A common misconception, particularly among politicians, is that Nigeria’s low debt-to-GDP ratio signals fiscal discipline and capacity for more borrowing. However, this overlooks the critical measure of debt-to-revenue, which reflects a country’s true ability to service its debt and influences its creditworthiness.

Data from the Debt Management Office (DMO) and the International Monetary Fund (IMF) illustrate this disconnect: Nigeria’s debt-to-GDP stood at approximately 40 percent in 2023, yet its credit rating, a crucial indicator of economic health and stability, is one of the weakest among peer economies.

Read also: Cement sector GDP’s growth falls on rising cost

The illusion of low debt-to-GDP

A low debt-to-GDP ratio is often celebrated as evidence of fiscal prudence. However, it fails to capture the broader picture of creditworthiness. Numerous factors, including political stability, economic resilience, and debt service capacity influence credit ratings. Nigeria’s rating, currently a B- by S&P and a mere 23 percent on the Tübinger Erlangen (TE) score, reflects challenges beyond just its debt size. These include volatile revenue streams, governance concerns, and external vulnerabilities.

These disparities are not unique to Nigeria. A recent report by the World Bank sheds light on the broader difficulties faced by developing economies in managing their debt burdens amidst unfavourable borrowing conditions.

Developing countries paid a record $1.4 trillion on foreign debt in 2023 —World Bank

While a low debt-to-GDP ratio often garners praise, it does not guarantee creditworthiness, especially for nations grappling with significant external pressures. According to the World Bank’s December 2024 International Debt Report, developing countries spent a staggering $1.4 trillion servicing foreign debt in 2023, with interest payments reaching a 20-year high. These rising costs have squeezed budgets, undermining critical spending on health, education, and infrastructure.

For the poorest nations, the strain is even more acute. The International Development Association, IDA-eligible economies paid a record $96.2 billion in debt servicing in 2023, with interest payments surging to an all-time high.

These figures reveal the systemic challenges faced by low-income countries in navigating the global financial system, where borrowing terms are far less favourable compared to advanced economies.

This underscores a paradox: while advanced economies like Japan or the United States maintain high debt-to-GDP ratios, their lower borrowing costs—bolstered by strong credit ratings and institutional trust—allow them to manage these debts sustainably.

In contrast, developing economies, even with modest debt levels, are penalised with exorbitant interest rates due to perceived risks, often rooted in “outdated” or biased credit rating systems.

As Indermit Gill, Chief Economist at the World Bank, remarked, “Multilateral development banks are now acting as a lender of last resort, a role they were not designed to serve.” This reflects the structural dysfunction in global financing, where money flows out of poor economies at the very time it is most needed for sustainable growth.

Global comparisons: A tale of context

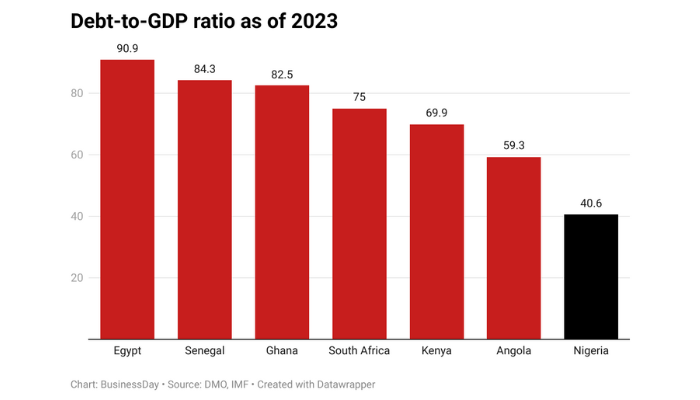

Countries like South Africa carry higher debt-to-GDP ratios but enjoy better credit ratings due to stronger institutions and better access to international markets.

Read also: Data expose gaps in Nigeria’s $1trn GDP target

Japan, with a staggering debt-to-GDP ratio exceeding 200%, maintains an enviable credit rating thanks to low borrowing costs and deep domestic bond markets.

“These rising costs have squeezed budgets, undermining critical spending on health, education, and infrastructure.”

Advanced economies like Japan, the UK, and the US as previously mentioned can sustain high debt levels because they borrow at minimal costs, supported by robust creditworthiness. In contrast, African nations face exorbitant borrowing costs due to perceived sovereign risks.

The Kenyan president’s argument: Credit rating agencies criticised

William Ruto the Kenyan President succinctly captured this disparity when he criticised the bias in credit ratings that drives up interest rates for poorer nations, making borrowing prohibitively expensive.

In a 2023 interview with the New York Times, Kenyan President William Ruto raised concerns about systemic inequalities in the global financial system, particularly regarding how poorer countries are profiled in credit markets. He highlighted that African nations like Kenya are often charged significantly higher interest rates—sometimes four to five times more than advanced economies—due to what he described as biased risk assessments by credit rating agencies.

Ruto argued that this profiling not only increases borrowing costs but also pushes many African economies into debt distress. He criticised the methodologies used by agencies like S&P, Moody’s, and Fitch, pointing out their historical misjudgements, including during the 2007-2008 financial crisis.

In his words, these agencies have once again “priced frontier economies out of the market,” ignoring critical nuances of their economic potential and reforms.

This observation underscores a recurring theme in global finance: the disparity in borrowing costs between developed and developing nations. Advanced economies with high debt-to-GDP ratios, such as Japan or the United States, enjoy lower interest rates and higher credit ratings because of perceived institutional stability and economic resilience. Meanwhile, countries like Kenya or Nigeria, are penalised with higher costs due to systemic biases.

Read also: VP Shettima sees debt to GDP decelerating to 30% after rebasing

Ruto’s argument adds weight to the idea that a country’s creditworthiness is not solely determined by its economic fundamentals. Instead, it reflects a combination of economic metrics, geopolitical perceptions, and institutional confidence—or the lack thereof—within the global financial ecosystem.

“This observation underscores a recurring theme in global finance: the disparity in borrowing costs between developed and developing nations.”

The Wagnerian perspective on borrowing

Adolph Wagner, a German political economist, offers a valuable lens to reframe the borrowing debate in his work titled Law of Increasing State Activities. Wagner argued that as economies grow, governments inevitably expand their expenditures to meet societal demands.

Borrowing, therefore, becomes an essential tool to fund infrastructure, welfare, and public services. In advanced economies, this principle has driven investments that enhance long-term growth and stability.

In Nigeria’s case, however, borrowing often fails to yield productive outcomes, infact many borrowed funds have been repatriated back to where it was gotten through embezzlement according to public affairs analysts.

Critics rightly question the allocation of borrowed funds, which disproportionately favours recurrent expenditures over capital projects. This inefficiency undermines the potential of borrowing to catalyse economic growth, fueling public scepticism.

Rethinking Nigeria’s credit narrative

The focus on Nigeria’s low debt-to-GDP ratio as a sign of fiscal strength misses the mark. What truly matters is the ability to service debt sustainably, attract investments, and maintain economic stability. Improving creditworthiness requires structural reforms to enhance revenue generation, reduce reliance on volatile oil exports by developing the non-oil sector, and ensure accountability in public spending.

Encouragingly, recent reforms spearheaded by the Central Bank of Nigeria (CBN) under Olayemi Cardoso, CBN Governor, have shown promise. Cardoso noted an uptick in Nigeria’s credit ratings, attributed to ongoing fiscal and monetary adjustments. This is a step in the right direction, but sustained progress will depend on aligning borrowing with productive investments that inspire confidence among stakeholders.

Conclusion

A low debt-to-GDP ratio is not a definitive measure of economic health or creditworthiness. For Nigeria, the priority should be improving fiscal discipline, strengthening institutions, and ensuring borrowed funds are used to drive growth. Borrowing itself is not the problem—it is how those resources are managed and whether they create long-term value. Wagner’s insights remind us that borrowing can be a catalyst for progress, but only when coupled with sound governance and visionary planning.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp