy removal and floating the naira with no social protests. With the current momentum, Tinubu’s next big move should be to reduce oil theft by reforming the security sector and involving host communities near the pipelines.

If successful, this could increase crude production to 1.6m bpd in 12-18 months, from current 1.2m bpd, barring OPEC limits. Positive oil prospects plus Dangote refinery coming online represent a potential structural improvement in Nigeria’s outlook.

Nigeria depends on hydrocarbons for 90% of its exports, at least half of fiscal revenues and about 6% of GDP. Higher oil revenues, and increased effort for non-oil revenue would ease the high debt service burden.

B+ credit rating in two years possible on reforms

Market-implied ratings from bond spreads are already B, adjusting faster than actual credit ratings. We think structural improvements will not only deliver the B rating next year, but even further prospects of B+ within two years.

Nigeria has low external leverage and financing requirements including a manageable external debt-servicing burden. FX reserves are moderate and can absorb near-term external funding constraints. Moody’s Caa1 rating likely to be adjusted higher too.

Risks to our call: Complacency: Losing reform momentum means limited oil sector reforms, maintaining FX restrictions, and continued financial repression in local markets.

Naira is now undervalued post the float

Higher oil exports ($12 billion more) and a liberalised import regime ($10 billion increase in non-oil imports) can still result in consistent current account surpluses over the medium term. USDNGN has moved from overvalued to undervalued.

We now see a USDNGN fair value of 680 per USD (previously 580). However, USDNGN is likely to trade above this level, with year-end 700, and a return to 650-680 in early 2024. The caution is transition time, aligning rates and still to unlock more USD into the formal market will take some time. When the dust has settled, the value of the naira should be stronger and appreciating.

Strategy: waiting on credit dips to buy again

For specific bond recommendations, we await further dips to create entry points. We have a constructive view for the next two years on the credit outlook.

We are still cautious on local markets and wait to engage when FX distortions are cleared- multiple rates, restrictions, and positive real rates. We do not think the CBN has the appetite for aggressive rate hikes yet.

Nigeria’s multiple challenges include declining oil production (Exhibit 1); a heavily managed exchange rate regime (Exhibit 4); low tax revenue (Exhibit 12), high debt servicing to revenue ratios (Exhibit 13); and an unsustainable fuel subsidy regime (recently removed), leading to the government running unprecedent fiscal deficits breaching the 3% limit.

The local market still has negative real rates (Exhibit 7), and restrictions on FX. As a result, Nigeria has suffered multiple rating downgrades. There is still no IMF-funded program or access to international capital markets while global rates are high.

President Tinubu was inaugurated on May 29 but is yet to appoint a full cabinet. He has moved swiftly to remove fuel subsidies and float the naira and has promised to reduce oil theft and increase fiscal revenues. We believe that both are likely to be addressed over the medium term.

Despite the multiple challenges suffered by Nigeria, external debt (servicing) is low, as are near-term Eurobond maturities (Exhibit 16) while FX reserves are moderate (Exhibit 11). implementing the core reforms provides upside to Nigeria’s credit outlook.

It likely passed the worst in policy inaction under the previous government. We are turning constructive on Nigeria’s outlook based on the likelihood of oil production being boosted by 400,000 bpd by the end of 2024.

Risks to our call: Losing reform momentum means limited oil sector reforms, maintaining FX restrictions, and continued financial repression in local markets. Tinubu promised a “thorough house cleaning of monetary policy” and reducing oil theft. Failure to eliminate central bank unauthorised fiscal financing is a risk.

Markets are pricing in a rating upgrade

Meanwhile, markets have responded positively to recent policy pronouncements with bond spreads tightening and performing better than peers, see Exhibit 2 and Exhibit 3. This is the first time in many years that Nigeria bonds are performing better than Angola.

In our view, it reflects the multiple upside triggers still in store for Nigeria on implementing reforms. On the other hand, Angola upside triggers are limited- oil prices at $75 per barrel could shift Angola fiscal surplus into a small deficit.

The big wins for Angola would be a Eurobond issuance near term or re-engaging with IMF on a funded program. Both are not likely near term. Global interest rates are too high for single B and the authorities have not signalled a likely return for a Fund program.

Rating upgrades in prospect

In 1H 23 Moody’s downgraded Nigeria to Caa1/stable while S&P affirmed its B- rating and weakened the outlook to negative. Fitch downgraded Nigeria to B-/stable in November 2022 and has stayed on a stable outlook including most recently in May 2023. We believe further downgrades are unlikely. We think a rating upgrade is more likely.

Moody’s decision to move to Caa1 before the elections becomes a difficult to justify. The primary reason for moving to Caa1 was the continued deterioration of the fiscal and debt position. Rising debt servicing costs have been taking a large portion of fiscal revenues, making it unsustainable.

Securitising the debt owed by federal government to the central bank of Nigeria is a positive step to reduce debt servicing costs – saves NGN2.5 trillion a year. The NGN22.7 trillion debt was being repaid at a cost of the monetary policy rate (18.5%) plus 5% compared with the new securities with a coupon of 9%.

The baseline for the decision was that reform prospects were limited due to vested interests and that the fuel subsidy would be removed more gradually. Moody’s perceived that it would take some time for a degree of fiscal adjustment to take place.

They argued that Nigeria’s Caa1 rating does not mean it is at imminent risk of default. Rather, it reflects very weak macro fundamentals. We do think Moody’s could reverse course, more likely in 12 than six months, so early next year Nigeria could be back to B- from Caa1.

S&P first step to revise outlook back to stable

S&P is concerned about the country’s debt servicing capacity due to the weak fiscal and external pressures. We expect, near term revision of outlook from negative back to stable in 2H 23 or 1H 24. Fiscal risks have eased on the removal of the fuel subsidy, resulting in higher oil revenues.

Past fiscal deficits of 5-6% of GDP are no longer likely in the medium term. A 2024 Budget that restores the deficit limit to 3% would be credit positive. Issues remain for both domestic and external financing and answers are more likely in 2024 than this year. We would expect S&P to be patient about upgrading to B – more an event for 2024.

Fitch likely first mover on upside

Fitch remained constructive with B-/stable in 2023. We think that Fitch are likely to be the first mover on the upside while others are likely to follow in the course of 2024. Fitch has indicated initial reform steps are positive for credit outlook.

The concern is execution and a better plan on increasing non-oil fiscal revenues. The rating constraints of security challenges, low non-oil revenues and weakness in the exchange rate framework are likely going to be addressed in coming months. Exchange rate weakness is half solved.

BB- is a remote possibility in our view

If FX reserves could reach $50 billion over the next 2-3 years, current account surpluses, stronger GDP growth and moderate fiscal balances could present the case for a return to BB-. While too early to talk about BB-, it is possible if structural improvements in the oil sector materialise, as we expect. Beyond 2025, in a bullish scenario. Ratings barely move more than two notches in a 3-year period.

Fuel subsidy removal boosts fiscal outlook

The new administration under President Tinubu has removed the contentious fuel subsidy and floated the naira. The removal of the subsidy, which cost about 2% of GDP in 2022 and about 1% of GDP in 1H 23, will improve fiscal revenues.

Fiscal weakness is likely to have bottomed in 2022 and should improve over the medium term. The removal of the fuel subsidy and likely increase in oil production should be positive for fiscal revenues. The next step should be spelling out in the 2024 budget the measures to increase non-oil revenues and reach the 3% deficit target from next year.

Floating the Naira one step towards orthodoxy

On June 13, Nigeria decided to float the naira, a signal of a return to orthodox monetary policy the internal and external value of the naira being determined largely by market forces. As of today, multiple exchange rates are yet to converge but operational blockages are gradually being eased.

For example, the central bank has removed foreign currency limits on domiciliary accounts. Domestic withdrawals of USD are still limited to $10,000 per day to enable deposit stability and prevention of money laundering activities and comply with anti-money laundering rules.

Some 43 import items are still banned from accessing foreign currency through the importers and exports (I&E) window, meaning that a parallel market may still exist for those goods. The ban is meant to encourage domestic production of the referenced goods cement, and staples such as maize, rice and milk, among others.

Post floating the naira, it has weakened close to 750 per USD. With our revised fair value estimate at 680 (previously 580), the naira now looks undervalued. The caution is transition time, aligning rates and still to unlock more USD into the formal market will take some time.

When the dust has settled, the value of the naira should be stronger and appreciating see Exhibit 6. We use the Compass fundamental equilibrium exchange rate modelling technique. Compass equilibrium exchange rates are consistent with the convergence of external current accounts to levels that are in line with country fundamentals.

Our variables are mainly current account and inflation dynamics. We discuss the current account in latter sections- essentially consistent surpluses with higher oil exports and a liberalised import regime. An addition of $12-13 billion on export revenues from higher oil production is moderated by a liberalised imports regime that could add $10 billion as non-oil imports increase. Still a net gain of $2-3billion that strengthens the current account surplus.

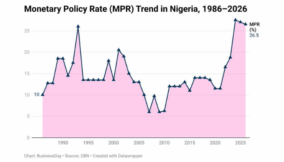

Aggressive interest rate hikes looking unlikely

When Mr. Godwin Emefiele took over as CBN governor in June 2014, inflation was under 10% and the real policy rate was positive. By 2016, inflation had risen towards 15% while policy rates remained lower than inflation. This persisted and the gap widened with inflation breaching 20% in August 2020.

The fuel subsidy removal and naira float mean higher inflation which we expect to rise to 30% in 3Q 23. Latest inflation print for May is 22.4%. A higher rate of 30% would require aggressive interest rate hikes. But these are politically sensitive for a less independent central bank.

We get the sense that aggressive hikes are not likely President Tinubu ultimately wants low interest rates and hiking too much could presumably hurt the manufacturing sector and potentially cause economic weakness. Rather, we expect the focus to be on addressing the sources of inflation reducing the parallel market, fiscal financing by the CBN and boosting domestic production.

Can a new governor be appointed? The legal questions:

President Bola Tinubu suspended Central Bank of Nigeria Governor Godwin Emefiele on June 9. He was arrested and taken into custody. An investigation will be carried out by the Department of State Services (DSS) which will forward the final report to Economic and Financial Crimes Commission if there is cause for prosecution.

Governor Emefiele implemented former President Buhari’s economic policy of managing the exchange rate level and keeping restrictions on imports, centralised FX allocations and financing the government above the regulatory limits. An acting governor has stepped in for the interim.

Emefiele’s departure is not a bad thing given the policy mix he pursued since being appointed. This an opportunity for the new administration to move forward with what President Tinubu described as a “thorough house cleaning” of monetary policy and a path towards a unified exchange rate.

There is a legal precedent with regard to removing/suspending a central bank governor. Governor Lamidu Sanusi in 2014 successfully appealed against his suspension by President Goodluck Jonathan in the high court in 2014. The argument was that CBN law does not include a provision for a president to suspend a central bank governor.

The senate has the power to remove a central bank governor but requires a two-thirds majority to pass the resolution. The new senate started on 13 June. The governing APC does not have a two-thirds majority, but slightly more than half.

The easiest step would be if Governor Emefiele resigned voluntarily before his term of office officially expires in June 2024. Before a resignation, it would be impossible to appoint a substantive governor.

Raising oil production next structural catalyst

President Tinubu intends to increase oil production by reducing oil theft through pipeline vandalism. The long-term targets are ambitious, reaching 2.5m bpd. Oil production levels above 2m bpd would require new investment over many years. We are of the view that 1.6m bpd is achievable in the medium term.

The proposed solutions involve reforming the security sector and getting host communities more involved. Security issues in the oil sector pipeline vandalism and the creation of illegal pipelines subverting the official lines are common in the Niger Delta. President Tinubu seems to possess the political capital to deal with vested interests in the oil sector via subsidy removal and floating the naira: two key measures the former president did not have the guts to deliver.

Reducing oil theft would lead to higher oil production. In our view, increasing crude oil production to 1.6m bpd in the next 12 months is feasible and would be a structural improvement from current levels of about 1.2m bpd. If we include condensates, total oil production could rise from the current 1.4m bpd to 1.8m bpd in two years a level that Nigeria was producing pre-pandemic.

Oil production has suffered temporary setbacks that are related to specific events. For example, in August 2022 and April 2023 crude oil production was barely 1m bpd. However, the resumption of oil production at Shell’s Forcados terminal in October 2022 lifted output substantially.

Similarly, the end of the Exxon Mobil labour strike in April 2023 was followed by higher production in May 2023. We also expect some reduction in oil leakages/pipeline vandalism usually associated with election season, helping our constructive view. Crude oil production should stabilise around 1.4m bpd this year.

Tinubu in favour – no social protests against reforms

President Tinubu has harnessed his political capital. He found support from key constituencies – _the unions and the youth – _which avoided usual protests against reforms in Nigeria. Young people are being promised interest-free university loans. Meanwhile, the president met with labour representatives to avoid potential strikes because of the fuel subsidy removal. Pump prices have more than doubled yet there have been no public demonstrations.

OPEC limits Nigeria crude oil production to 1.4m bpd

The OPEC+ group in the June 2023 meeting pushed for Nigeria’s oil production quota to be reduced to 1.38m bpd, The rationale being that it had consistently produced below its previous quota of 1.742m bpd and the overall need to reduce global oil production to influence oil prices.

The government is pushing for a reversal of the decision. Even with the new quota, Nigeria is still producing crude below the limit. In 2023, the highest level was 1.3m bpd in February 2023 and the lowest was just under 1.2m bpd in May.

So, there is still room to expand by at least 200,000 barrels before reaching the limit. Production quotas could still be higher in 2024 than they are currently. The next OPEC + meeting is November 26 but an OPEC seminar on July 5-6 could also provide some signals.

Oil sector reform starts with the NNPC

Implementing the Petroleum Investment Act of 2021 would be the starting point for sector reform and increase exploration investment activities over the medium to long term. Reforming the Nigeria National Petroleum Corporation (NNPC) is being considered including the separation business units on functional lines: the regulator function vs the upstream concessionaire function.

The other part is NNPC’s asset sales – _selling partial stakes across the downstream (refinery), mid-stream and upstream (production) sectors. This process would take time but could generate valuable USD.

IOCs move focus from onshore to deep water exploration

The main international oil companies (IOCs) operating in Nigeria are Shell, Total, Chevron, and Exxon, among others, responsible for about half of total oil production. IOCs have been divesting from onshore fields over the past few years to help meet net zero emission targets and as some of the fields matured.

They have divested from onshore fields, or marginal fields that don’t have many oil reserves. In addition, onshore facilities are more prone to pipeline attacks and oil theft than deep water oil extraction. The IOCs are not necessarily exiting Nigeria just focusing more on offshore. Local oil companies can have better community relations when extracting onshore oil.

Long-term investment in the oil sector requires implementation of the 2021 Petroleum Investment Act The act places some responsibility on host communities based around the pipelines to help with reducing the illegal activities.

Funding to these communities will act as an incentive for collective responsibility and ownership. Other measures include improving the fiscal regime by lowering the tax and royalties’ structure: size and timing are still unclear at this stage. This should be followed by an improvement in the licencing of upstream production.

Dangote refinery could go live in 4Q 23

The Dangote refinery was commissioned in April 2023 by former President Buhari. We understand the technical issues are almost resolved and Dangote could go online in 4Q 23, helped by the liberalisation of petrol prices. This domestic refinery could reduce demand for oil imports and, at full capacity of 650,000 bbl, could even export some of its output. In the initial stages of production, it is likely to be operating at about half capacity.

CAD to weaken near term, positive over medium term

The 2Q 23 current account balance is likely to be negative (-1.2% of GDP), similar to 1Q 23 (-0.7% of GDP). This is due to a fall in oil production in 2Q (on the Exxon Mobil labour strike in April) and lower oil prices remaining below $80 per barrel in 1H 23.

Over the remainder of the year, we expect oil prices to be higher – $80 bbl, and $82 bbl in 3Q and 4Q respectively. Oil production picks up by 250 thousand bpd by year end. The combination should support an overall current account deficit of -0.1% of GDP. effectively, near balance.

2024 current account outlook has better prospects. Our house view assumes oil prices averaging $90 per barrel. Higher oil production (1.6m bpd) could increase export receipts and eliminate current account deficits over the medium term.

Every additional 100,000 bpd at an average oil price of $80-90/bbl generates $3-3.3 billion per year. A cumulative increase of 400,000 barrels can yield over $12-13 billion per year at $80-90/bbl. The amounts generate up to 3% of GDP in additional receipts.

We allow our forecasts to account for more flexibility on higher imports reflecting the market-determined exchange rate and without import restrictions. We estimate that restrictions on imports and FX availability may have compressed non-oil imports by as much as $10 billion, see Exhibit 10.

Essentially, an open market could see imports rising to account for over 2% of GDP. Overall, we see current account surpluses of 1% of GDP.

Nigeria’s breakeven oil price is a moving target

The external break-even oil price is generally high relative to other oil-producing countries. This is largely due to lower oil production in recent years. In 2022, the oil price averaged $99 per barrel and Nigeria posted a balanced current account.

As a result, we estimate that an average oil price of $100 with oil production of 1.4m bpd could balance the current account, other factors held constant.

On the fiscal side, it is almost impossible to balance the budget even under the most optimistic scenarios. The federal government did not balance its budget even in the 2012-14 high oil price + high oil production environment. Then, the price was above $100/bbl and Nigeria was producing more than 2m bpd.

We would need to go back to our previous 2022 estimates of a fiscal break-even oil price of at least $140 per barrel and assume oil production of at least 1.8m bpd for a balanced budget.

Low external financing needs; issuance likely in 2024

Nigeria has low external financing needs and a current account that is usually near balance, see Exhibit 9. On fiscal financing, the majority of funding is done in the domestic market. We estimate external fiscal financing of close to 1% of GDP over the medium term.

This translates into about $4-5 billion external borrowing per annum. We expect Nigeria to consider an issuance at the earliest opportunity once global rates have started falling in 2024 and when the domestic story is more compelling.

The 2023 budget put external borrowing at $4bn while external repayments amount to $2.5bn. Due to policy inaction, cheap concessional funding has been hard to come by for Nigeria. With markets inaccessible, FX reserves have declined moderately.

The country has no IMF backstop. We therefore think that once market conditions improve, Nigeria will look to issue within the next 12 months. The $500 million Eurobond maturing in July 2023 will be repaid comfortably.

Fiscal performance: 2022 the weakest

Since the COVID-19 pandemic, fiscal deficits have exceeded the legal limit of 3%, averaging close to 5% in the past three years. In 2022, the fiscal deficit of the federal government reached -5.5% of GDP.

Over 80% was funded in domestic market by DMO and the central bank overdraft facilities. Nigeria received $1.5 billion in external financing in 2022, made up of the $1.25 billion Eurobond issued in March 2022 and a syndication loan amounting to $260 million.

2023 budget revisions likely on appointment of Minister

A finance minister is yet to be appointed. Once this takes place, proposals are likely to be put forward to amend the budget. The approved 2023 budget assumes an oil price of $75 per barrel, production of 1.69m bpd and an exchange rate of NGN435.57 per USD. Oil prices have so far been around $75 while oil production including condensates remains below the budgeted levels. The currency float to over NGN600 could inflate oil revenues in 2H 23.

The federal government planned for a deficit of NGN10.78 trillion or 4.78% of GDP in 2023 to be largely financed by the domestic market at about NGN7 trillion. Foreign borrowing put at N1, 76 trillion which could translate into close to $4 billion (pre-naira float) in external borrowings in the plan, largely from concessional sources.

Only the World Bank is pencilled in to provide $800 million in cash payments to support the vulnerable post the removal of the fuel subsidy, increasing non-oil fiscal revenue. The 2024 budget will be an opportunity to prove a credible path to a better fiscal outlook.

Read also: Tinubu’s next big move is fighting crude theft, says Bank of America

Securitisation of CBN debt makes debt cheaper

Tinubu has already effected two fiscal gains – removing the fuel subsidy and securitising the CBN overdraft facility to the federal government. The federal government had an overdraft facility with the central bank at a cost of MPR (18.5%) plus 5%.

In May 2023, the national assembly approved the securitisation of government loans owed to the CBN and these will likely be added to the official debt statistics by the DMO. The loan was about NGN22.7 trillion or $50 billion at time of approval or just over $30 billion post devaluation. The amount represents under 10% of GDP. The new instruments to be issued have maturity of 40 years, no principal repayment in the first three years, amortise over 37 years and pay interest per year of 9%.

The securities will be issued to the CBN by the government. This securitisation lowers the cost of debt servicing for the government as it will now pay 9% instead of about 20% (MPR+3%) for its overdraft facility. That’s at least NGN2.5 trillion of savings in one year.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp